[Deep Dive] Alibaba, Meituan and JD's Quick Commerce War and How Grab and Sea Will React

A Deep Dive into the Platform War, Unit Economics, and the Next Phase of E-Commerce in SEA

This piece was written in collaboration with Zack Zhu, who publishes Contrarian Perspectives and is one of the sharpest analysts I know. Zack anchored the China section with ground-level insight into how Meituan, Alibaba, JD, and Douyin are actually fighting this battle, and why the unit economics matter more than the headlines.

I then built on that to translate the lessons to Southeast Asia, with a primary focus on the three key competitors: Grab, Sea Limited and TikTok Shop. If you like analysis that goes past the noise and into how platforms actually compete, I’d highly recommend subscribing to his newsletter.

Introduction

China’s quick commerce war has been years in the making, but it is only in the past 12-18 months that it has erupted into a full-blown, high-stakes battle between the country’s tech giants.

But what is quick commerce, and why is Alibaba, the world’s largest e-commerce platform, burning roughly $5 billion per quarter just to remain competitive?

Most importantly, why does this fight matter, and what lessons does it hold for markets beyond China, particularly Southeast Asia?

In this article, we’ll explore the current state of China’s quick commerce boom and how its situation might offer a glimpse into the future of the Southeast Asian market.

Table of Contents

Quick Commerce 101

Why Quick Commerce is Inevitable

Quick Commerce in China

Meet the Players

The Backstory of China’s Quick Commerce War

Why JD Lit the Match

The Convergence of Four E-Commerce Logistics Models

How the War is Being Fought

JD’s Push into a New Logistics System

Alibaba Joins the War

Will Alibaba Succeed this Time?

Meituan and Alibaba’s Competitive Advantage

The Current Status of the War

GMV Market Share: Alibaba vs. Meituan

China’s Food Delivery Unit Economics (Pre-War)

China’s Food Delivery Unit Economics (Post-War)

The Difference in Unit Economics

Delivery Network

Core Users of the Platform

What are they Fighting for?

The Quick Commerce Market

Traffic Spillover

The Different Approaches of Alibaba vs. Meituan

Quick Commerce Market in 2024

What has Changed in 2025?

What are the Limits of Quick Commerce?

The Next Stage of the War & Other Players

AI Search & Qwen

Regulators & Platform Subsidies

China’s Quick Commerce Subsidies

What makes China’s Instant Logistics Special? How Do Platforms Aggregate So Much Volume?

A Native Food Delivery Environment

The Normalisation of Loss Leaders

How Platforms Are Innovating

Innovation on the Supply Side

Pinhaofan (拼好飯)

Innovation on the Demand Side

Shenqiangshou (神抢手)

God Coupon (神券)

Innovation on the Rider Side

The Four Main Delivery Models

The Infrastructure Layer

Meituan’s Initiatives and Micro-Warehouses

Micro-Warehouses

Micro-Warehouse Types

General Merchandise

Specialised Warehouses

Brand Warehouses

Meituan’s Advantages and Services

Alibaba, Taobao’s Advantages and Services

The Ecosystem Surrounding Quick Commerce Platforms

In-Store Services

To-Home Services

Traffic Platforms: Search and Discovery

Restaurants, Retailers, and Other Physical Shops

On-Demand Logistics

Closing: What China Teaches Us

The Current Players and Landscape in SEA Today

Grab Holdings

Sea Limited

TikTok Shop

Strategic Positioning: Three Different Plays

Core Business Model

Customer Acquisition & Frequency

Logistics Network & Fulfilment

Merchant/Seller Network

Monetisation and Revenue Streams

What It Takes to Win in SEA Quick Commerce

Southeast Asia vs China

How this Converges over the Next 5 Years

How Big can Quick Commerce be in Southeast Asia?

Why Southeast Asia Won’t See a China-Level Subsidy War Everywhere (Yet)

The End-Game for SEA Quick Commerce

Conclusion

1. Quick Commerce 101

Quick commerce refers to ultra-fast, on-demand delivery, typically fulfilling orders within 10 to 60 minutes by leveraging nearby retail stores or micro-warehouses.

Quick commerce first began with service-heavy categories like restaurants, and expanding into products that require more delicate handling, such as flowers and cakes. Today, thanks to the massive scale these platforms have accumulated, it has become cost-effective to deliver more commoditised, lower-margin products as well.

In China, quick commerce has now evolved into a broad retail channel. Platforms offer everything from clothing and electronics to groceries and everyday household items, effectively replicating the assortment of a local physical store, delivered within the hour.

Why Quick Commerce is Inevitable

At its core, the history of retail is a story of collapsing time and friction. Consumers have always traded up on convenience, moving from physical stores to e-commerce, from multi-day delivery to same-day, and now from hours to minutes. As cities become denser and consumers more smartphone-native, the distance between inventory and demand keeps shrinking, making ultra-fast delivery not just desirable but increasingly viable.

Once that infrastructure is in place, it is only natural for platforms to onboard more types of merchants that can leverage the same delivery system. As scale increases and delivery costs fall, and as micro-warehouses and local fulfilment hubs proliferate, an expanding range of products becomes economically viable for instant delivery.

More importantly, as consumers become accustomed to on-demand fulfilment in one category, their expectations reset across others, shifting behaviour from planned purchases to immediate consumption. This creates a virtuous cycle of higher frequency, better density, and lower unit costs, making the expansion of quick commerce less a strategic choice and more a structural inevitability.

In that sense, quick commerce is not a discretionary product decision, but the natural end-state of a scaled marketplace.

2. Quick Commerce in China

China’s quick commerce market operates at a scale that is difficult to replicate anywhere else in the world. In 2024, DoorDash, the largest player in the US, processed roughly 6.8 million orders per day. By contrast, Meituan and Alibaba’s quick commerce platforms each handle more than 70 million daily orders, around ten times of DoorDash’s volume.

By the end of 2025, quick commerce was running at roughly 180 million orders per day, with about 40 million coming from non-food categories. Because non-food categories have a much higher AOV, it now accounts for over 40% of the ~RMB 2.5 trillion (USD $350 billion) quick commerce market.

Population density is a major driver, but much of the credit has to go towards Chinese platforms, who have developed deep innovations across both supply and demand, enabling them to generate and sustain extraordinary order volumes.

We expect many of these playbooks to spread globally. For Southeast Asia in particular, China’s trajectory can be a helpful reference, given the region’s cultural proximity and strong links to Chinese culture and companies.

First, for readers new to China’s quick commerce landscape, here’s a brief overview of the main players.

Meet the Players

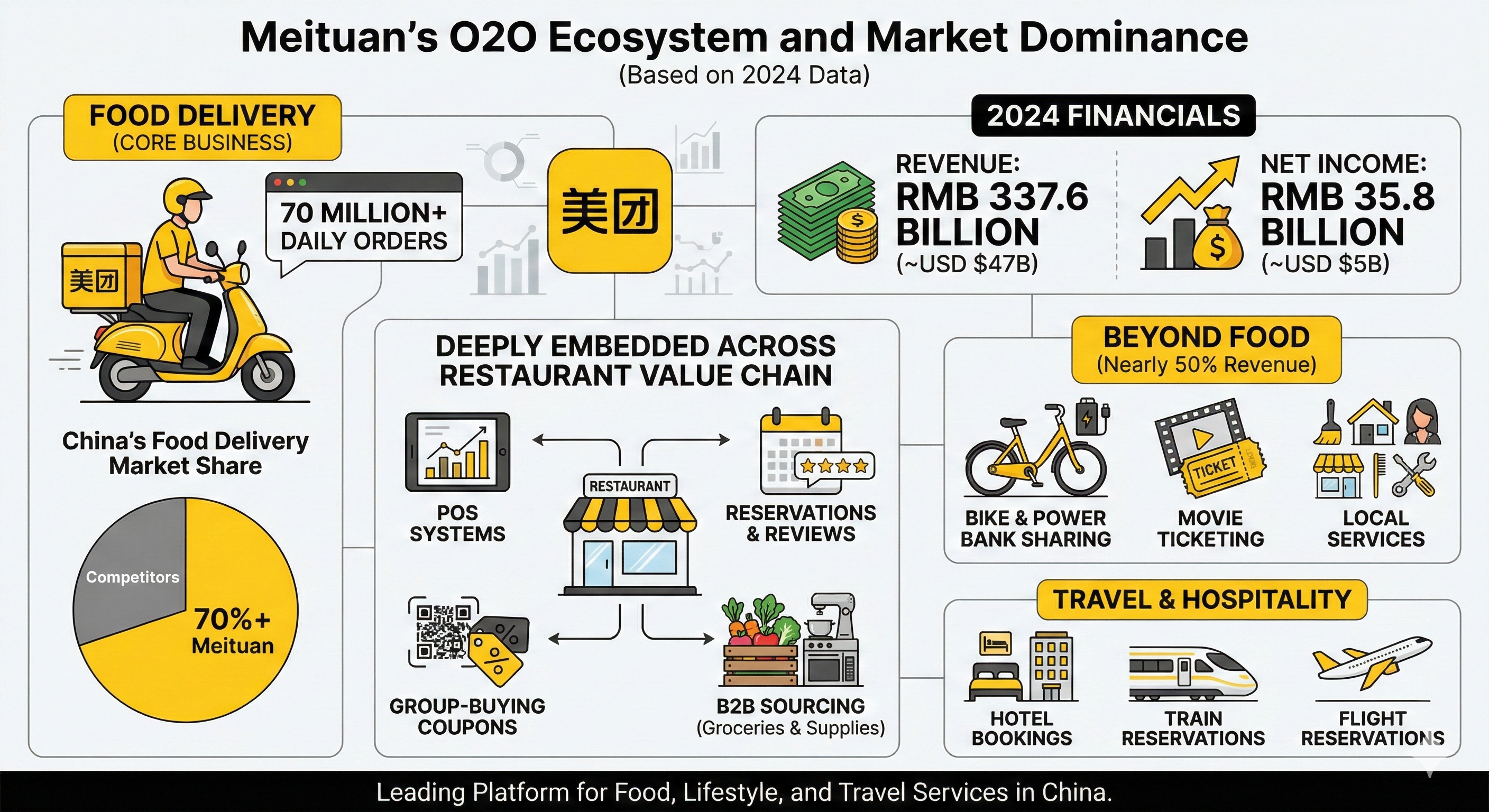

Meituan

Meituan is China’s leading food delivery platform processing over 70 million orders on a daily basis. In 2024, Meituan generated RMB 337.6 billion (~USD $47 billion) in revenue and over RMB 35.8 billion (~USD $5 billion) in net income. At the time, it controlled over 70% of China’s food delivery market, and notably, close to half of its revenue now comes from services beyond food delivery.

Meituan is deeply embedded across the restaurant value chain. It plays a meaningful role in POS systems, reservations, reviews, group-buying coupons, and is also a key platform for restaurants to source groceries and supplies. Beyond food, Meituan has also built a strong position across a wide range of O2O services, including bike and power bank sharing, movie ticketing, and local services. It is also an important player in travel, offering hotel bookings as well as train and flight reservations.

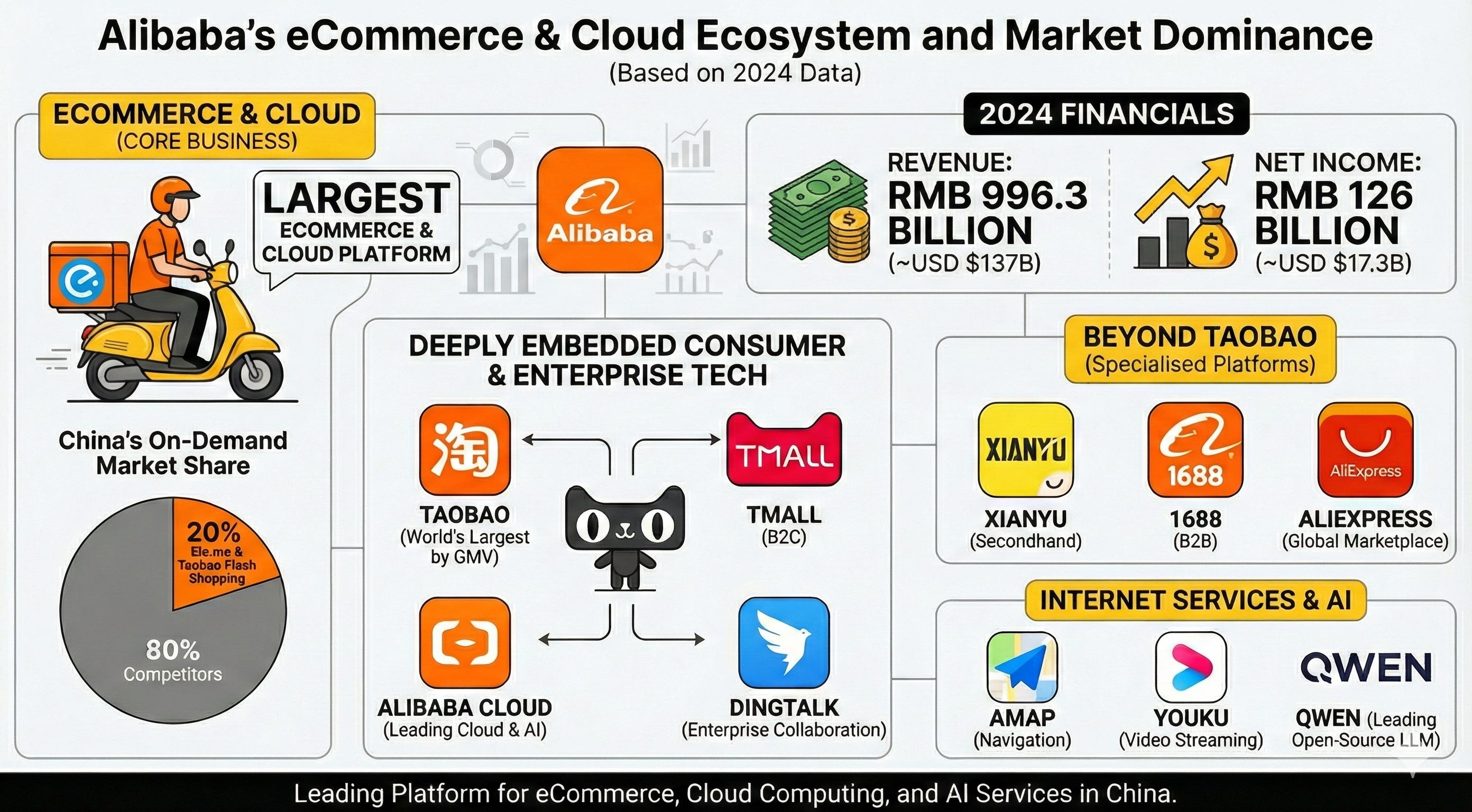

Alibaba

Alibaba is China’s largest e-commerce and cloud computing platform by both market share and profitability. It owns Taobao, the world’s largest e-commerce platform by GMV. Alibaba is also behind Qwen, a leading open-source large language model adopted by Airbnb and other Western companies.

In 2024, Alibaba reported revenue of RMB 996.3 billion (~USD $137 billion) and profits of RMB 126 billion (~USD $17.3 billion). Prior to the escalation of the quick commerce war, its food delivery platforms, Ele.me held roughly 20% market share.

Beyond Taobao, Alibaba operates a portfolio of specialised e-commerce platforms. Xianyu is a second-hand C2C marketplace with 200 million users. 1688 is a B2B marketplace with over 100 million users. AliExpress is a B2C marketplace focused on international markets. In addition, Alibaba also owns a broad suite of internet services, many of which exceed 100 million users. These include AMAP, Qwen, Youku, and Dingtalk, reinforcing Alibaba’s position as one of the most deeply embedded consumer and enterprise technology ecosystems in China.

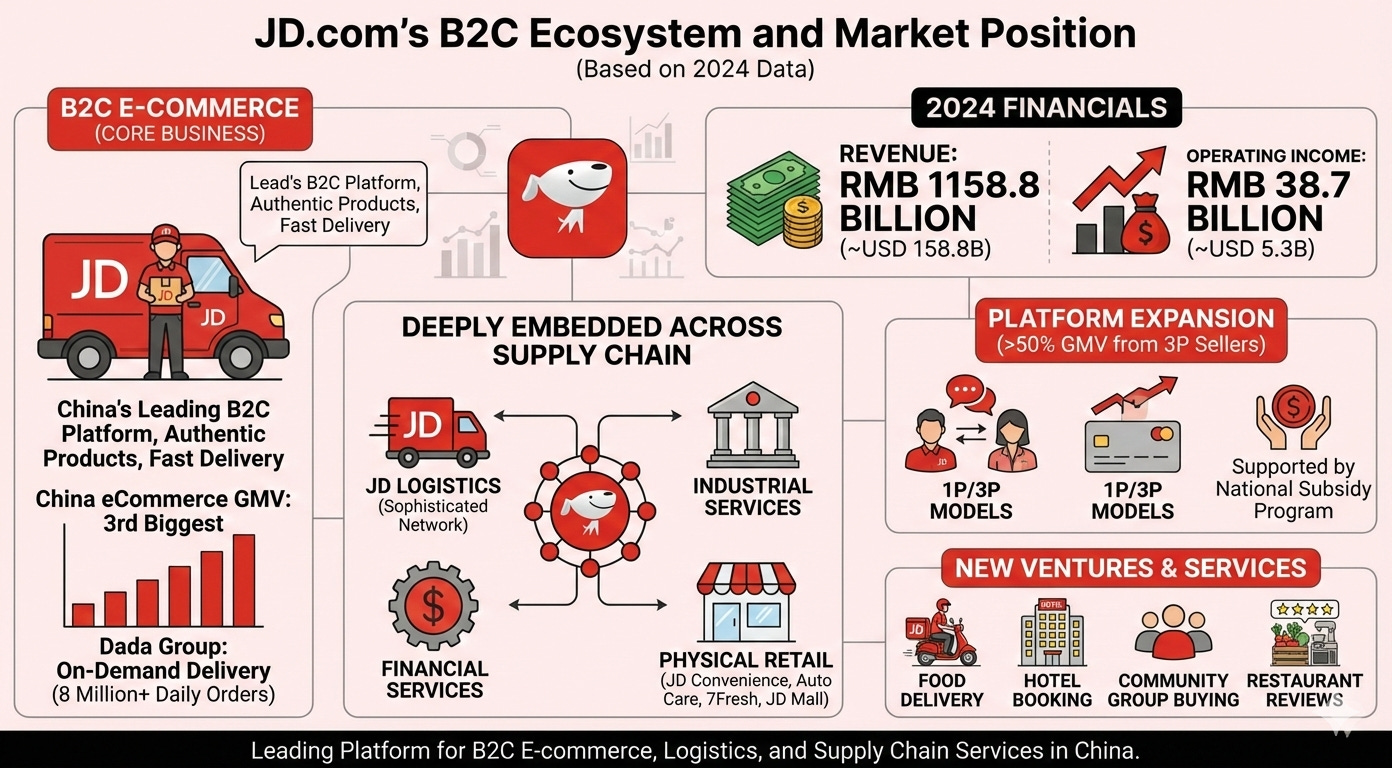

JD

JD is one of China’s leading B2C e-commerce platforms, widely recognised for its authentic products, high service standards, and consistently fast delivery. It has a particularly strong following among higher-income consumers who value reliability and quality.

Beyond retail, JD operates across a broad range of sectors. Its logistics arm, JD Logistics, is widely regarded as one of the most sophisticated logistics networks globally. JD also owns Dada Group, an on-demand delivery platform processing roughly 8 million orders per day. JD’s ecosystem spans the entire eCommerce supply chain, including industrial services, financial services, telehealth and physical retail through JD Convenience Stores, JD Health, JD auto care, 7Fresh, JD Mall, and more.

In recent years, JD has shifted from a purely self-operated model (1P) to a platform model (3P), with over half of its GMV now generated by third-party sellers. In the past year alone, it has expanded into food delivery, hotel booking, community group buying, restaurant reviews, and other new ventures. These bold moves have been supported by strong growth in its core e-commerce business, fuelled in part by the national subsidy program.

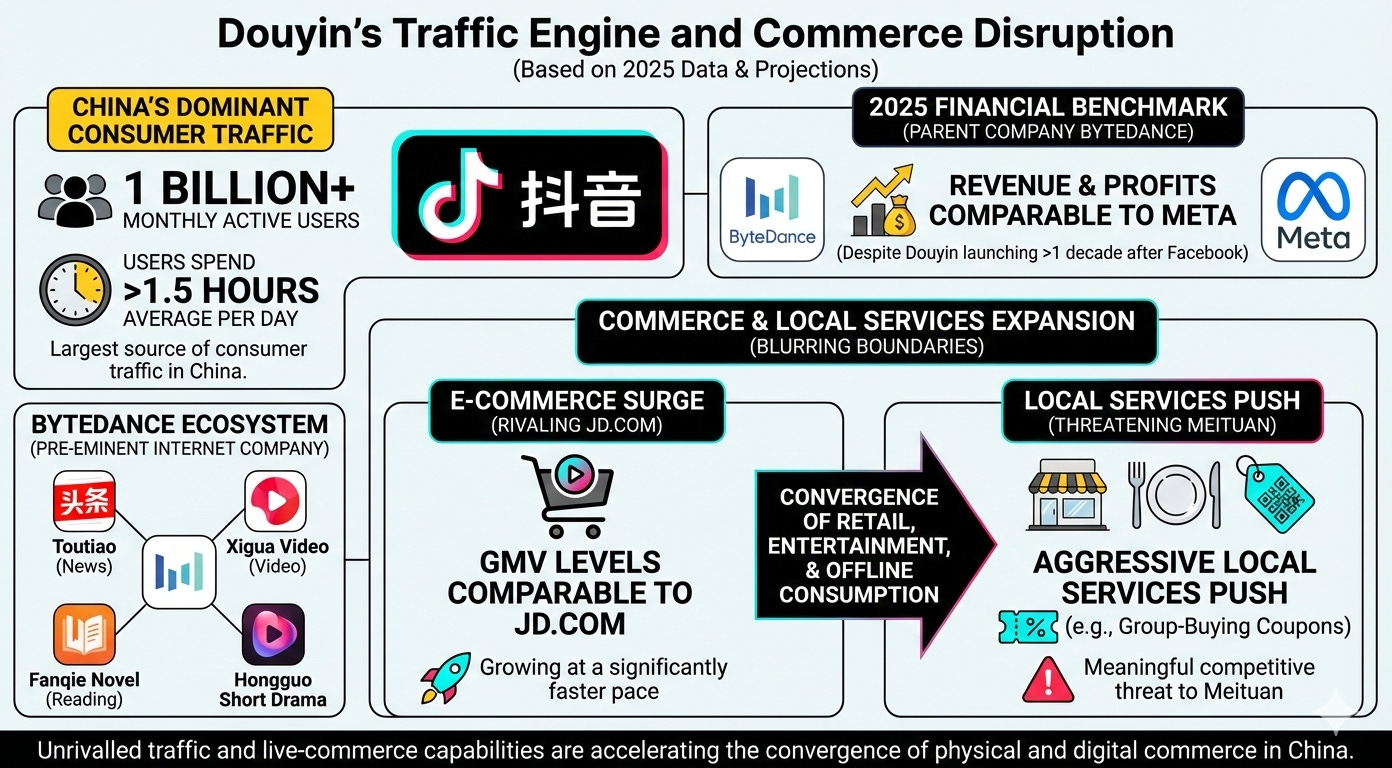

Douyin

Douyin is China’s domestic equivalent of TikTok. It is one of the largest sources of consumer traffic in China, with over 1 billion monthly active users. Users spend an average of more than 1.5 hours per day on the platform. Douyin is owned by ByteDance, which also owns several other traffic sites, including Toutiao and Xigua Video. Today, ByteDance is regarded as the pre-eminent internet company in China. For reference, its top and bottom-line in 2025 are comparable to Meta’s, despite its main product, Douyin, launching over a decade after Facebook.

On the commerce side, Douyin’s e-commerce business has reached GMV levels comparable to JD.com, while growing at a significantly faster pace. Its push into local services, including group-buying coupons, represents a meaningful competitive threat to Meituan. More broadly, Douyin’s unrivalled traffic scale and live-commerce capabilities are accelerating the convergence of retail, entertainment, and offline consumption, further blurring the boundaries between physical and digital commerce.

Pinduoduo

Pinduoduo is China’s second-largest e-commerce platform by GMV, best known for its affordable white-label products. In addition to its core business and global expansion through TEMU, Pinduoduo is also the country’s leading platform for agricultural goods. Its grocery service, Duoduo Maicai, is the largest community group-buying network in China. Operating on a next-day delivery model, it allows customers who place orders before midnight to receive their groceries before noon the following day.

S.F. Intra-city

S.F. Intra-city is a subsidiary of S.F. Express, China’s largest logistics company by revenue and a brand synonymous with premium service. As the leading third-party on-demand delivery platform by revenue, S.F. Intra-city now fulfils around 5 million orders per day and is the preferred instant-delivery partner for premium brands seeking high-reliability, time-critical fulfilment.

3. The Backstory of China’s Quick Commerce War

Much of the attention around China’s quick commerce war has centred on Meituan and Alibaba Group (via Ele.me and Taobao Flash Shopping). However, the company whose core value proposition is arguably under the greatest threat is JD.com.

JD was the first to escalate the conflict, formally kicking off the latest phase of competition in February 2025. Alibaba followed roughly three months later, announcing an initial RMB 50 billion (~USD $7 billion) investment into quick commerce. This raises an important question: why did JD start the war in the first place?

Why JD Lit the Match

JD is a leading B2C e-commerce platform in China, long recognised for its quick and reliable delivery. However, since Meituan’s aggressive push into quick commerce beginning in 2021, particularly across daily necessities and consumer electronics, JD’s delivery advantage has come under increasing pressure.

JD’s delivery edge was built on an extensive network of distributed warehouses and logistics hubs. By the end of 2024, the company operated more than 1,600 warehouses and over 19,000 logistics hubs nationwide, enabling delivery windows ranging from 4 to 48 hours. In fact, approximately 95% of first-party products are delivered within 24 hours.

Meituan, however, has pursued a different model. By partnering with hundreds of thousands of physical stores and rolling out more than 50,000 micro-warehouses, it has rapidly scaled infrastructure optimised for ultra-fast fulfilment.

For a growing segment of consumers, Meituan has become the default app for speed, with delivery times often under 30 minutes. As a result, JD has gradually lost mindshare around being the fastest option, a critical pillar of its historical differentiation.

By late 2024, over 300 million users had purchased non-food items through Meituan’s Flash Shopping service. Average daily volumes surpassed 10 million in Q3 2024 and has continued to grow rapidly. Peak daily orders reached 18 million in April 2025 and surged to 25 million by August 2025.

In effect, Meituan’s expansion began to encroach directly on JD’s core promise. JD’s decision to initiate the quick commerce war was therefore defensive as much as it was offensive.

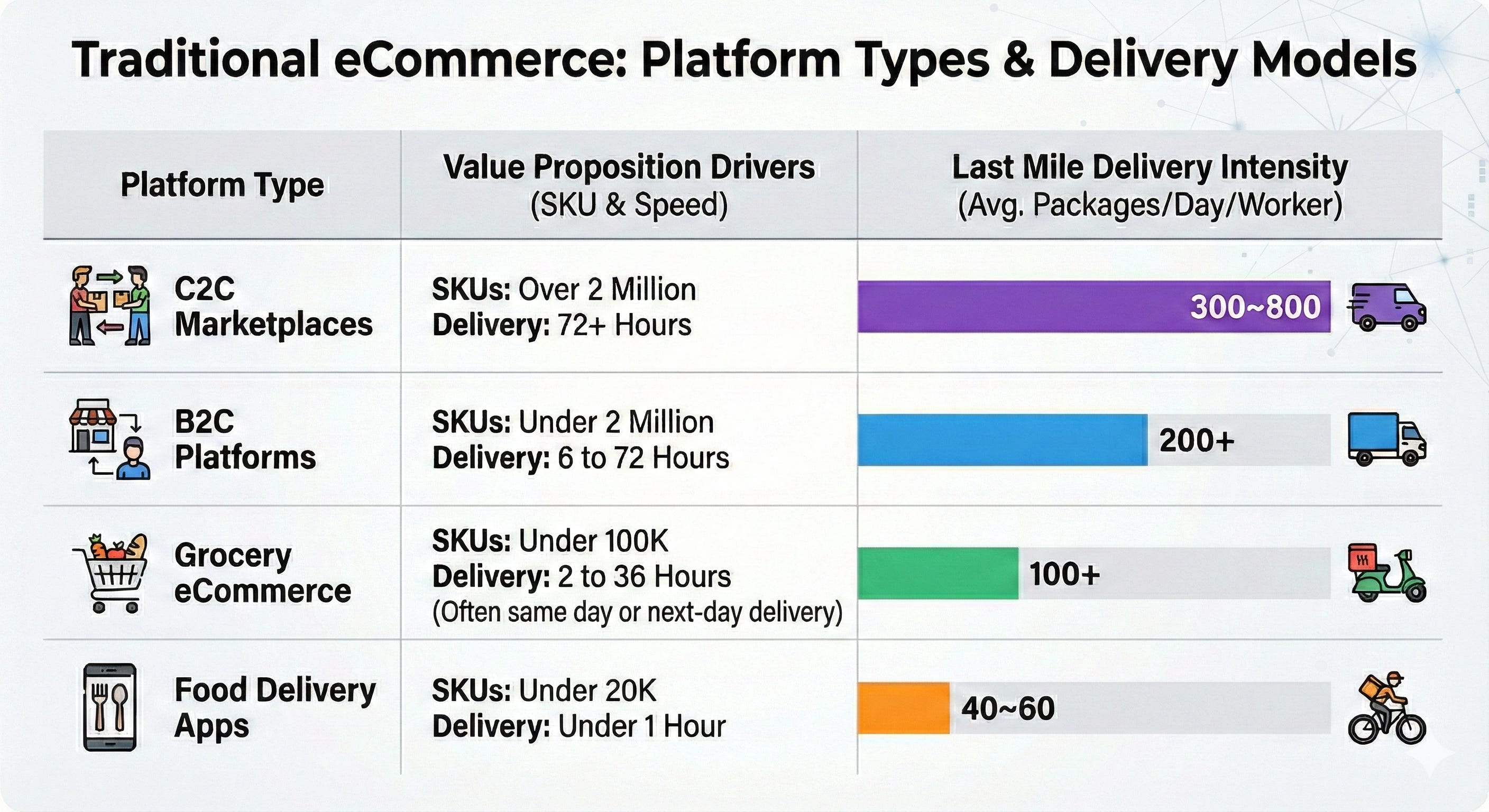

The Convergence of Four E-Commerce Logistics Models

In traditional e-commerce, there are four main platform types, each paired with a different delivery model that reflects its unique value proposition.

C2C marketplaces: Over 2 million SKUs – Delivers in 72+ hours - last mile workers deliver 300-800 packages on average per day

B2C platforms: Under 2 million SKUs – Delivers in 6 to 72 hours - last mile workers deliver 200+ packages on average per day

Grocery e-commerce: Under 100K SKUs – Delivers in 2 to 36 hours, often next-day - last mile workers deliver 100+ packages on average per day

Food delivery apps: Under 20K SKUs – Delivers in under 1 hour - last mile workers deliver 40-60 packages on average per day

In China, as logistics infrastructure has rapidly matured, the boundaries between these networks have begun to blur. Sellers on C2C platforms have become increasingly commercialised and operationally sophisticated, enabling much faster fulfilment. Many orders that once took more than 72 hours are now delivered in under 24 hours, especially in Tier-1 cities.

This evolution has narrowed the speed gap between C2C and B2C. The traditional strength of B2C logistics, speed, is no longer a clear advantage.

A key structural constraint for B2C logistics, however, is that warehouses are typically located in suburban areas. This creates inherent limits on delivery speed due to distance and the need for batch-based distribution. For JD to improve its delivery time meaningfully, it will likely need to adopt a new logistics model that breaks this bottleneck.

4. How the War is Being Fought

JD’s Push into a New Logistics System

JD Logistics, a publicly listed company majority-owned by JD.com, fully acquired DADA Group in Q2 2024. DADA had already been a listed subsidiary of JD prior to the transaction, but was not fully owned. In October 2024, JD.com then acquired DADA from JD Logistics, bringing the asset directly under the group’s control. Shortly after, in February 2025, JD launched its own food delivery service leveraging DADA’s capabilities.

DADA is an on-demand delivery platform that helps retailers and brands fulfill instant delivery orders. Major chains such as Yonghui Supermarket (永辉超市), Walmart, and Carrefour rely on DADA for their on-demand fulfillment needs. As of Q3 2024, DADA was handling approximately 7 million orders per day.

By fully integrating DADA and launching its food delivery business, JD built its “new” logistics network to compete head-to-head with Meituan’s quick commerce business.

JD first launched its food delivery service within the JD app, leveraging its existing traffic and offering aggressive subsidies to attract both restaurants and consumers to the newly formed marketplace. It focused on onboarding “high-quality” restaurants and hired more than 150,000 full-time delivery workers to support the operational workload.

Achievement Highlights:

March 1: Surpassed 1M orders per day – Initial launch, with a zero-commission policy attracting merchants

April 15: Peaked at over 5M orders per day – CEO Richard Liu personally delivered orders; JD launched a RMB 10 billion subsidy campaign

April 22: Peaked at over 10M orders per day – Reached this milestone just 70 days after launch

May 14: Peaked at over 20M orders per day – Approached the scale of the second-largest player in just 75 days

June 18: Peaked at over 25M orders per day – Set a yearly high during the 6.18 shopping festival

JD now appears to be stabilising at around 11 million orders per day if exclude orders from its third-party DADA Group.

Alibaba Joins the War

Alibaba Group was the primary challenger to Meituan in China’s on-demand market long before JD escalated the latest phase of the quick commerce war. With deeper roots in local services and the financial firepower of its core e-commerce business, Alibaba has since displaced JD as the market’s “new” challenger.

This rivalry is not new. In fact, Alibaba was once a major investor in Meituan. The relationship began to deteriorate after Meituan aligned itself more closely with Tencent in 2015. Alibaba responded by backing Meituan’s main rival, Ele.me, before fully acquiring the company in 2018.

Despite committing more than USD 10 billion to the effort, Alibaba failed to arrest Meituan’s rise. Between 2016 and 2020, Meituan’s food delivery market share expanded from roughly 35% to over 70%, while Alibaba’s delivery arm struggled to gain traction. To date, Alibaba’s on-demand delivery business has yet to achieve profitability.

Will Alibaba Succeed This Time?

No one knows how this round will ultimately play out, but several factors make this cycle meaningfully different.

Firstly, Alibaba is finally entering the war with the full weight of its core business rather than merely using Ele.me to fight the proxy war. Taobao has folded food delivery directly into its e-commerce group and fully embedded Ele.me into the Taobao user experience. Ele.me has been rebranded as Taobao Flash Sale, given priority placement, and elevated to a first-class traffic destination within Alibaba’s ecosystem.

Second, the external environment has improved significantly. Regulators have moved to curb practices that forced restaurants and other third-party sellers to choose sides, and after years of industry standardisation, most restaurants now list on both Meituan and Ele.me. This has lowered switching friction and made multi-platform competition far more viable than in previous cycles.

Lastly, Alibaba’s internal posture has shifted. Under new e-commerce CEO Jiang Fan, and with legendary founder Jack Ma once again closely involved, the company’s willingness to invest aggressively has clearly increased. Capital allocation, execution intensity, and competitive ambition are all operating at a level not seen in recent years.

Meituan and Alibaba’s Competitive Advantage

Meituan’s moat is primarily driven by powerful three-sided network effects across merchants, consumers, and riders, and it holds a clear competitive advantage in all three. Scale on the demand side attracts more merchants, greater merchant density improves selection and pricing, and higher rider density lowers fulfillment times and unit economics, reinforcing the flywheel.

That said, Alibaba Group enters the battle with a different set of strengths. First, it has a significantly larger war chest, giving it greater capacity to sustain subsidies and long-term investment. Second, Alibaba has access to a much broader base of e-commerce users through Taobao, many of whom can be converted into quick commerce users at relatively low marginal cost. Third, Alibaba maintains deep, long-standing relationships with pure-play e-commerce sellers and major brands, providing a structural advantage as quick commerce expands beyond food into higher-value, branded retail categories.

Meituan’s Advantages

Although Alibaba and Meituan offer access to a broadly similar merchant base, Meituan’s relationships with restaurants are far deeper and more structural.

On the merchant side, Meituan controls a significant share of the restaurant POS market and is a major driver of in-store demand through group-buying coupons. It has also worked closely with many restaurant operators to launch cloud kitchens and develop platform-exclusive menu items tailored specifically for on-demand consumption. In addition, Meituan owns Dianping, China’s largest restaurant review platform, and KuaiLu, a leading grocery replenishment platform for restaurants. Together, these assets embed Meituan deeply into daily restaurant operations, not just order fulfillment.

On the rider side, Meituan has built a highly mature and disciplined delivery network. A large portion of its riders are managed by experienced franchise operators who oversee full-time couriers. These franchise-managed riders form the backbone of Meituan’s stable, high-efficiency delivery system, contributing to consistent service quality and reliable fulfilment.

On the consumer side, Meituan has spent years refining its unit economics by actively identifying profitable users and deprioritising those that are structurally loss-making. As a result, Meituan has a clear understanding of which users contribute positively to long-term profitability. Unlike Alibaba, which is currently subsidising a large proportion of orders more indiscriminately, Meituan takes a far more selective approach, targeting incentives primarily at users with attractive lifetime value.

This filtering mechanism extends beyond consumers to merchants and riders as well. Over time, weaker operators are naturally pushed out, leaving Meituan with a higher-quality base of restaurants and a more reliable rider network than its competitors.

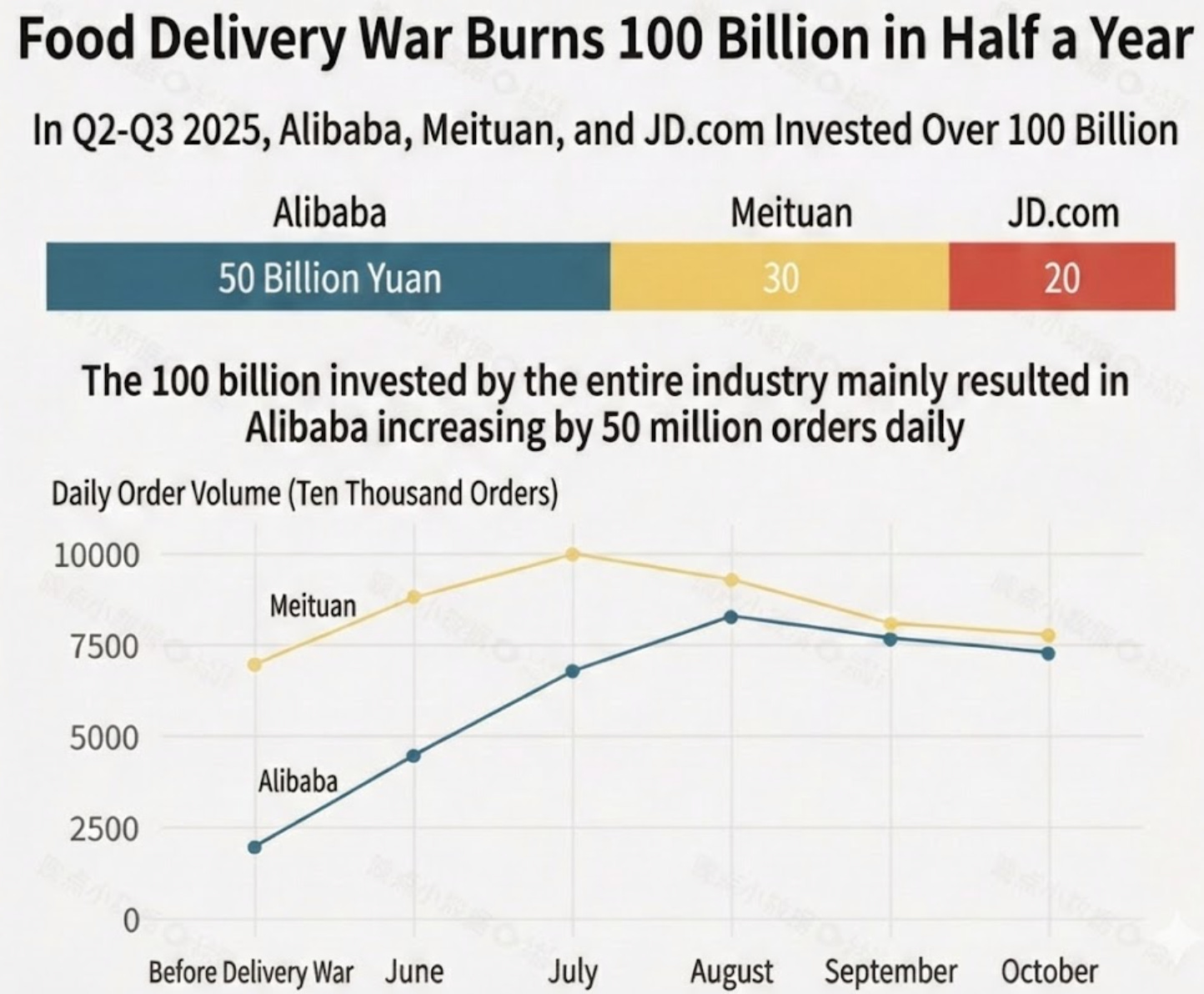

5. The Current Status of the War

As of the latest earnings calls, the three major players have collectively accumulated around RMB 100 billion (~USD $14 billion) in losses over Q2-Q3 2025. In recent months, daily order volumes have stabilised at roughly 75 million for Alibaba, 75 million for Meituan, and around 11 million for JD.

GMV Market Share: Alibaba v. Meituan

From May to September, Alibaba grew its daily order volumes to a level similar to Meituan’s. Despite this surge in volume, the GMV split between Meituan and Alibaba has remained broadly stable at around 6:4. Including JD in the comparison, Alibaba’s GMV share remains below 40%, while Meituan continues to hold just above 50%.

This gap exists because Alibaba’s orders are mostly low-value transactions. In August 2025, its average order value was estimated to be around RMB 15-20, and at the peak of promotional activity, more than half of all orders came from bubble tea and coffee shops.

By contrast, Meituan continues to dominate higher-value orders. In the third quarter, Meituan accounted for more than 66% of orders above RMB 15 and around 70% of orders above RMB 30. This reflects a structurally stronger position in higher-ticket categories and helps explain why Meituan has been able to defend its GMV share despite aggressive competitive spending across the industry.

China’s Food Delivery Unit Economics (Pre-War)

In China, the average rider cost per order is about 7 yuan, and the platform’s gross take rate (including commissions, delivery fees, advertising, etc.) is roughly 25%. This implies that the platform needs an average order value of at least 28 yuan to break even.

Before the subsidy war began, China’s average order value hovered around RMB 45–50. With rising order volumes, new operational initiatives, and a gradual reduction in subsidies, Meituan has successfully turned quick commerce into a highly profitable business.

Over the past three years, Meituan’s operating profit per order has been:

2022: ~1.05 yuan

2023: ~1.2 yuan

2024: ~1.4 yuan

In 2024, Meituan achieved operating profits equivalent to about 4% of food delivery GMV with a gross take rate of only around 25%. By comparison, despite an estimated 30-35% gross take rate, DoorDash captures only about 1% of GMV as profit. Grab’s gross take rate is around 35%, yet its segment adjusted EBITDA margin is roughly 2% of GMV.

Meituan is therefore at a meaningfully later stage of the monetisation curve.

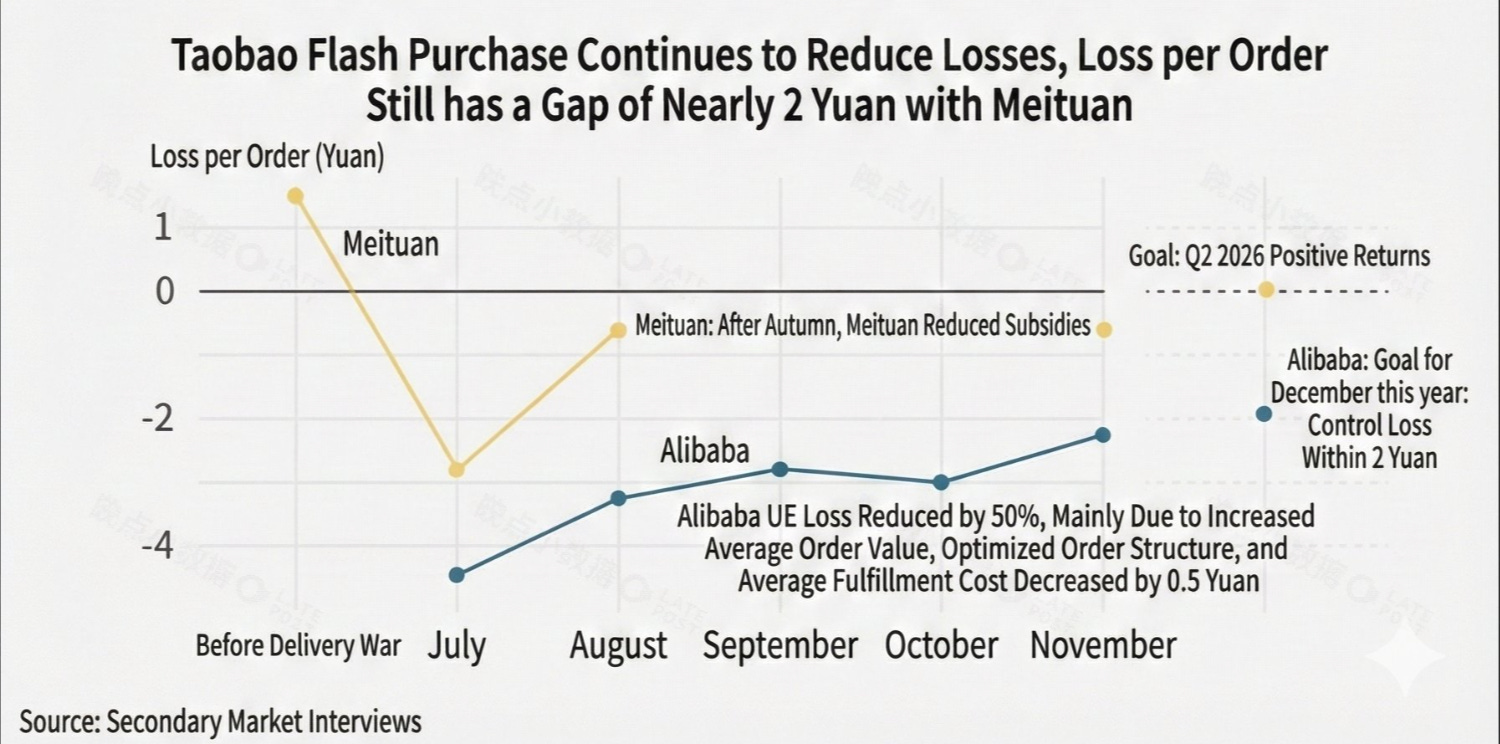

China’s Food Delivery Unit Economics (Post-War)

In Q3 2025, Meituan’s delivery business is estimated to have recorded a loss of around RMB 20 billion ($2.8 billion USD), compared with roughly RMB 36 billion ($5 billion USD) for Alibaba. Despite operating at similar order volumes, Alibaba’s loss per order is still about 2.1x that of Meituan’s. In other words, there remains roughly a RMB 15 billion ($2 billion USD) gap in cost structure even at comparable scale.

That said, Alibaba has been actively optimising its unit economics, and its AOV mix has improved substantially. Average order value has grown at a double-digit rate, and less than 25% of orders now come from bubble tea and coffee shops. Alibaba’s loss per order has been cut roughly in half from the lows seen in July. Even so, there remains a gap of roughly RMB 2 per order versus Meituan, underscoring the persistence of Meituan’s structural efficiency advantage.

The Difference in Unit Economics

The difference in unit economics comes down to two key factors:

The delivery network

The core user base of each platform

Delivery Network

First, Meituan’s delivery network is still meaningfully more efficient. This is partly due to its data advantages in batching and routing, and partly because Meituan operates a larger, more experienced base of full-time franchise operators and riders.

These franchise-managed, full-time riders form the backbone of a more disciplined and predictable delivery system, which translates into higher utilisation and lower cost per order. (We will discuss the franchise and full-time rider model in more detail shortly)

Core Users of the Platform

Over the past few years, Meituan has been refining its unit economics by actively identifying profitable users and deprioritising those that are structurally loss-making. As a result, Meituan has a much clearer understanding of which users contribute positively to long-term profitability.

Unlike Alibaba, which is currently subsidising a large proportion of orders more indiscriminately, Meituan takes a far more selective approach, targeting incentives only at users with attractive lifetime value. In 2025, depending on a customer’s VIP tier, core spenders receive meaningfully larger discounts on the same orders, reinforcing this focus on high-quality demand.

6. What are they Fighting for?

There are two main prizes at stake:

The fast-growing quick commerce market

The traffic spillover from bundling quick commerce with existing platforms

The Quick Commerce Market

In 2024, the market size of e-commerce in China overall is about 16 trillion yuan (~ USD $2.3 trillion). Food delivery alone accounted for around 1.35 trillion yuan (~ USD $193 billion), while non-meal quick commerce was approximately 780 billion yuan (~ USD $110 billion). Combined, the broader quick commerce market was therefore worth about 2.1 trillion yuan (~ USD $300 billion).

While China’s overall e-commerce market has been relatively stagnant, the non-meal quick commerce sector has seen explosive growth, with a CAGR of around 46% from 2019 to 2024, and is expected to grow a further 20-30% in the coming years. It is becoming an increasingly large part of the pie, and it is likely only a matter of time before it surpasses traditional food delivery in scale. Alibaba’s CEO has been explicit about this, stating on the Q2 2025 earnings call that quick commerce is expected to contribute around 1 trillion yuan in incremental GMV over the next three years.

For Alibaba and JD, even though quick commerce still accounts for only about 5% of the eCommerce market today, its expanding selection and improving value proposition represent a growing strategic threat. For example, Meituan is now offering an increasingly broad range of electronics and branded products that were traditionally only available in physical stores or through conventional e-commerce platforms.

Traffic Spillover

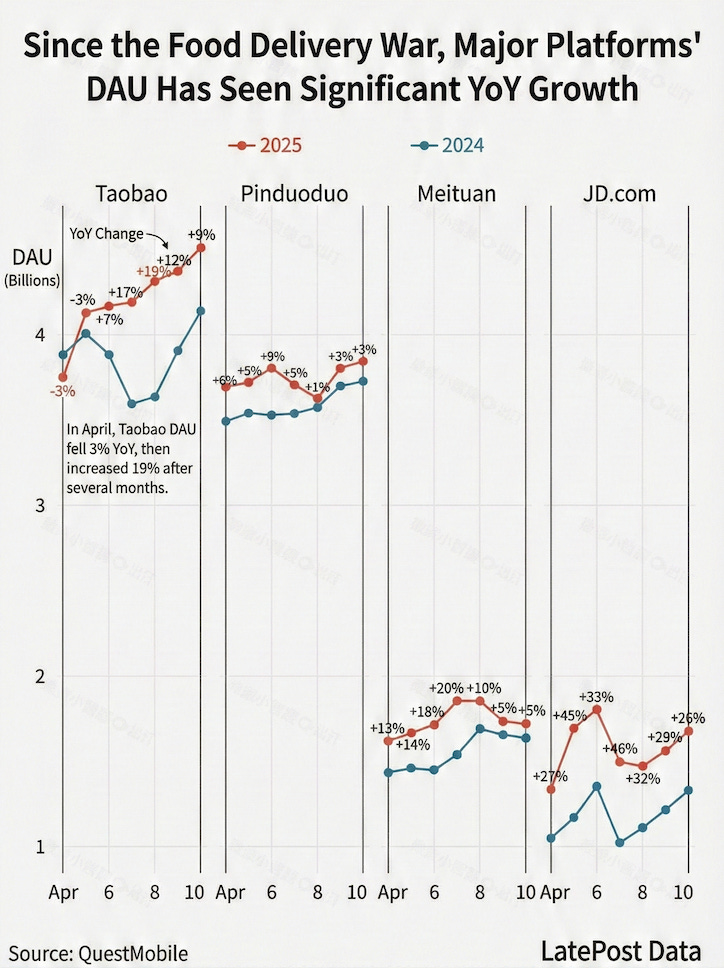

It is a well-known strategy that bundling products or features increases user retention and usage. Amazon Prime, Microsoft Office, and Meituan’s own super-app ecosystem are all built around this logic. Alibaba and JD are similarly hoping that by bundling quick commerce into their platforms, users will also increase their engagement with their core e-commerce offerings.

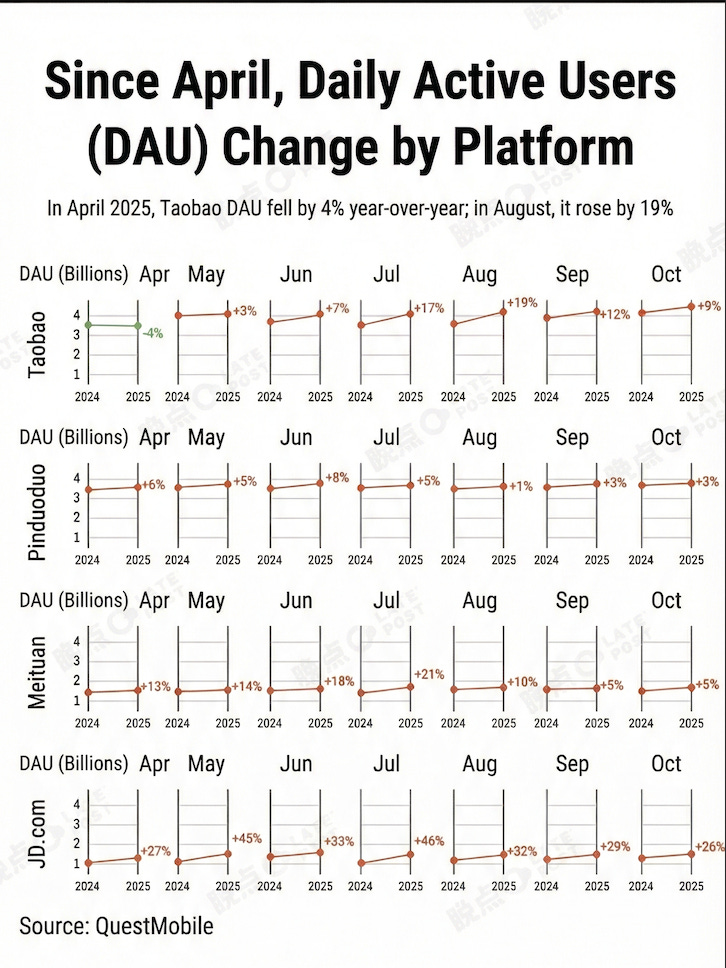

Since the subsidy war began, both JD’s and Alibaba’s DAU have indeed risen by a meaningful amount. For now, however, the bundling of quick commerce into the core offerings does not appear to have had a meaningful impact on core sales yet.

The Different Approaches of Alibaba vs. Meituan

Alibaba and Meituan are approaching quick commerce from fundamentally different starting points.

For Alibaba, the goal of rolling quick commerce into Taobao is primarily to enhance the delivery experience for the same products already sold on its platform. For Meituan, the focus is more on expanding SKUs and merchant coverage to better serve users using the same underlying on-demand delivery network. This leads to two very different ways of building the business.

Alibaba effectively segments products into three categories:

Urgent needs: delivered within 30 minutes

High-intent needs: fulfilled within 4 hours / same day

Other products: shipped through the traditional e-commerce logistics system

Meituan, by contrast, is far more singular in its ambition: 30-minute delivery for as many categories as possible. They also treat food delivery very differently. For Alibaba, restaurant orders are primarily a way to lower the marginal cost of operating an on-demand network, with the ultimate goal of better monetising non-food categories.

This is why, after scaling restaurant orders, Alibaba has increasingly shifted its focus toward non-food products. For Meituan, restaurant orders are the core of the business, and the company continues to double down on this segment as its foundation.

Quick Commerce Market in 2024

Within the roughly 780 billion yuan quick commerce market, the competitive landscape can be broadly divided into three tiers:

Meituan

JD and Ele.me

Other players

Meituan alone fulfilled over 270 billion yuan in GMV, implying a market share of around 35%. JD and Alibaba’s Ele.me each held roughly 10% market share. The remaining players, including Alibaba’s Freshippo, Sam’s Club, Dingdong and various other independent retailers, collectively accounted for around 45% of the market.

In 2024, Alibaba’s Ele.me, Taobao’s one-hour delivery, and Freshippo were still largely operated as separate businesses. Many third-party orders were fulfilled either by merchants’ own fleets or outsourced to independent on-demand delivery platforms such as DADA Group or S.F. Intra-city.

What has Changed in 2025?

The most important shift is that Alibaba has started to integrate these previously separate businesses, and has begun to replace parts of its original delivery fleet with Ele.me’s workforce.

Second, before Alibaba launched aggressive subsidies, many quick commerce merchants chose not to sell on Ele.me because the traffic was not worth the added operational complexity. With the new subsidy push, more sellers are now choosing to serve both platforms.

In recent months, Meituan’s non-food orders have stabilised at around 18 million per day, with average order volume growing roughly 80% year-over-year. Meanwhile, Taobao has surpassed 10 million average daily orders, with active buyers growing by around 200%. (10M orders include Tmall Supermarket orders/Freshippo orders, if exclude it’s 7M)

What are the Limits of Quick Commerce?

The biggest limiting factor for quick commerce is selection. To achieve 30-minute delivery, products must be stored within roughly a 3-mile radius of the customer. This makes the model capital-intensive and operationally demanding, requiring a very high level of service quality.

Today, even in the city centres of China’s Tier-1 cities, the available selection is only around 200,000 SKUs (we will discuss micro-warehouses in more detail shortly).

Because of storage constraints and the promise of rapid delivery, pricing in quick commerce is generally less competitive than in traditional e-commerce. The shopping experience in some verticals such as apparel and electronics is also still weaker. Customers may receive the wrong item, or products that have been returned or previously used. It will likely take several more years of operational refinement before the overall experience reaches parity with traditional e-commerce.

7. The Next Stage of the War & Other Players

Taobao and Meituan are both platforms that are primarily driven by search intent, but the nature of that intent differs. On Meituan, search intent is mostly concentrated around food delivery, groceries, and urgent needs. On Alibaba, by contrast, most users come for long-tail SKUs and broader selection.

For now, quick commerce is still largely centred on food delivery. This is because the infrastructure for long-tail quick commerce remains relatively primitive. Most brands still do not store inventory close to end consumers, even though both Taobao and Meituan are aggressively building this capability. It will likely take several more years before the product experience for long-tail, instant fulfilment becomes truly smooth and reliable.

While Meituan, Alibaba, and JD are the three main players today, companies like Douyin and Pinduoduo are also testing, or have already launched, related offerings in this space. On-demand commerce is simply too important a battleground for major e-commerce platforms to ignore.

AI Search & Qwen

Qwen is Alibaba’s equivalent of ChatGPT and has now surpassed 100 million monthly active users. It is deeply integrated across Alibaba’s apps. In my personal experience, the food ordering flow through Qwen is already very smooth.

Large language models could become a meaningful traffic driver for quick commerce by changing how users search and discover products. During the 2/6 promotion, Qwen reportedly fulfilled one million bubble tea orders within three hours, highlighting the potential of AI-driven interfaces to reshape demand distribution.

Regulators & Platform Subsidies

There has been increasing noise from regulators around curbing excessive competition in the quick commerce space. In our view, the government is not trying to stop competition between platforms per se, but rather to limit the abuse of platform traffic power to force merchants into unsustainable subsidy wars.

China’s Quick Commerce Subsidies

An interesting shift has occurred compared to the early days of ride-hailing and food delivery in the 2010s. Back then, restaurants generally welcomed platform competition because platforms were subsidising both merchants and consumers aggressively.

This time is different. Many restaurants are now under significant pressure. As platforms have gained more control over traffic distribution, they have increasingly used that leverage to force merchants to co-fund subsidies. When all major platforms adopt the same practice, merchants effectively have no choice.

Regulatory intervention is therefore aimed at preventing platforms from dragging merchants into a race to the bottom, and at ensuring that merchants are not the primary losers in the subsidy war. Before regulators stepped in, for every dollar a platform subsidised, merchants often had to contribute roughly three dollars. For example, if a platform offered a four-dollar coupon, the merchant would typically be required to fund three dollars of that discount.

8. What makes China’s Instant Logistics Special? How Do Platforms Aggregate So Much Volume?

To understand the efficiency of Meituan’s instant logistics model, two structural factors matter above all else.

First, China’s urban design and restaurant ecosystem are unusually well-suited to food delivery. Many cities are built around electric scooters, and the restaurant environment itself is optimised for delivery. This creates what could be described as a native food delivery environment.

Second, and more importantly, platforms relentlessly aggregate both demand and supply. This combination drives extremely high utilisation. For instance, it is normal for a rider to complete around 8-9 deliveries per working hour, a level of density that is difficult to replicate elsewhere.

A Native Food Delivery Environment

In China, many cities and road networks are designed with electric scooters in mind, which are ideal for food delivery. Most restaurants now offer menus specifically tailored for delivery, and in some cases, ordering delivery is actually cheaper than dining in-store.

Ghost kitchens and cloud kitchens are also widely used, producing food solely for delivery platforms. In addition, many shopping malls and food plazas have dedicated parking areas for riders, and sometimes even internal corridors designed to speed up order pickup. At the destination, office buildings and residential complexes often provide delivery lockers or shelves where riders can drop off orders efficiently.

Today, dark kitchens alone account for roughly 30% of total food delivery orders.

The Normalisation of Loss Leaders

In China’s ultra-competitive environment, e-commerce platforms are deeply familiar with the concept of loss leaders. Loss-making orders are treated as a marketing expense to boost user frequency, expand scale, and suppress competition.

As a result, a meaningful portion of orders across most platforms is structurally unprofitable. This is not seen as a failure, but as a deliberate strategy to build habit, density, and long-term competitive advantages.

9. How Platforms Are Innovating

Innovation on the Supply Side

Meituan is a good example of how platforms innovate on the supply side. It increasingly treats kitchens like factories: standardised, digitised operations designed to produce meals at lower cost and higher consistency.

To support this, Meituan operates across the restaurant value chain:

KuaiLu: helps restaurants replenish groceries faster and at lower cost

POS systems: help restaurants track costs, participate in promotions, and digitise daily operations

Raccoon Kitchen and branded satellite stores: help strong restaurants scale through site selection and cloud-kitchen formats while lowering operating costs

Redeemable flash-sale coupons: aggregate demand during off-peak periods to boost utilisation

Together, these tools help restaurants scale more efficiently while keeping prices competitive. But Meituan does not stop at being just a tool provider, it increasingly intervenes directly in food supply itself.

Pinhaofan (拼好飯)

Pinhaofan, launched in 2020, is one of the clearest examples of Meituan stepping directly into the supply side. It is often described as the Pinduoduo group-buying model for food delivery, and today contributes a double-digit share of Meituan’s total orders.

Meituan initially launched Pinhaofan in lower-tier cities, targeting more price-sensitive consumers, before gradually expanding it nationwide. The model is relatively simple. Meituan selects a small number of popular dishes such as “Beijing Duck” or “Dumplings”, and then partners with restaurants in each region to produce them. Meituan guarantees a fixed purchase price to the restaurant and sets the final retail price itself.

In effect, this turns restaurants into outsourced production units for the platform. The final price, including delivery, typically ranges between 10-15 yuan (about USD 1.50-2.10) for a full meal.

Meituan loses money on most Pinhaofan orders. But this is a deliberate choice, it keeps users engaged, increases order frequency, and helps the platform build the scale and density that underpin its logistics efficiency.

Innovation on the Demand Side

Shenqiangshou (神抢手)

Shenqiangshou is one of Meituan’s initiatives that packages restaurant meals into products designed to be sold through live streaming, short videos, newsfeeds, and other discovery-driven channels. The goal is to standardise what is usually highly customised and difficult to forecast, making both demand and sales more predictable. This allows restaurants to reach customers through both traditional intent-based ordering and discovery-based browsing. Today, Shenqiangshou accounts for a double-digit share of Meituan’s total orders.

God Coupon (神券)

God Coupon is Meituan’s coupon-driven traffic allocation system. It further segments in-app traffic by grouping customers based on their behaviour and their familiarity with the app. Users receive different offers based on past behaviour, and the system also rewards those who actively engage with and learn how to use the platform. The result is effectively personalised pricing for each customer.

Compared with traditional VIP programmes, the key difference is that VIP discounts are usually static: members receive predictable discounts tied to their membership tier, and merchants provide additional discounts based on that level. God Coupon, by contrast, uses dynamic, behaviour-based incentives.

On the merchant side, restaurants can opt into different programme tiers depending on how much discount they are willing to offer for specific customer segments and dishes. Meituan then matches those coupons to the right users to improve overall conversion.

Overall, this system helps Meituan allocate demand more efficiently across different restaurants and user segments.

Innovation on the Rider Side

A key difference between Meituan and many Western delivery platforms is that Meituan places far greater emphasis on rider experience and familiarity. Unlike Western platforms, which rely primarily on data metrics and batching algorithms to manage service quality, Meituan uses a franchise-partner network to manage full-time couriers, smooth capacity swings, and maintain consistent service levels.

Meituan also groups gig couriers into tiers. The core idea of this system is to route different types of orders, often segmented by price and context, to couriers who repeatedly operate in similar environments, allowing them to build familiarity over time. This familiarity allows an experienced delivery to be nearly twice as productive as a new worker.

The Four Main Delivery Models

In practice, Meituan operates four main delivery models (which you can think of as funnels):

Chang Pao 暢跑(freelance, priority access)

Riders can pick orders first, so the easier orders usually land here.

It’s common to complete 8-9 orders per hour.

Pros: very flexible hours; usually stays busy

Cons: low pay per order (about 3.5-5.5 yuan); physically demanding; you may not see the final pay for an order until the next day

Exclusive 專送(full-time, franchise-managed)

Full-time riders are the backbone of the network, managed through franchises (typically 50-150 riders per franchise).

Pros: base salary; more balanced order volume; better learning from experienced riders

Cons: assigned orders (no picking, and can include undesirable orders); work continues regardless of weather

Le Pao 樂跑 (part-time support for peak periods)

Similar to the Exclusive model, but mainly used to help balance volume during peak seasons (e.g., summer or major promotions).

Overflow freelancers 純眾包(used for residual orders)

The platform typically uses this group to handle orders that remain after the main funnels are covered.

In addition, Meituan operates smaller, specialised funnels for fragile items (such as flowers and cakes), expedited deliveries, longer-distance orders, and riders assigned to specific stores, among others.

10. The Infrastructure Layer

Meituan’s Initiatives and Micro-Warehouses

For quick commerce to scale beyond food, Meituan needs to strengthen the supply side of its marketplace. It cannot rely solely on existing physical retailers. It also needs fast, reliable inventory positioned close to consumers. This is why Meituan has been building a network of urban micro-warehouses to fulfil orders more quickly and more consistently.

Micro-Warehouses

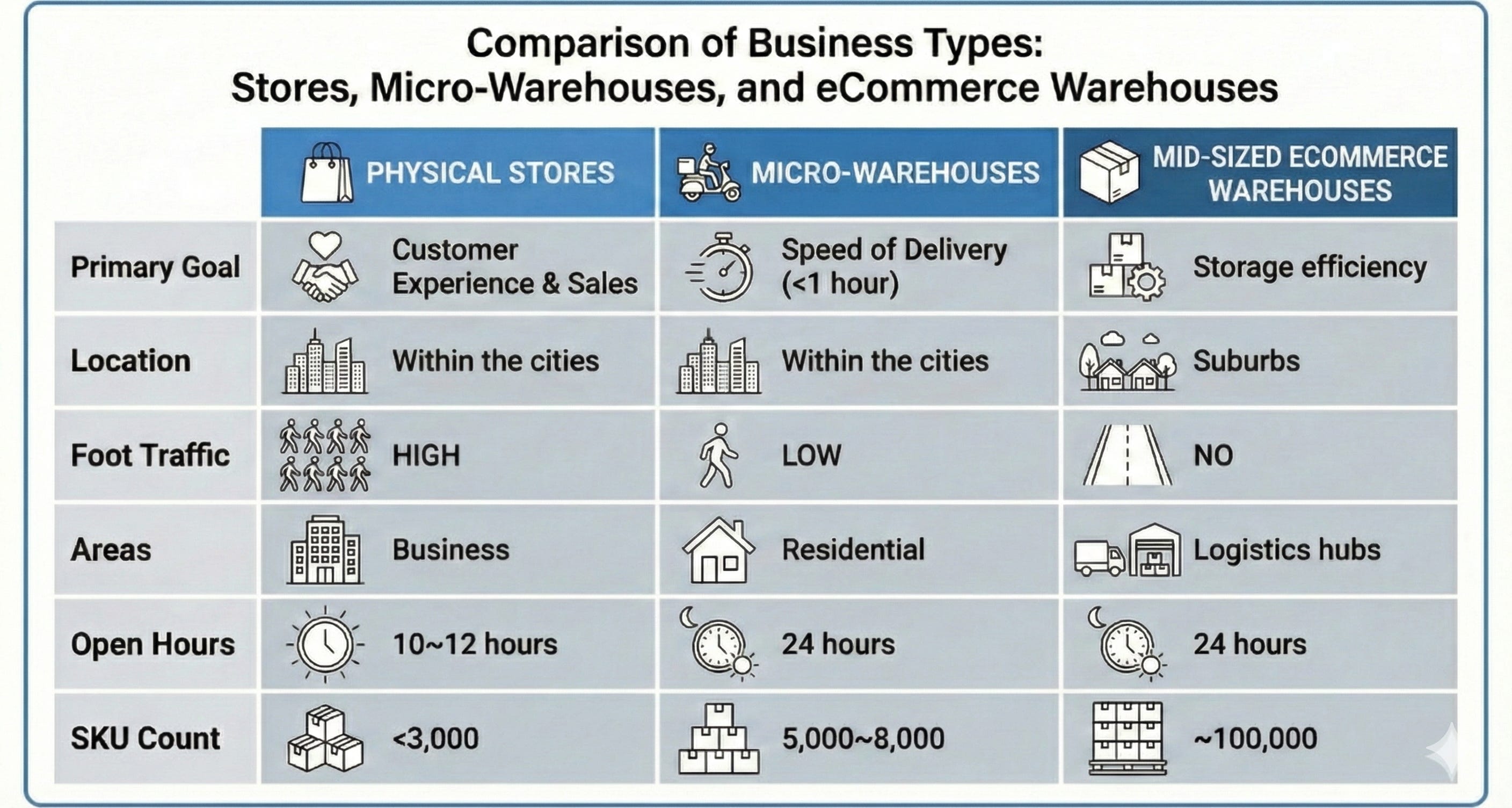

Micro-warehouses are the retail-goods equivalent of ghost kitchens. Just as ghost kitchens are built specifically for food delivery platforms, micro-warehouses are built specifically for quick commerce. They are typically cheaper to operate than physical retail stores, which allows platforms to offer more competitive pricing.

Like physical stores, micro-warehouses are usually located within cities. The difference is in their purpose. Physical stores are optimised for foot traffic and the in-store shopping experience. Micro-warehouses, by contrast, are essentially small warehouses embedded within urban areas, often located inside buildings or basements with near-zero foot traffic.

Another key difference is operating hours. Micro-warehouses are typically open 24 hours, whereas physical stores usually operate on limited schedules.

Here is a comparison of physical stores, micro-warehouses, and mid-sized e-commerce warehouses:

Micro-Warehouse Types

Micro-warehouses can be broadly divided into three categories:

General merchandise

Specialised warehouses

Brand warehouses

General Merchandise

General merchandise micro-warehouses are essentially the dark-store equivalent of convenience stores. They focus on high-frequency items and tend to have the highest location density.

Compared with convenience stores, the key difference is assortment. They typically do not carry fresh products, but they offer roughly 2-3x more SKUs.

Squirrel Convenience Store and Taobao Convenience Store are Meituan and Alibaba’s self-operated brand built around this model.

Specialised Warehouses

Specialised warehouses are dark-store formats built around specific retail verticals. Common examples include pet supplies, beauty and personal care, alcohol, and pharmacy.

Freshippo and Xiaoxiang Supermarket are fresh-focused formats backed by Alibaba and Meituan, respectively.

Brand Warehouses

Brand warehouses are facilities that hold inventory for well-known brands in order to enable faster, often same-day, delivery.

In most cases, brands do not operate these warehouses themselves. Instead, they partner with professional micro-warehouse operators that manage shared facilities and store products from multiple brands under one roof.

Meituan’s Advantages and Services

Meituan began building its micro-warehouse network in 2018 and accelerated these efforts in 2021. To support third-party merchants, it developed the “Meituan Morning Glory System,” a software suite that helps merchants manage warehouse operations, source products, and sell across multiple quick-commerce platforms.

Because this system is deeply integrated with Meituan’s ecosystem, warehouses that adopt it can receive more traffic and gain better visibility into local search demand.

Compared with Alibaba, Meituan currently offers a broader selection and lower pricing in general merchandise, and it has also built a solid base of specialised and brand warehouses.

Alibaba’s Advantages and Services

Taobao’s key advantages are its massive traffic and long-standing relationships with brands. Because of these relationships, many brands are willing to participate in Taobao’s brand-to-warehouse model, placing inventory closer to consumers. As a result, when users search on Taobao, they can already select branded products that are eligible for fast delivery.

This offering is still limited to a relatively small number of SKUs today, but it is expected to expand. In particular, products stocked within the same city should increasingly qualify for same-day delivery.

Compared with Taobao, Meituan lacks the same depth of brand relationships and the same breadth of traditional e-commerce SKUs, but it compensates with stronger control over on-demand fulfilment and local inventory density.

11. The Ecosystem Surrounding Quick Commerce Platforms

To understand the value chain of quick commerce, we can broadly break the ecosystem into three layers:

Traffic & demand generation

Merchants (restaurants, retailers, and other physical or online shops)

On-demand logistics platforms

In addition to these core layers, there is a crucial adjacent category: in-store services.

In-Store Services

In China, “in-store services” refer to physical retail or service consumption that is driven by online traffic. As the boundary between online and offline continues to blur, more and more physical businesses now rely on digital platforms to acquire customers.

Similar to ghost kitchens, China has seen the rise of barber shops, salons, clinics, and other service providers that operate in locations with almost zero foot traffic and rely almost entirely on online demand. In-store services in China have now grown into an industry worth roughly USD $280 billion.

To-Home Services

The counterpart to in-store services is to-home services, where goods or services are delivered directly to the consumer. Quick commerce is a classic example: products are delivered from physical locations to your home.

Historically, quick commerce platforms have relied primarily on to-home services to drive transactions. However, to capture more marketing spend and deepen merchant relationships, in-store services have become one of the most important complementary channels.

In-store services range from simple restaurant bookings and pickup orders, to group-buying meals, to a wide variety of coupons for offline activities and even OTA-style services. What makes in-store services especially attractive is their near-zero marginal cost. Before the quick commerce war began, Meituan’s in-store services were estimated to contribute around 40% of its overall operating profit.

Strategically, in-store services matter because restaurants, physical stores, and retailers all rely on the same traffic platforms to drive both in-store and to-home sales.

Traffic Platforms: Search and Discovery

Today, quick commerce platforms still rely heavily on search-driven intent to generate sales. However, with the rise of live commerce and short-form video, an increasing share of transactions is now driven by discovery-based content. Many merchants now maintain dedicated social media teams purely to generate discovery-driven demand on these platforms.

Traditionally, quick commerce platforms monetise through search traffic (ads and commissions) plus delivery fees. As discovery-driven traffic becomes a larger share of incremental growth, quick commerce platforms have increasingly begun competing directly with content-driven traffic platforms for user attention and advertising budgets.

Restaurants, Retailers, and Other Physical Shops

Restaurants, retailers, and other physical shops form the supply backbone of quick commerce platforms. Diversity of selection and price competitiveness are the main reasons users continue to transact on these platforms.

Non-food supply has now become the centre of the e-commerce battlefield, and this is the core reason why traditional e-commerce players like JD, Alibaba, and Shopee feel increasingly threatened by players like Meituan and Grab, and are now scrambling to build their own on-demand logistics networks.

To capture more value and improve price competitiveness, we should expect continued evolution at this layer. More and more sales are likely to shift from traditional brick-and-mortar stores to micro-warehouses. The trend of brands adopting micro-warehouse models is, in our view, inevitable.

On-Demand Logistics

The on-demand logistics layer is the keystone of the entire ecosystem. Its flexibility is what allows the same network to serve many different business types simultaneously.

On-demand logistics did not originate with food delivery. Long before mobile internet, businesses already used courier networks for urgent parcels and documents. The real transformation today is that platforms can now offer fast delivery at affordable prices to almost any business and any consumer. That is what makes this wave fundamentally different.

Looking ahead, we expect two main types of on-demand logistics platforms to coexist:

Vertically integrated platforms owned by traffic ecosystems (e.g. Meituan, Grab, Taobao)

Independent platforms (e.g. SF Intra-City, Lalamove), which are likely to focus more on the premium and specialised end of the market

12. Closing: What China Teaches Us

We believe China’s quick commerce war offers three lessons that matter far beyond China.

First, quick commerce is ultimately a density and platform strategy game. Food delivery is just the starting point of quick commerce, while the true long-term value lies in the non-food category. When rider utilisation is high enough, delivery becomes cheap enough to support a broader assortment and higher frequency. But China’s experience also shows that the outcome is not driven by density alone. What truly moves the needle is the platform’s willingness to actively shape the supply side, aggregating demand, shaping merchant behaviour, standardising operations, and iterating at breakneck speed towards pushing more categories and use cases onto the same delivery network. In other words, platforms do not merely “unlock” existing supply, they manufacture and discipline it to fit the network. This is how new categories and use cases get pushed onto the same delivery network, even before they are naturally profitable.

Second, order volume is the most important long-term indicator. More orders mean more density, better rider utilisation and lower cost per delivery. Without enough throughput, no delivery network can ever approach efficiency. But China has already shown that volume alone does not decide outcomes. Two platforms can run at similar delivery volumes and still end up with radically different losses per order. The reason is that order volumes alone are not sufficient. Unit economics is also key. The structure of the network and the mix of users and merchants ultimately determine whether growth compounds or simply burns cash.

Third, quick commerce expands not just through search-driven demand, but increasingly through discovery and in-app surfaces that manufacture incremental orders. Food is the entry point, but non-food is the real long-term prize. In China, platforms have increasingly used content, promotions, and in-store services to create incremental demand, further reinforcing frequency and utilisation across the network. As discovery becomes a larger share of orders, advertising also becomes a structurally more important monetisation lever, and one of the key competitive battlegrounds between platforms.

These lessons are directly relevant to Southeast Asia, but they will not play out in the same way. The region’s fragmentation, varying urban density, and higher delivery costs will shape both the pace of adoption and the ultimate profit pool. With that framing, we can now turn to Southeast Asia’s starting point.

13. The Current Players and Landscape in SEA Today

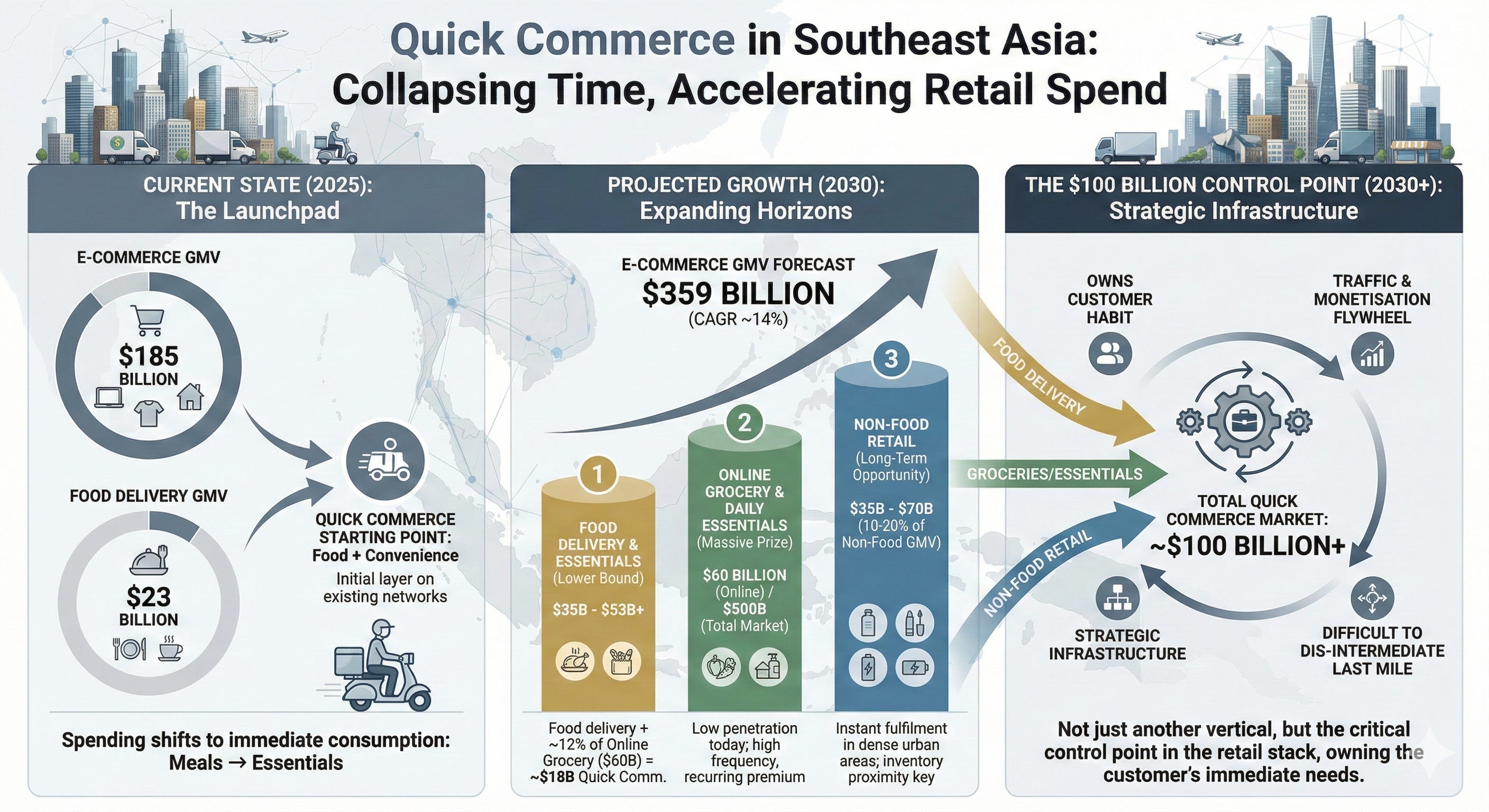

Southeast Asia’s e-commerce sector has expanded rapidly over the past decade, underpinned by rising internet penetration, affordable smartphones, and a young, mobile-first population. By 2025, total e-commerce Gross Merchandise Value (GMV) in the region reached approximately USD $185 billion, making it one of the fastest-growing digital commerce markets globally. While traditional marketplace e-commerce still accounts for the majority of this volume, a structurally important shift is underway within the ecosystem.

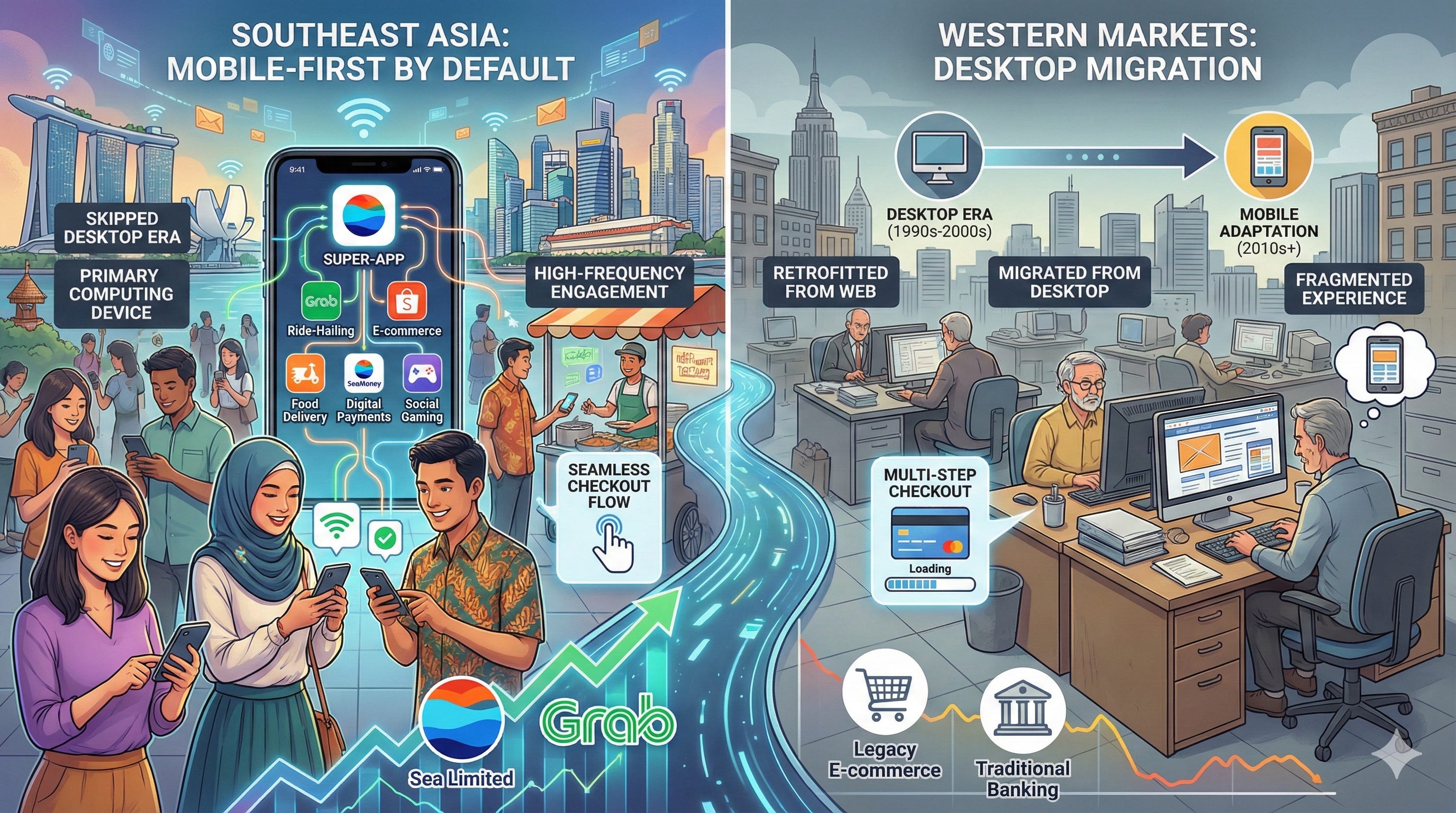

A defining characteristic of Southeast Asia’s digital economy is that it is mobile-first by default. Unlike Western markets that migrated from desktop to mobile, Southeast Asia largely skipped the desktop era altogether. For hundreds of millions of consumers, the smartphone is their primary and often only computing device.

This has profoundly shaped how commerce platforms are built and used: verticalised apps, super-app behaviours, deep integration with payments, and high-frequency engagement loops are the norm. This environment has disproportionately benefited the likes of Sea Limited and Grab, whose entire product experience was designed from day one around mobile discovery, in-app engagement, and seamless checkout flows, rather than being retrofitted from a web-based desktop-first paradigm.

Quick commerce is emerging as one of the most promising growth vectors within Southeast Asian e-commerce. Although it remains a smaller portion of total GMV today, its strategic importance far outweighs its current scale. This is particularly true in online groceries, where penetration remains in the low single digits across most markets. As urban density increases and consumers grow accustomed to on-demand services, the ability to deliver essential goods within minutes rather than days is becoming a defining differentiator rather than a niche offering.

Food delivery represents another adjacent vertical that we believe will increasingly converge with quick commerce. In 2025, food delivery GMV in Southeast Asia is estimated at roughly USD $23 billion. Importantly, food delivery has already solved many of the hardest problems in last-mile logistics: dense rider networks, demand forecasting by location and time of day, and consumer willingness to pay for speed and convenience.

When combined with e-commerce and grocery delivery, these segments together represent a total addressable opportunity of more than USD $200 billion, growing at a mid-teens pace despite macroeconomic headwinds.

Unlike China, where quick commerce has entered a phase of intense competition focused on market dominance, subsidies, and monetisation, Southeast Asia remains firmly in the earlier stage of ecosystem formation. The current battle is not about extracting maximum profit per order, but about positioning, habit formation, and defining default consumer behaviour. Platforms are competing to become the first app consumers open when they need something immediately, whether that is a meal, groceries, or household essentials.

Growth in the sector continues to be driven by urbanisation and deeply entrenched on-demand consumption habits, but it is becoming more measured. Inflation and economic uncertainty have made consumers more value-conscious, forcing platforms to balance speed and convenience against pricing discipline and operational efficiency. This environment increasingly favours players with existing scale, strong logistics infrastructure, and the ability to cross-subsidise across multiple services.

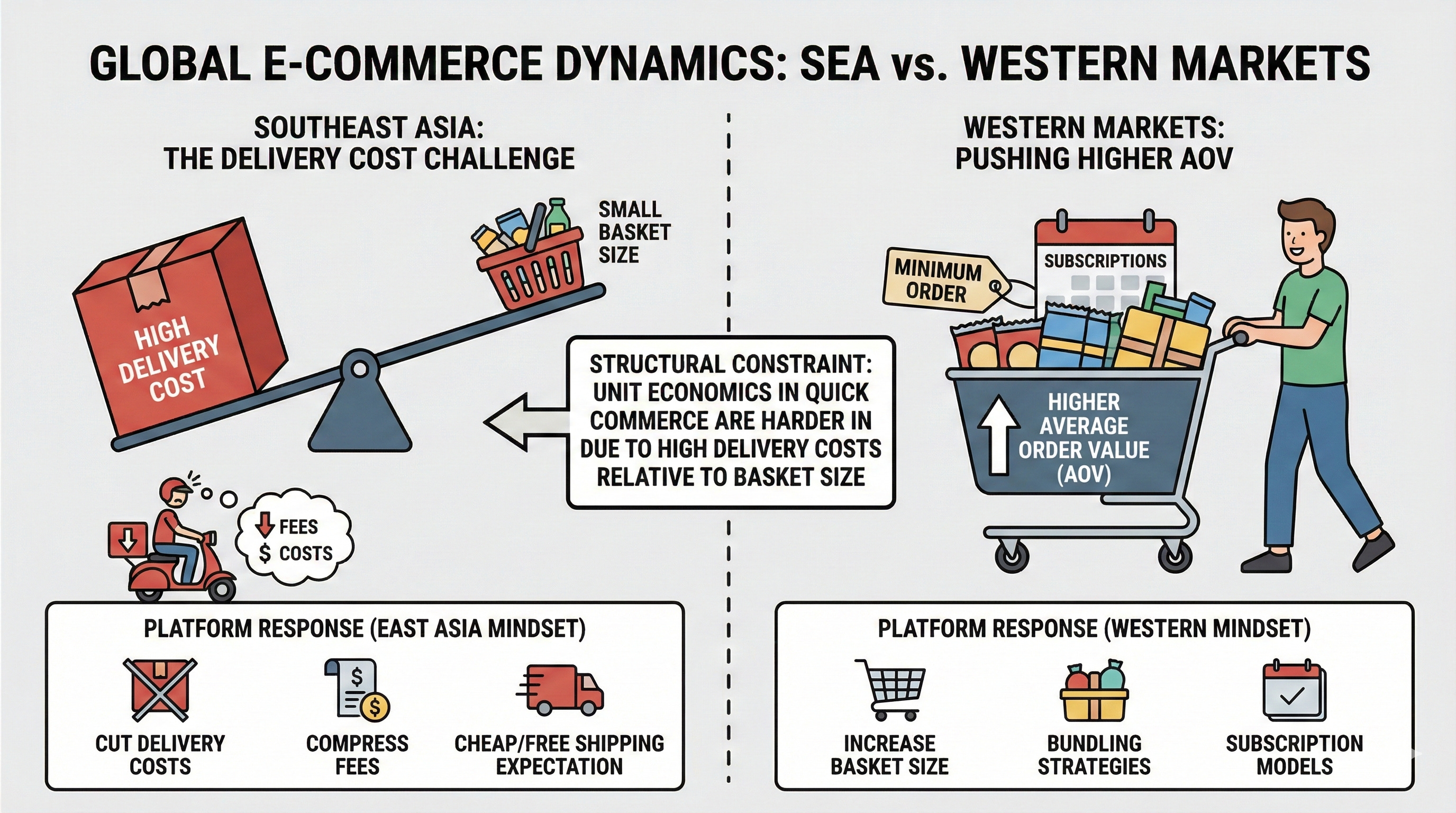

A key structural constraint in Southeast Asia is that delivery costs remain high relative to basket size. This creates a fundamental tension. In Western markets, the typical response has been to push average order values (AOV) higher through bundling, subscriptions, and minimum order thresholds. In much of East Asia, however, the platform mindset is different. Rather than increasing basket sizes, platforms are under constant pressure to cut delivery costs and compress fees, because consumers are highly price-sensitive and used to cheap or free shipping. This makes unit economics in quick commerce structurally harder and raises the bar for operational excellence.

In our view, only three players meaningfully matter in Southeast Asia’s quick-commerce landscape today: Grab, Sea Limited, and TikTok Shop. Each is approaching the opportunity from a fundamentally different angle, shaped by their core competencies, existing user relationships, and long-term strategic objectives. We believe understanding these differences is key to understanding how Southeast Asia’s quick-commerce market is likely to evolve over the next decade.

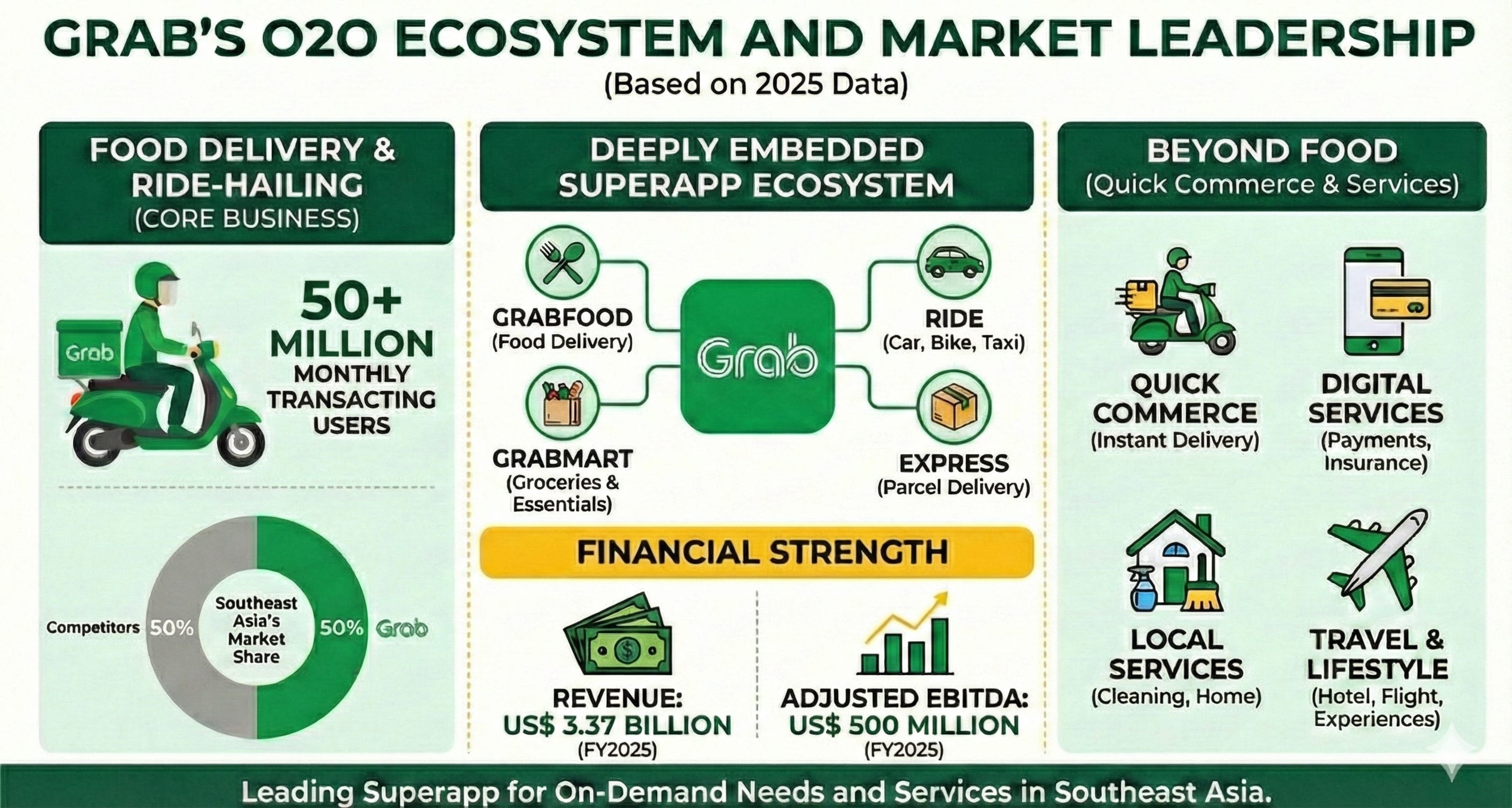

Grab Holdings

Grab is the clear leader in ride-hailing and food delivery across Southeast Asia, with roughly 55% market share in the latter. In major urban centres such as Singapore, Jakarta, Bangkok, Ho Chi Minh City, and Manila, Grab benefits from the deepest rider density, the highest order frequency, and the strongest restaurant relationships.

In terms of Grab’s push towards quick commerce, their strategy has been to leverage its ride-hailing user base and infrastructure to cross-sell food (GrabFood) and grocery services (GrabMart), positioning itself as the go-to app for on-demand needs. It has also adopted the Meituan strategy of expanding beyond food into local retail, errands, ticketing, and services.

Grab’s core strength is its delivery network and marketplace efficiency. The company operates in over 500 cities and has over 45 million monthly transacting users. More importantly, Grab already owns the hardest asset to replicate. It has a liquid, city-level logistics network that is profitable in food delivery and extensible into adjacent categories. In other words, food delivery is what has kick-started Grab’s journey but is not the end-game. It is instead the engine that keeps riders active, demand predictable, and unit economics stable.

Grab is the closest equivalent to Meituan in Southeast Asia due to its deep focus on logistics-led services, food delivery, and local commerce. Like Meituan, Grab's core strength lies in owning the "I-need-it-now" consumer moment across major urban centers, leveraging a dense and operationally mature rider network that has already achieved profitability in food delivery.

To truly win in quick commerce, Grab’s next phase is not just about adding more categories, but about professionalising its fulfilment stack. That means better handling of fragile items, higher-value goods, temperature-sensitive products, and more standardised service levels. Today’s rider-based pickup model works extremely well for meals and convenience goods, but scaling into broader retail will require tighter packaging standards and more predictable service quality.

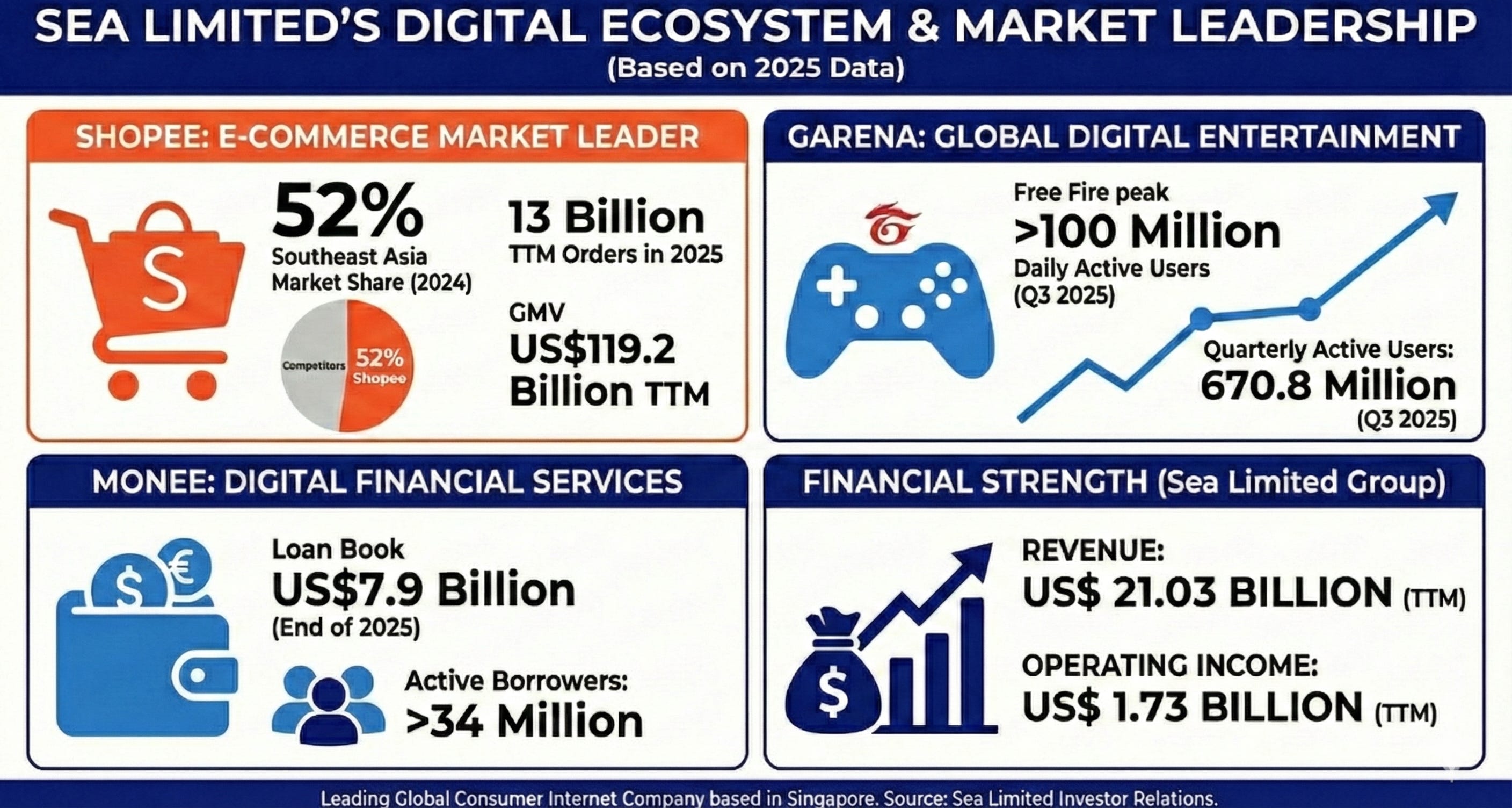

Sea Limited

Sea Limited is the largest digital player in the space and through Shopee, owns Southeast Asia’s largest demand surface in e-commerce. Its logistics arm (SPX Express) has scaled rapidly into next-day and same-day delivery, but it remains structurally different from food delivery networks.

That said, Sea Limited has made an entry into food delivery through ShopeeFood. Today, it has a presence in Vietnam, Thailand, Malaysia and Indonesia, with plans to launch in Philippines in the immediate future. It is not clear if Shopee has plans to aggressively enter the quick commerce landscape, but it appears to be an inevitable future, as we will discuss later.

In dense cities like Jakarta, Shopee has introduced same-day and instant delivery options (under 2 hours) for select purchases. When a user orders from a nearby seller, Shopee may dispatch a ShopeeFood rider (motorbike courier) to pick up the item immediately, rather than routing through postal delivery. This effectively turns the vast network of marketplace sellers into nodes for quick fulfillment, using the already scaled logistics asset of ShopeeFood.

As Forrest Li, Sea’s CEO, noted, demand for very fast delivery is rising among urban buyers who even show willingness to pay a premium for under-2-hour service, and Shopee saw a 35% YoY increase (Q3 year-on-year) in orders using these faster options in Greater Jakarta.

A critical asset is ShopeeFood. Despite entering the market late, it has scaled rapidly. In 2025, ShopeeFood’s GMV is estimated at USD $3.3 billion, surpassing Foodpanda’s USD $2.5 billion and Gojek’s USD $1.9 billion in food delivery. This makes ShopeeFood the second-largest food delivery platform in Southeast Asia by GMV, with roughly 14% market share, up from about 5% just three years ago.

The picture is even more striking in the four markets where ShopeeFood actually operates. There it holds close to 20% market share. The competitive impact shows up clearly in Grab’s numbers. In ShopeeFood markets, Grab’s share is about 50.5%, versus 67% in markets where ShopeeFood is not present, highlighting ShopeeFood’s role as meaningful competitor.

The strategic logic is that ShopeeFood can serve as a “foot in the door” for quick commerce beyond food. Once a driver network is in place and consumers get used to ordering on Shopee frequently, not just for occasional shopping but daily needs, Shopee can integrate other on-demand offerings. Interestingly, Shopee has taken a different approach to players in China and India. Instead of building a separate quick commerce business, it is compressing delivery time by using assets that are already scaled, such as utilising ShopeeFood riders to fetch and deliver parcels for Shopee orders.

Shopee appears to be closest to Alibaba in terms of its roots and strategy. Like Alibaba, Shopee began as a traditional e-commerce marketplace with a strong focus on third-party sellers, and control over the customer experience. Both have since expanded into adjacent services, including food delivery, while continuing to rely on batch-based fulfilment experience.

Shopee reflects Alibaba’s model in terms of its platform ecosystem, monetisation strategy, and traffic power. Like Alibaba’s Taobao, Shopee generates massive consumer demand through search-driven shopping, price promotions, and in-app engagement. It increasingly monetises this traffic through advertising, seller services, and payments, much like Alibaba does via Taobao/Tmall.

Alongside this, Shopee has been steadily layering in discovery-driven commerce through features such as Shopee Live, short-form video feeds, and algorithmic product recommendations. This shifts part of the shopping journey from pure intent-based search toward browsing and impulse discovery, allowing Shopee to stimulate demand rather than merely capture it. In this sense, Shopee is gradually blending Alibaba’s search-driven marketplace model with elements of TikTok-style content commerce, broadening both user engagement and monetisation opportunities.

Importantly, Shopee is also gradually shifting towards a more B2C and consignment-driven model in selected categories. Through ShopeeMall, brand stores, and more centralised fulfilment arrangements, Shopee is taking greater control over inventory quality, delivery standards, and customer experience. This mirrors the path taken by JD and parts of Alibaba’s ecosystem, where platforms move from being pure marketplaces towards hybrid models that blend third-party sellers with platform-managed inventory to support faster, more reliable fulfilment.

To win in quick commerce, Shopee’s key challenge will be operational standardisation. Its marketplace DNA gives it enormous breadth, but also introduces variability in packaging, fulfilment readiness, and service quality. Moving into instant delivery for higher-value or more fragile goods will require tighter control, clearer merchant standards, and deeper integration between its warehousing, riders, and seller network.

TikTok Shop

TikTok Shop is the newest entrant reshaping Southeast Asia’s e-commerce, taking an attention-first approach by integrating shopping into the wildly popular TikTok short-video social media app. It is the fastest growing e-commerce player, with estimates of about mid double-digit growth in 2025, which is incredible considering the scale it now operates at.

Owned by ByteDance, TikTok brings a fundamentally different DNA. Rather than starting from delivery or marketplace infrastructure, it started from an algorithmic content platform with hundreds of millions of engaged users and added e-commerce functionality on top. Interestingly, it is the only major player in both China and Southeast Asia.

In Southeast Asia, TikTok Shop launched around 2021 and quickly gained traction by leveraging TikTok’s massive user base in countries like Indonesia, Thailand, and Vietnam. Its model is inspired by Douyin (TikTok’s Chinese sister app), where in-app shopping has become hugely successful. In SEA, TikTok Shop has seen explosive growth, although not without regulatory hurdles.

TikTok Shop’s strategy is a unique one. It has positioned itself as a social commerce platform where users discover products through videos and live streams in their feed, rather than through search queries. The idea is that every scroll can become a shopping opportunity. For instance, a makeup tutorial links to the cosmetics being used, a fashion livestream has “buy now” pop-ups for the clothes, etc. However, it is also incentivising users to create content specific for shopping conversion. (This is something Amazon has tried in the past to no avail)

TikTok’s rise is fueled by its hundreds of millions of users in the region and its highly engaging content algorithm. Southeast Asia has a huge TikTok user base. For context, TikTok has over 150 million users in Indonesia alone. This gives TikTok Shop a built-in audience that it can convert into shoppers without them ever leaving the app. TikTok’s algorithm excels at showing users content they didn’t know they wanted, also known as impulse buying.

TikTok Shop is still early in instant commerce, but it is perhaps the most dangerous long-term variable for its competitors. It has unmatched attention density and live-commerce conversion, giving it a unique position to influence where demand flows, even if it does not own delivery (yet). Being the subsidiary of ByteDance in China, its strategy mirrors that of Douyin, dominating user attention and demand creation, despite lacking the same depth of proprietary logistics infrastructure.

TikTok is also beginning to experiment with faster fulfilment, including 1-hour delivery in selected markets and categories, signalling that it understands attention alone is not enough. However, unlike Grab and Shopee, TikTok remains logistics-light and heavily dependent on partners. Its long-term challenge will be building a fulfilment experience that matches the immediacy of its content consumption.

To win in quick commerce, TikTok must evolve from being a demand-generation machine into a reliable commerce platform. That means investing in fulfilment standards, returns handling, customer service, and merchant discipline, especially as it moves into higher-value and more complex product categories.

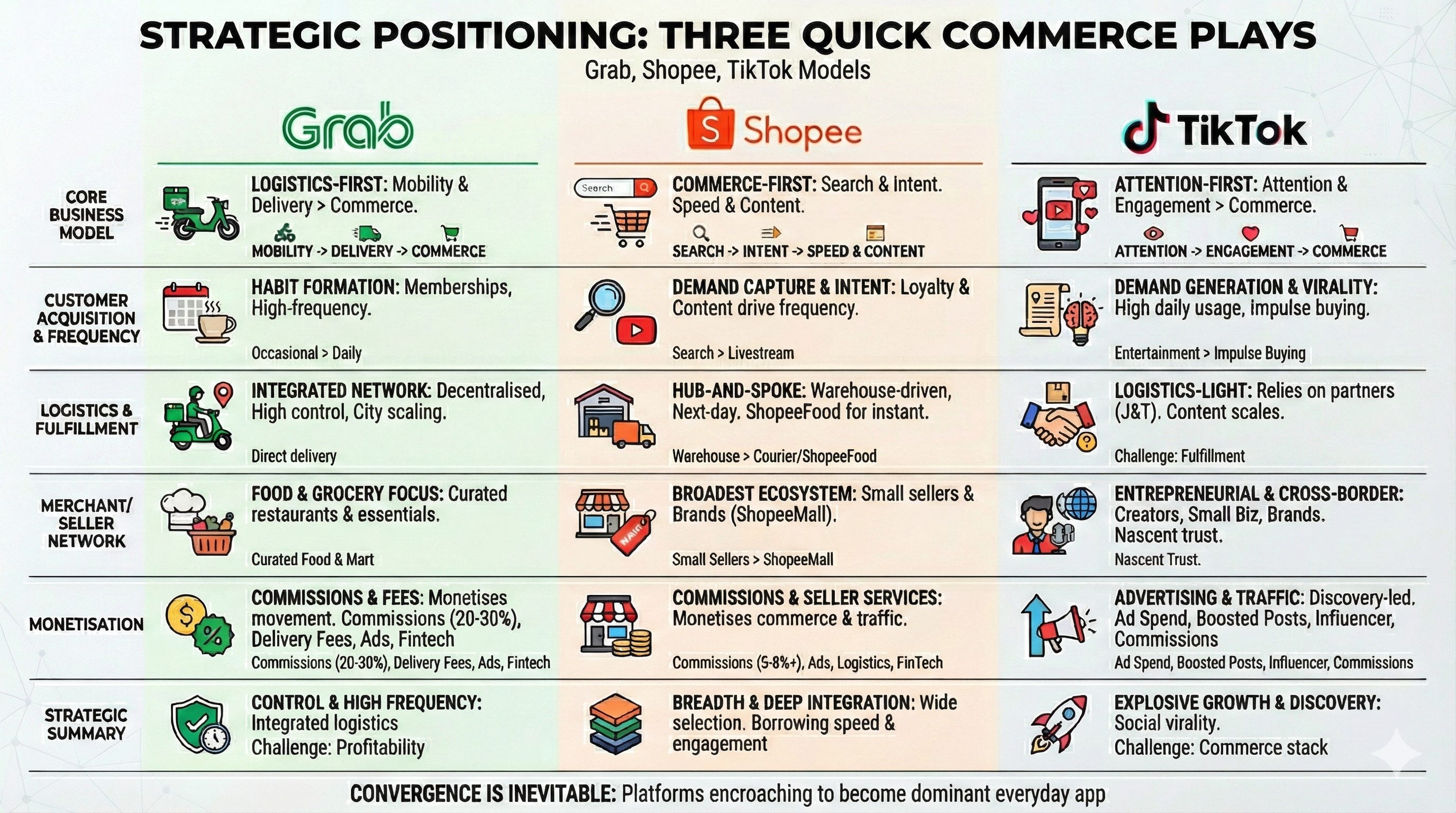

14. Strategic Positioning: Three Different Plays

The quick commerce strategies of Grab, Shopee, and TikTok reflect their different origins and core competencies. Let’s compare and contrast their models along key dimensions:

(For more context on these 3 competitors, check out this article)

Core Business Model

Grab exemplifies a “logistics-first” model, building from mobility and delivery services. It focuses on solving the real-world problem of moving people and goods efficiently, then layering commerce on top of that network.

TikTok Shop represents an “attention-first” model, where the primary asset is consumer attention and engagement; commerce is a way to monetise that attention.

Shopee represents a “commerce-first” model rooted in search and intent-driven purchasing. Its core asset is not attention or logistics, but demand with clear buying intent. It is monetising that purchasing intent and now progressively layering in speed and content to broaden when and how often that intent is expressed.

Customer Acquisition & Frequency

Grab and Shopee initially relied on incentives and breadth of selection to seed adoption (e.g., cheap rides, free delivery, massive catalogues). Over time, they deliberately engineered habit formation by expanding everyday use cases and then layering in memberships and loyalty programmes (GrabUnlimited, Shopee’s VIP tiers).

For instance, Grab moving from occasional rides and weekly grocery shops to daily food orders and even multiple touch-points per day. The result is a shift from promotion-driven usage to embedded, repeat behaviour across verticals.

At the same time, both platforms have been deliberately increasing their level of control and monetisation intensity. What began as physical advantages (rider fleets, merchant density and local coverage) has progressively turned into a digital edge driven by data, algorithms and product design.

Platforms are also moving up the stack through greater vertical integration, from handling parts of sourcing and private labels (e.g., GrabMart) to expanding into adjacent verticals such as bookings, reviews, and FinTech. As more activity flows through their ecosystems, software increasingly determines demand allocation and monetisation, compounding their competitive advantages over time.

TikTok entered, probably somewhat fortuitously through a different strategy, already commanding high daily usage because of its entertainment value. The challenge for them is in converting that usage into purchases.

Another way we can look at the dichotomy between these players is the “demand-generation vs demand-capture” piece. Grab generates demand by convenience, which is more akin to fulfilling latent needs. Shopee was traditionally more demand-capture (people going onto Shopee when they needed something), however livestreams and tie-ups with YouTube and Meta may change that into a demand-generation machine. TikTok’s commerce strategy revolves around turning passive scrolling into impulse buying, generating demand that might not have existed otherwise.

Logistics Network & Fulfilment

Grab has the most integrated logistics network suited for quick commerce. Its army of riders is a core asset, giving it control over the customer experience. It operates a decentralised model (drivers pick up from merchants).

Shopee’s logistics is more hub-and-spoke and warehouse-driven for now, optimised for next-day delivery, though it’s leveraging ShopeeFood riders for instant delivery in some cases.

TikTok is logistics-light, relying on partners (primarily J&T Express).

This affects scalability. For instance, Grab can scale quick deliveries city-by-city, but might find it harder to handle large-items or cross-country deliveries. Shopee can handle nationwide distribution through its warehouses and courier partners, but is now tweaking to handle intra-city express. TikTok can scale content virally across countries easily, but fulfilling orders physically is likely to be a challenge and require time.

Merchant/Seller Network

Shopee has the broadest merchant ecosystem, millions of small sellers plus brands. Through ShopeeMall, it is now the leading platform for brands in Southeast Asia. It is essentially infrastructure for others to sell.

Grab’s merchant network in quick commerce is currently focused on food & grocery outlets. It curates this network to ensure coverage of popular cuisines and essential goods. Crucially, this is not a generic marketplace that can be copied and pasted across markets, but instead, is a fragmented and localised network that is structurally difficult and time-consuming for competitors to replicate at scale.

TikTok’s merchant base started with a lot of entrepreneurial individuals and small businesses, some of whom are new to e-commerce but savvy in social media, as well as cross-border sellers from China providing ultra-cheap goods. Over time TikTok is attracting more established brands and retailers to set up official TikTok stores given the platform’s reach.

Each platform’s seller mix influences customer perception. For instance, Shopee and Grab, having been around for longer, are perceived as more “trusted” for transactions while TikTok is still in a nascent stage and has to prove its reliability.

Monetisation and Revenue Streams

All three ultimately monetise via transaction commissions and fees, albeit with nuances.