Food Delivery in Southeast Asia (2026)

The Two-Horse Race (Grab vs Sea)

Food Delivery is one of the most lucrative sectors for platforms to operate in. From a convenience add-on prior to COVID, food delivery is now a weekly, sometimes daily, digital habit for tens of millions of households.

Once that habit has formed, it has become increasingly difficult for consumers to go back to their old ways.

In the US, food delivery has scaled into a US$100B+ annual GMV market. DoorDash alone is at a $100B annualised GMV run-rate as of Q3 2025. (Key to note that this includes grocery and convenience delivery at ~25-30%)

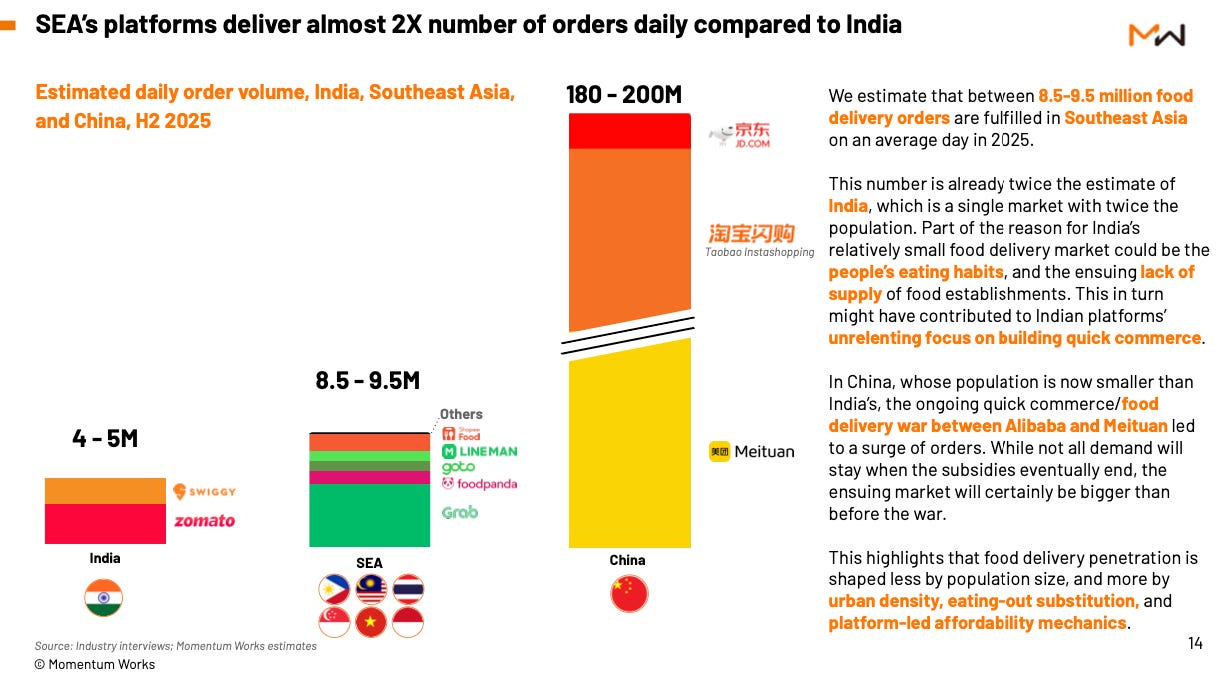

China is a whole level above. It processes between 180-200 million orders per day, translating to 70+ billion orders per year, across food, groceries and local retail. This adds up to ~$300B in annual GMV. Meituan, the leading food delivery business in China, processes over $150B in food delivery GMV annually. Food delivery in China is no longer a vertical, but a demand engine for the entire local services economy.

Southeast Asia today sits at a much earlier point on the same curve, but the numbers are already meaningful. Regional food delivery GMV is estimated at $22.7B as of end-2025 with roughly 8.5-9.5 million daily orders. This is still only a fraction of China and the US on an absolute basis, but it is inevitable that penetration rates, order frequency and unit economics improve over time.

In this piece, we run through the key takeaways from food delivery in Southeast Asia in 2025, what to expect in 2026, the key players moving forward and my personal perspective of the space.