Grab Q1 2026 Earnings Review

Surprisingly Strong Results Amidst a Challenging Climate

Grab reported Q1 2026 Earnings after the market close on 4th May 2026.

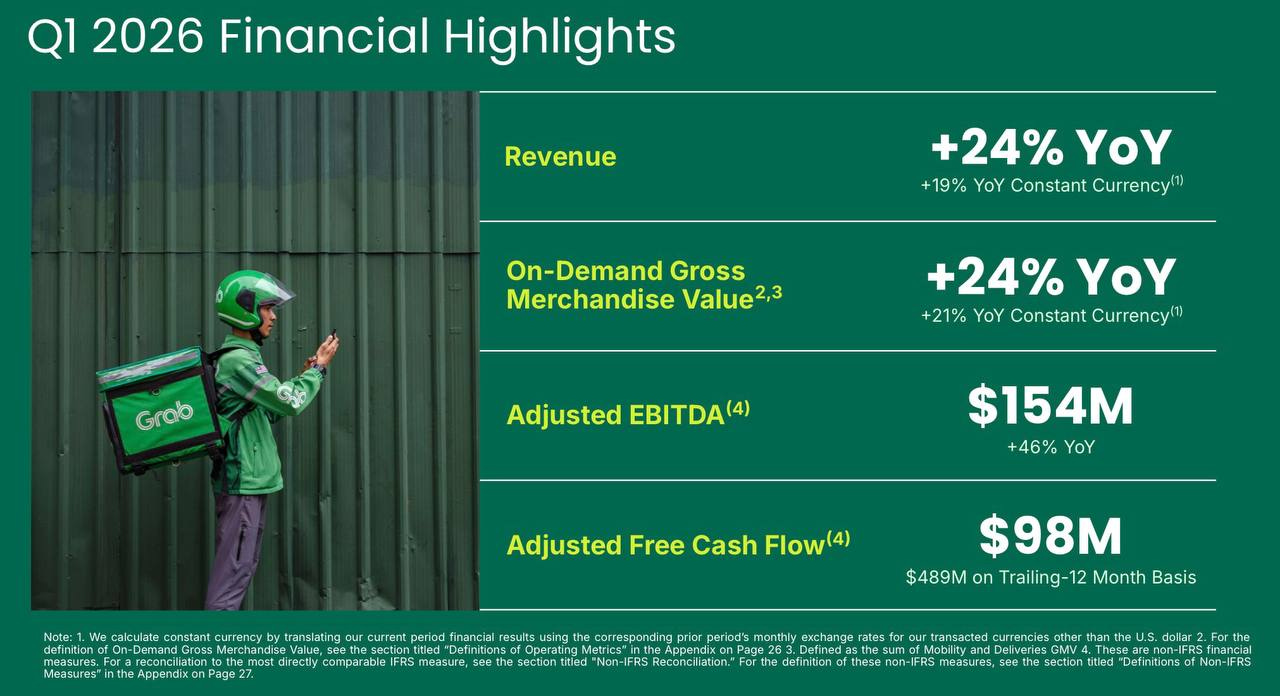

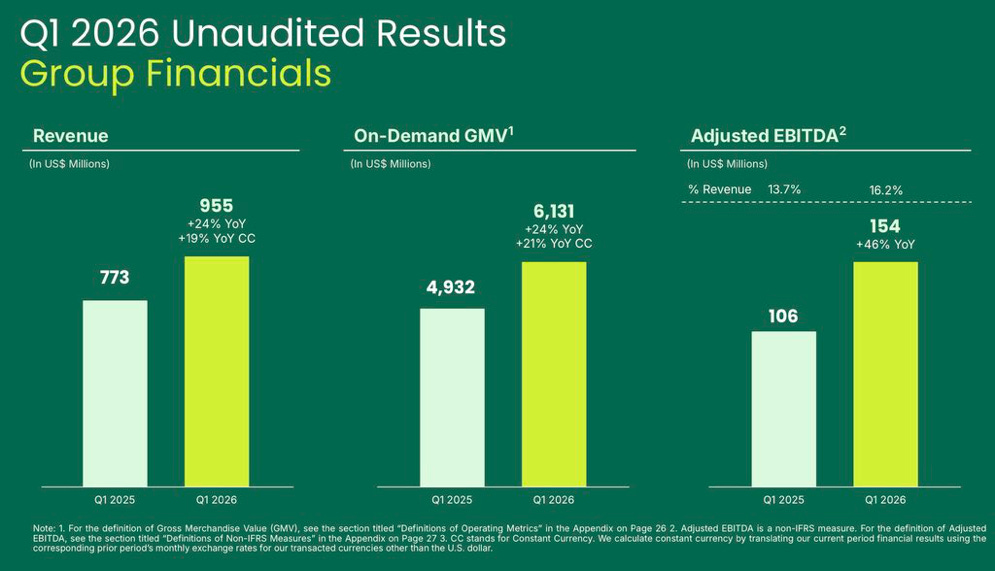

Revenue: $955M v $921M est. (+24% YoY, 19% Constant Currency)

EBITDA: $154M v $142M est. (+46% YoY)

EPS: $0.04 v $0.02 est.

Selected Key Metrics

On-Demand GMV: $6,131M (+24% YoY)

On-Demand GMV per MTU: $130 (+4% YoY)

Group MTUs: 51.6M (+16% YoY)

Loan Portfolio: $1,438M (+130% YoY)

Adjusted EBITDA: $154M (+46% YoY)

Adjusted Free Cash Flow: $76M (+10% YoY)

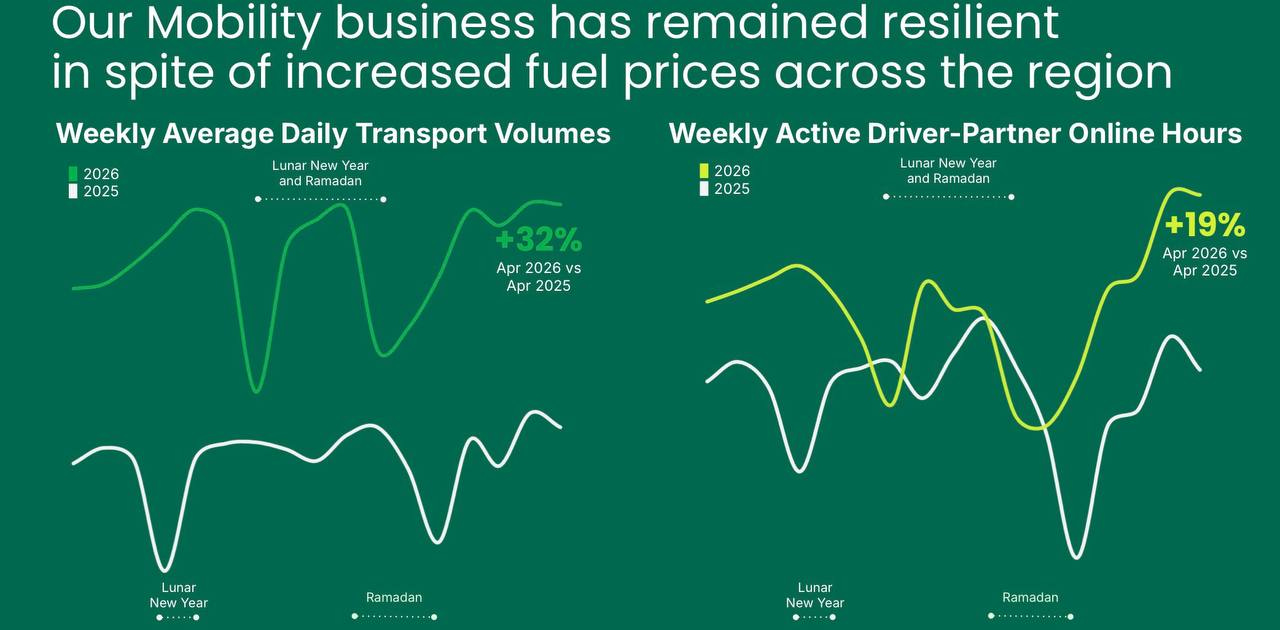

Grab’s earnings for the quarter beat expectations on both top and bottom-line. This was quite surprising considering Q1 was expected to be a weak quarter due to fuel price spikes related to the Strait of Hormuz crisis.

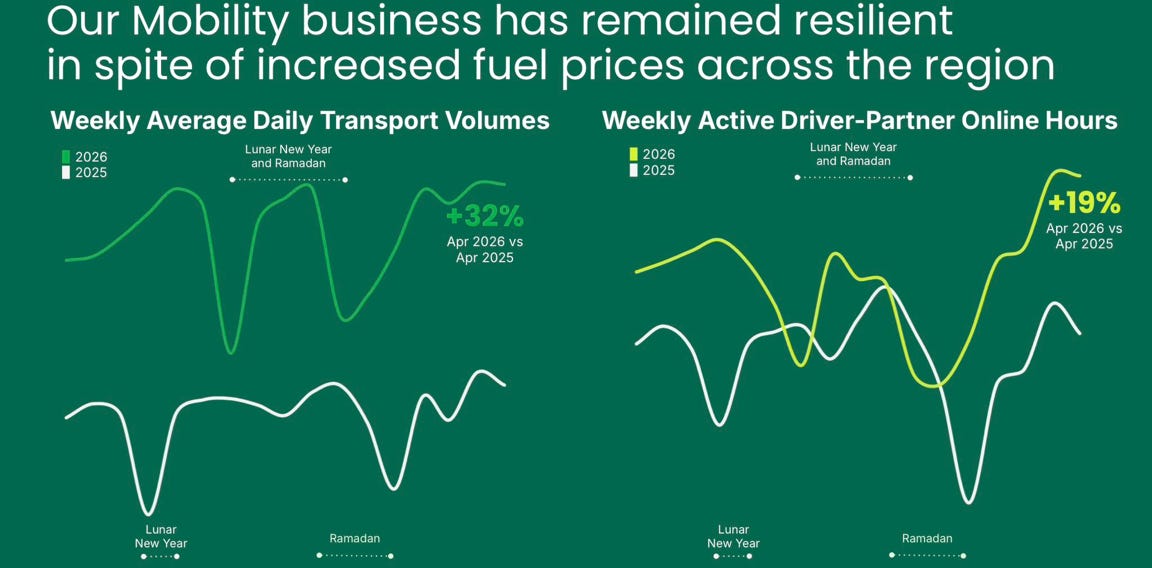

Interestingly, it was not a case of deliveries/financial services cushioning the fall in mobility. The mobility business remained extremely strong, with volumes in April up 32% YoY despite the increased fuel prices.

In this piece, I will break down the earnings in full, highlight key points on management commentary during the call and discuss my personal thoughts in the last section.

Table of Contents

Deliveries & Mobility

GFin, Financial Services

Key Call Commentary

Positives & Negatives

Conclusion

1. Deliveries & Mobility

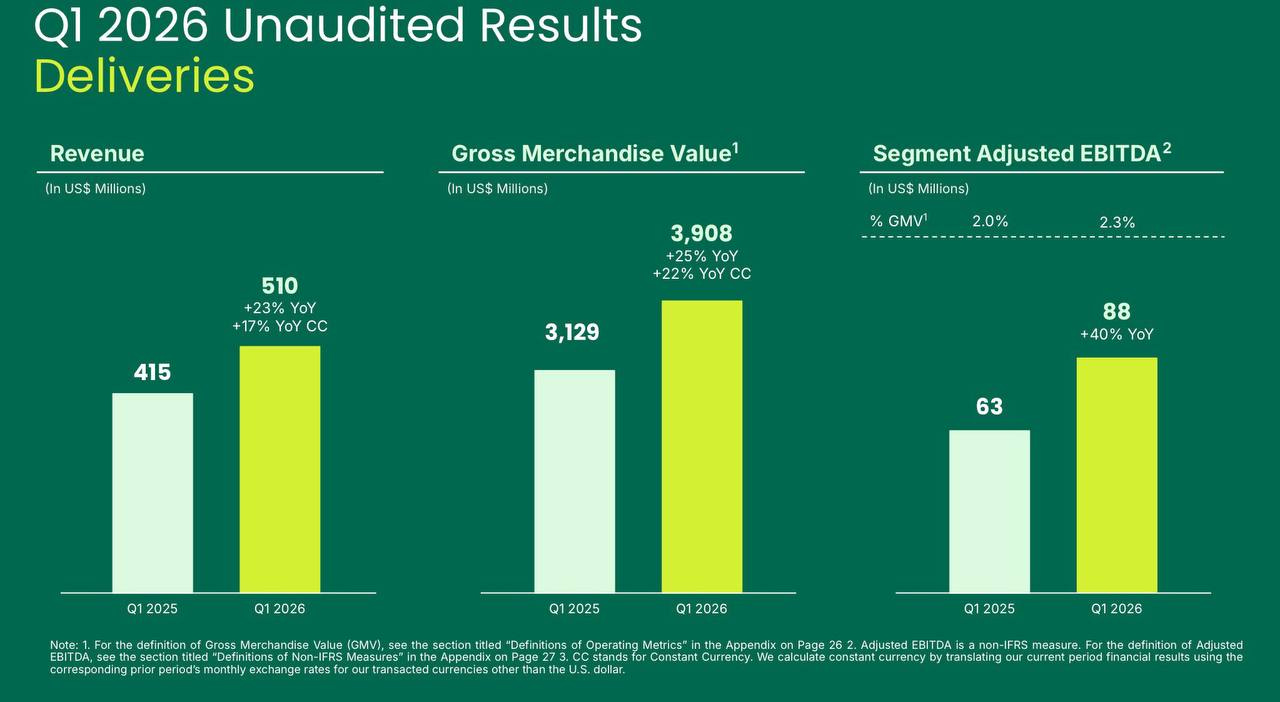

Deliveries is Grab’s largest segment by GMV and Revenue.

GMV grew 24% YoY (or 22% on a constant currency basis). Adj. EBITDA margin also grew from 2.0% to 2.3%, tracking closer towards management’s long-term target of 4+% margins.

This growth has been attributed to higher contributions from advertising and gains in operating leverage. Segment Adjusted EBITDA was up 40% YoY as a result.

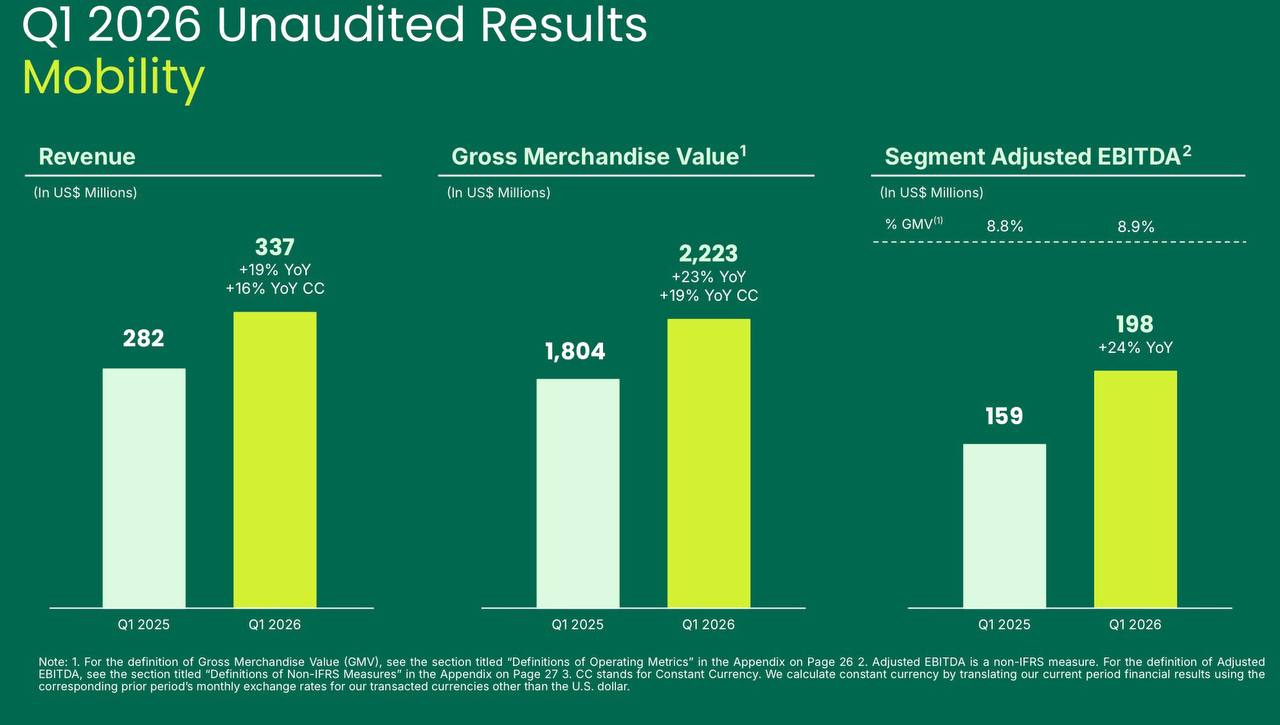

Mobility GMV grew 23% YoY (or 19% YoY on a constant currency basis). Revenue growth was slower at 19% YoY (or 15% YoY on a CC basis) due to the continued focus on affordability.

Segment Adj. EBITDA continued expanding from 8.8% to 8.9%. This is more or less the steady state margin target that management has issued for mobility (9+%).

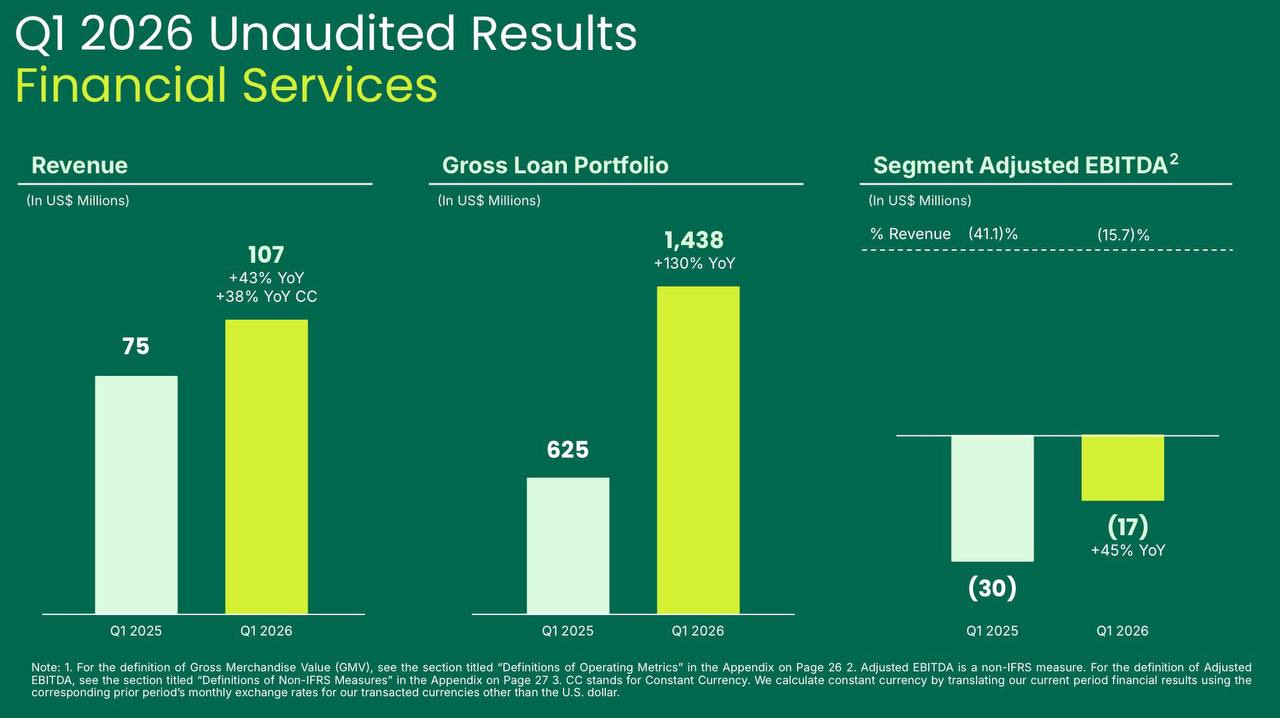

2. GFin, Financial Services

This quarter was yet again very strong for GFin, following on from last quarter. The net loan portfolio reached $1.44B, up from $1.18B just last quarter. That represents 22% QOQ growth and 130% YoY growth.

Management has set a FY2026 target of $2B, that appears to be a rather low bar considering the current numbers. Segment Adj. EBITDA margin improved from -41.1% to -15.71%. Grab tracks closer towards profitability, which it expects in the 2nd half of this year.

Customer deposits across GXS Singapore and GXBank Malaysia remained relatively stable at $1.63B.

As I’ve discussed in the past, I believe Grab has the potential to grow much faster than ~40%. For instance, Sea has 10x the loan book but is growing faster. Grab’s recent launch of cash loans for consumer could help spur this.

3. Key Call Commentary

Again, Grab hosted a live video earnings call with an IR head taking charge of questions.

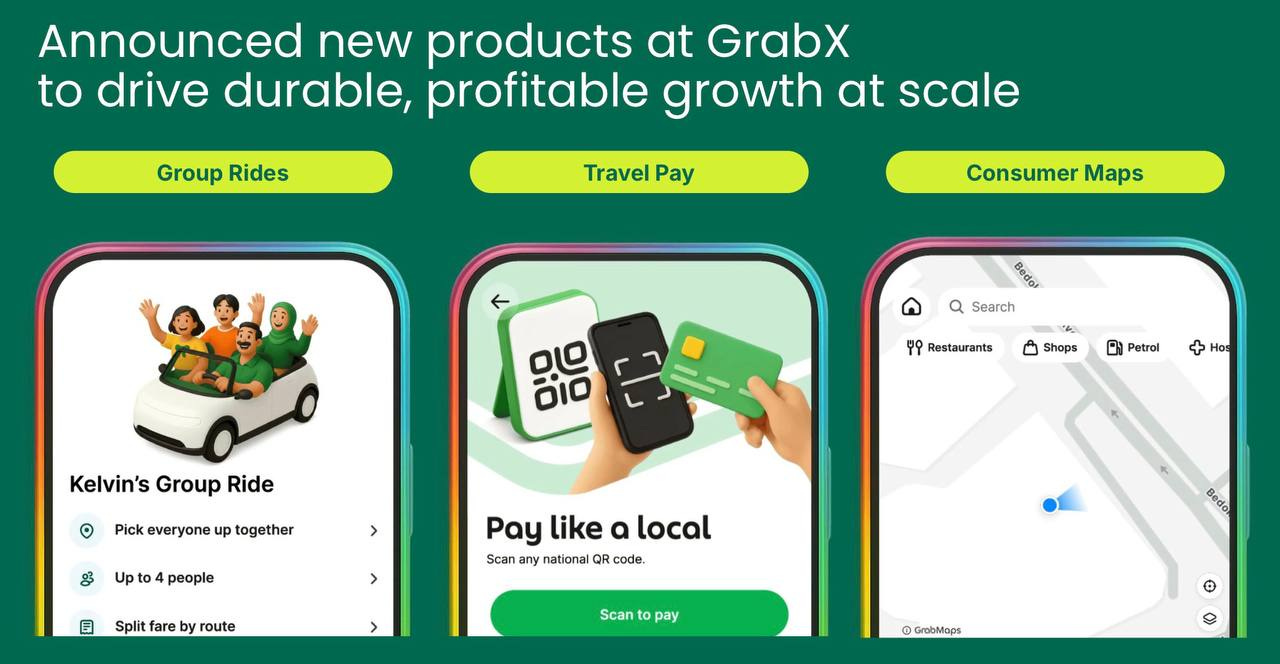

On New Product Innovations

“Product innovations we have made have really targeted affordability and reliability. Group orders, for example, has GMV up 74% year-on-year, and we launched group rides at GrabX last month, which is a similar concept for sharing rides to reduce pricing for individual consumers. And that’s now available across all 6 of our core markets. GrabUnlimited, of course, is very good value for high-frequency customers, and it continues to account for 1/3 of our deliveries GMV. So all of these are highly affordable products, which keep the demand strong even when consumers are stretched.”

On Fuel Crisis

“We’re monitoring the fuel situation extremely closely. And of course, we will not hesitate to act further if needed. In the medium term, we are committed to accelerate the EV transition to reduce our driver partners exposure to fuel price volatility.

So for example, in Thailand and Philippines, we have a drive-to-own program that connects our drivers with OEMs like BYD and GAC, where we have deals of up to 70,000 vehicles available across 6 markets with accessing to financing so they can own those more easily. In Vietnam, we have secured preferential charging rates also through our charging network partners, EBOOST and Charge+, which helps our drivers in the transition also. And finally, in Thailand, I am pleased to say that our total fleet supply has crossed 30,000 EVs on the platform and demand for those from consumers is also strong, where they can select that EV option, and that demand has grown by over 35% year-on-year.

So this fuel crisis has become an opportunity in the sense that it helps us to accelerate that EV transition.”

On Indonesia’s 8% Commission Cap

“The recent announcements are explicitly focused on Ojek drivers, who are our 2-wheel ride hailing partners. The 4-wheel drivers earn well above the minimum wage, so we believe they're less of a concern for regulators in Indonesia.

That said, of course, we're engaging very proactively with the relevant ministries to try to seek absolutely clarity and the technical aspects of how the decree will be implemented.

It's worth noting that 2-wheel mobility, that the decree referred to in Indonesia, is less than 6% of our total mobility GMV. So we are, therefore, reiterating our expectations for mobility margins to stabilise within that historical range and not to go outside of that range."

On GrabMart

“GrabMart is an exciting segment. The TAM is very large, arguably larger than food delivery altogether. So we are doing a lot to accelerate the product innovation particularly the front end, the AI-powered shopping agent, which we think will transform the ease with which consumers can, for example, create a weekly shopping basket and then improve the targeting for Grab more cross-sell as well.

And by the way, GrabMore grew more than double-digits quarter-on-quarter. Overall, as a result, the grocery MTUs are growing at 2.6x the rate of food MTU growth on a year-on-year basis. So that shows you that it’s really expanding the top of our funnel, which is extra important in the age of AI in terms of generating data and deepening the long-term value relationships that we have with our consumers.

And then the order frequency that we saw were 1.8x higher than the food-only users, which illustrates that long-term value enhancement that I was speaking about. So over the long term, the North Star is very clear. We’ve got global peers, who have achieved like 20% to 40% mart penetration as a percentage of their deliveries business overall. So it’s definitely the right model that we’re pursuing.”

On Grab’s Loan Book

“We actually don’t have any issue at all in raising deposits. We’ve been really gratified at the trust that consumers have in the Grab brand, the Grab ecosystem, our capabilities to protect their money. And if you look at the pricing of our deposits, we are never the most aggressive in the market. We’re able to actually gather sufficient deposits to create the right shape of balance sheet. So there’s no point having excess deposits, particularly in this yield curve environment. So what you’re seeing is that’s carefully managing the level of deposits to make sure that we optimise for P&L purposes. If we needed to raise more deposits, we’re very confident that we can do that.”

4. Positives & Negatives

Positives:

Growth accelerated despite seasonality and fuel price concerns

Coming into earnings, one of the biggest worries was the increase in fuel prices that would affect demand across the region. Yet, transport volumes were up +32% YoY in April.

GMV also came in much stronger than expected which led to a beat in top-line expectations.

Operating leverage in action

Grab’s Adj. EBITDA margin increased from 13.7% to 16.2% YoY, which combined with GMV increasing 24% YoY led to a 46% increase in Adj. EBITDA.

This is classic operating leverage in action, and I believe we will start to see this increase exponentially in the months and years to come, especially as GFin turns profitable in H2 2026.

Advertising is becoming a real profit lever

GrabAds is becoming a core profit driver for the business. Average spend of quarterly active advertisers on Grab’s self-serve platform had average spends grow 44% YoY.

GrabAds is vital for Grab because it can lift delivery margins without hurting consumers or drivers. It is similar to how advertising improved the economics of other marketplace businesses. (Think Amazon, DoorDash, Meituan)

New product innovations are contributing to top and bottom line growth

Group orders for instance, grew by 74% YoY and has contributed significantly to deliveries growth. I discussed my take on new product innovations that were announced at Grab’s 2026 product day.

The initial reaction to the 8% commission cap appears to be overblown

Grab discussed during the earnings call that it was only applicable to 2-wheelers, which represented just 6% of total mobility GMV. Using FY2025 numbers, and assuming a 12pp cut in take-rates, it would result in a $57M drop in annualised revenue or 1.7% haircut on the group’s top-line.

Negatives:

Partner Incentives

It is never good to see partner incentives up 54% YoY. In this case, it was a necessary action to an unexpected event. In time, this will moderate, but it certainly affected the bottom-line, which led to a QoQ fall in net income.

Fuel costs are likely to remain a headwind

Management repeatedly referred to elevated fuel costs and the regional fuel crisis. Grab is supporting drivers through fuel discounts, cashback, EV transition initiatives, and government subsidy coordination.

The risk is that if fuel costs stay high, Grab may eventually have to choose between three bad options: subsidise drivers more, raise consumer prices, or accept weaker supply. None are great for margins.

Indonesia commission regulation sets a precedent and potential spillover effect

As I discussed in this piece, the worry of Indonesia’s policy, is that drivers in other Southeast Asian countries may push for similar caps. If it spreads to Malaysia, Thailand, Vietnam, Philippines, or Singapore in modified form, the valuation impact could be much larger.

GFin growth could be faster

Again, I believe Grab should be much more aggressive in growing its Financial Services business. It has to be a core growth driver that brings the group’s revenue growth closer to 30% as Monee is doing for Sea.

Grab’s management ultimately remains relatively conservative which is one of the largest drawbacks. I believe they do have shareholders’ interest at heart and are long-term thinkers, but to succeed and stake a strong claim on the financial services segment in the region, I do think they have to be more aggressive.

5. Conclusion

Overall, this was a very strong quarter for the business amidst challenges that they couldn’t anticipate or prepare for. Grab stock is down over 25% YTD due to concerns over fuel prices and general weakness in emerging markets.

This quarter has put to bed many of these concerns.

That said, fuel will continue to be a headwind for the foreseeable future.

While fuel will continue to be a headwind for the foreseeable future, it is ultimately a short-term issue and will mean less to Grab as it transitions to EVs and AVs over the long-term. I remain optimistic and positive on Grab at these prices as I have reiterated many times.

Please feel free to read my 2026 thesis to understand why:

Thanks for reading! If you enjoyed this piece, please give it a like and consider subscribing to a tier of your choice.

As a reminder, paid subscribers receive 6-8 articles a month covering:

Earnings Reviews (Grab, Sea Limited, dLocal, Mercado Libre and more)

1-2 Deep Dives (always happy to receive suggestions)

Portfolio Review (sharing all my positions & changes)

Just yesterday, I released my Circle Deep Dive which I would recommend checking out if you are interested!

Disclaimer: The content presented in this thesis is for informational and academic purposes only and does not constitute financial advice. The analysis and opinions expressed are based on research and should not be interpreted as a recommendation to buy, sell, or hold any security. Readers should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.

Great work, It will be interesting to see if any other countries follow Indonesia and implement the 8% caps.

Superb piece, thank you.