Circle Internet Group (Deep Dive)

The Public Market Bet on Stablecoins

Circle operates the world’s largest regulated stablecoin network, and the second largest stablecoin (USDC) behind only Tether (USDT), which remains private.

Circle is undoubtedly the best public market proxy on stablecoins today. Its flagship product, USDC, is a fully reserved digital dollar that circulates across 30+ blockchain networks, effectively a protocol for dollars on the Internet.

At the end of 2025, there was $75.3 billion USDC in circulation (up 72% YoY), with on-chain transaction volume hitting nearly $12 trillion in Q4 alone (247% YoY growth).

While ~95% of Circle’s revenues today are derived from USDC, the business is diversifying its revenue streams into other areas such as Circle Payments Network, Arc, wallet infrastructure, developer services, tokenised money market products, and enterprise settlement tools.

In this piece (11,700 words), we will discuss Circle’s history, its value proposition, moat, future prospects and what I personally think of it as an investment.

Table of Contents

Company History

Value Proposition

Business Model

Product Offerings

Moats & Differentiation

Market Context & Industry Positioning

Competitive Landscape

Financials

Ownership & Management

Valuation

Catalysts & Outlook

Bull and Bear Case

GabGrowth Quality Score

Concluding Thoughts (What I am personally doing)

1. Company History

Origins and Vision (2013-2016)

Circle was founded in October 2013 by Jeremy Allaire and Sean Neville in Boston, Massachusetts, with $9 million in seed funding from Jim Breyer, Accel Partners and General Catalyst.

Allaire was already a serial internet entrepreneur. He'd co-founded Macromedia (maker of Flash) and had a front-row seat to the web, mobile, and cloud platform shifts. He also founded Brightcove in 2004, which became a major online video platform for media companies and brands, helping businesses publish and distribute video on the internet before YouTube and streaming became as dominant as they are today.

When Bitcoin emerged, he viewed it as a potential protocol for value on the internet, analogous to HTTP for information or SMTP for email.

Allaire believed that blockchain technology would eventually allow fully reserved dollars to move on the internet in an open, interoperable way, which would drive the cost of storing and moving value down to effectively zero.

However, in 2013, none of the conditions for that vision existed. Blockchain infrastructure was primitive, regulators was non-existent and banks wouldn't touch it. Consumers certainly weren't asking for internet-native money, or understood it at the time.

Therefore, Circle started with what was available, creating a consumer Bitcoin payment app called Circle Pay. The product let users buy, hold, and send Bitcoin and fiat currencies through a simple mobile interface. It was essentially a Venmo for crypto, and with Allaire’s credibility, Goldman Sachs led a $50M funding round alongside IDG Capital Partners.

In September 2015, Circle became the first company to receive New York's BitLicense, the state's newly created framework for virtual currency businesses. In April 2016, it became the first firm to receive virtual currency licensure from the British government. While competitors were moving fast and breaking things, Circle was collecting licenses. At the time, this was seen as a slow move, but looking back, was probably one of the most decisive moves.

By late 2016, Circle stopped supporting Bitcoin exchange functionality in its consumer app entirely. The company stated it was "now more than ever not a consumer bitcoin exchange" and would focus on global payments and "next-generation blockchain technology." It was the first clear signal that Allaire was pivoting toward what would become USDC.

Pivot & Costly Mistakes (2017-2019)

The next phase of Circle's history is messy, costly, and absolutely critical to understanding the company today.

In February 2018, riding the crypto bull market, Circle acquired Poloniex, one of the largest cryptocurrency exchanges at the time for $400 million. The logic was to build a broad digital asset marketplace. Circle simultaneously raised $110 million in a Series E led by Bitmain (the Chinese mining giant) at a nearly $3 billion valuation. The company was applying for banking and securities licences, envisioning itself as a regulated crypto-financial conglomerate.

However, the 2018 crypto winter crushed trading volumes. Poloniex's ranking plummeted. The SEC began investigating tokens traded on the exchange. Circle found itself managing a regulatory minefield that distracted from its core vision. By October 2019, Circle sold Poloniex (just 18 months after buying it) at an estimated $156 million loss. It subsequently sold its Circle Trade OTC business to Kraken and its Circle Invest retail trading app to Voyager Digital.

Circle made bad mistakes and these were expensive lessons, but by stripping away all their non-core business lines, Circle was left with one product, which embodied its founding vision: USDC.

USDC had launched quietly in September 2018, co-created through the Centre Consortium, a joint venture between Circle and Coinbase. Each USDC token was fully backed by U.S. dollar reserves, issued on the Ethereum blockchain, and designed to be the kind of boring, transparent, fully reserved digital dollar that institutions could eventually trust. In its first few months, over 100 crypto-focused businesses adopted USDC, but it was still tiny, mostly a niche settlement tool for the digital asset ecosystem.

COVID Growth and the SPAC Era (2020-2022)

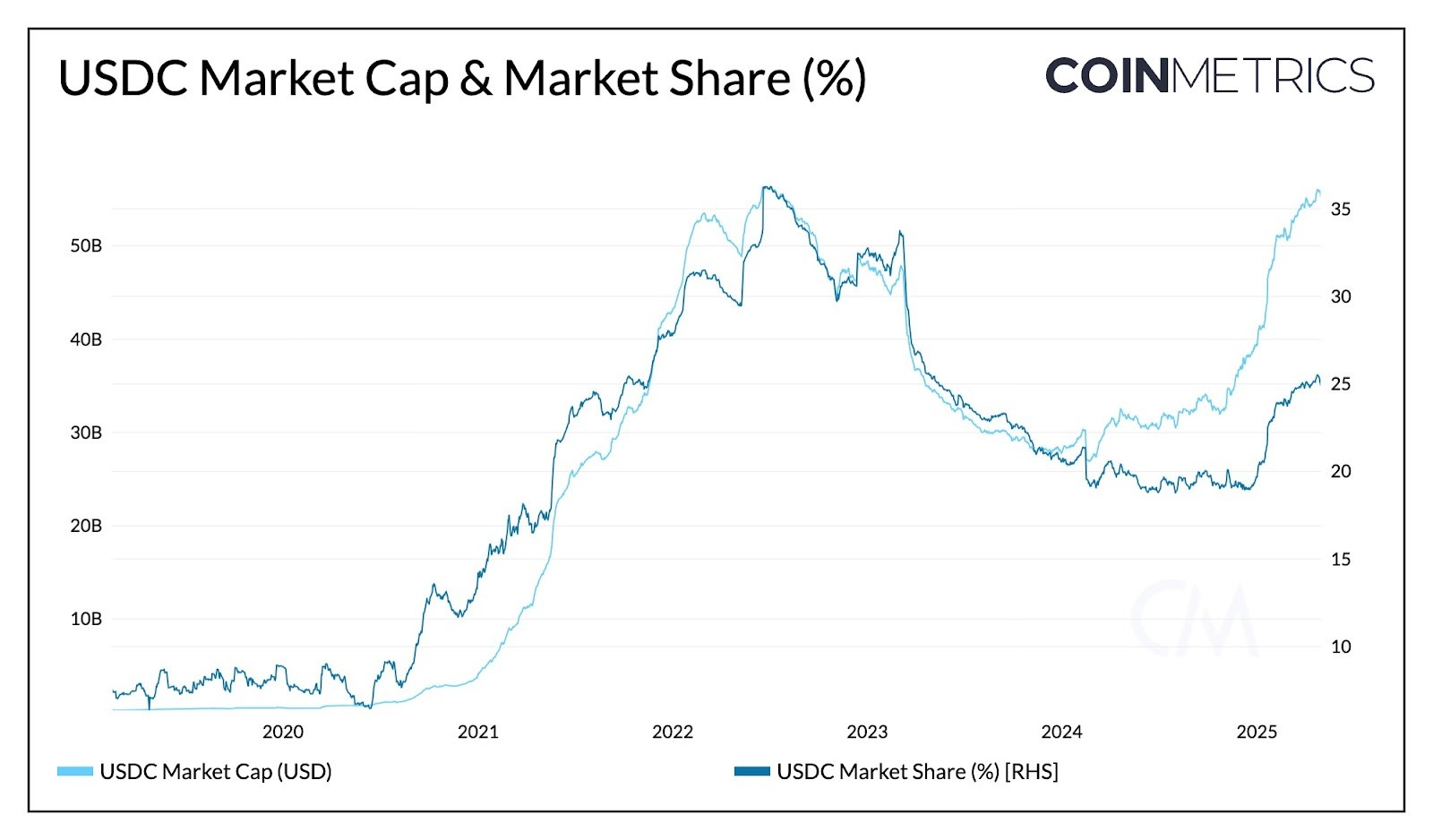

COVID-19 was an accelerant for digital dollars just as it was for digital commerce. As the world moved online, demand for on-chain settlement surged. USDC circulation grew from roughly $4 billion at the start of 2021 to $52.5 billion by early 2022, a staggering 13x increase in barely a year. Circle went from interesting niche player to systemically important infrastructure almost overnight. Its market share surged during this period to as high as 35%.

In July 2021, Circle announced plans to go public via a SPAC merger with Concord Acquisition Corp, initially valued at $4.5 billion. By February 2022, with USDC's circulation having more than doubled since the deal was announced, the terms were renegotiated to $9 billion.

Then the crypto industry imploded. Terra/Luna collapsed in May 2022, wiping out over $60 billion. Celsius and Three Arrows Capital failed. FTX, once valued at $32 billion, went to zero in November 2022. The SEC, understandably spooked, delayed qualification of Circle's SPAC filing. In December 2022, Circle and Concord mutually terminated the merger agreement.

The path to public markets was dead. But the worst was yet to come. On March 10, 2023, Silicon Valley Bank collapsed. Circle disclosed that $3.3 billion of USDC's cash reserves, roughly 8% of the total backing, were trapped at the failed bank. USDC immediately broke its dollar peg, plunging to $0.87 over the weekend. In a single week, investors redeemed a net $6 billion out of USDC.

This was an existential moment. Had the FDIC not backstopped SVB deposits that Sunday night, Circle could have faced a permanent shortfall in its reserves. The peg recovered within days once the government guarantee was announced, but the damage to market confidence was severe. USDC circulation, which had already been declining from its $55 billion peak, continued falling to a low of roughly $24 billion by late 2023. Tether, which had no direct U.S. banking exposure, surged to over 70% stablecoin market share.

The SVB episode is essential context for understanding Circle today. It exposed a genuine vulnerability (counterparty risk in reserve custody) that Circle has since addressed by shifting the vast majority of reserves into short-term U.S. Treasuries managed by BlackRock.

However, it also demonstrated something important about the network. Even after the worst stress test imaginable, USDC didn't die. It de-pegged, bled assets, and then stabilised and began rebuilding. It proved the stickiness of the underlying network effects and that it had true resilience.

Refocusing, IPO, Platform Expansion (2023-Now)

The 2023-2024 period was Circle's rebuilding phase. The company cut staff, discontinued non-core investments like SeedInvest (sold to StartEngine), and narrowed its entire focus to stablecoin infrastructure. Revenue remained strong during this period driven by high interest rates on the reserve portfolio ($1.45B in 2023 and $1.68B in 2024). Circle started generating real profits from what was now a clean, focused business.

In April 2025, Circle filed its S-1 for a traditional IPO. By June 2025, the company listed on the NYSE under the ticker CRCL. After years of false starts and near-death experiences, Circle was finally public.

Circle stock CRCL 0.00%↑ was priced at $31 per share but was heavily oversubscribed and eventually opened at $69, closing the day at $83. In the subsequent few weeks, Circle traded as high as $289.99, an incredible 4.2x from the opening price. Circle has since been in a significant drawdown as crypto experiences a bear market again, falling to as low as $50 in February this year.

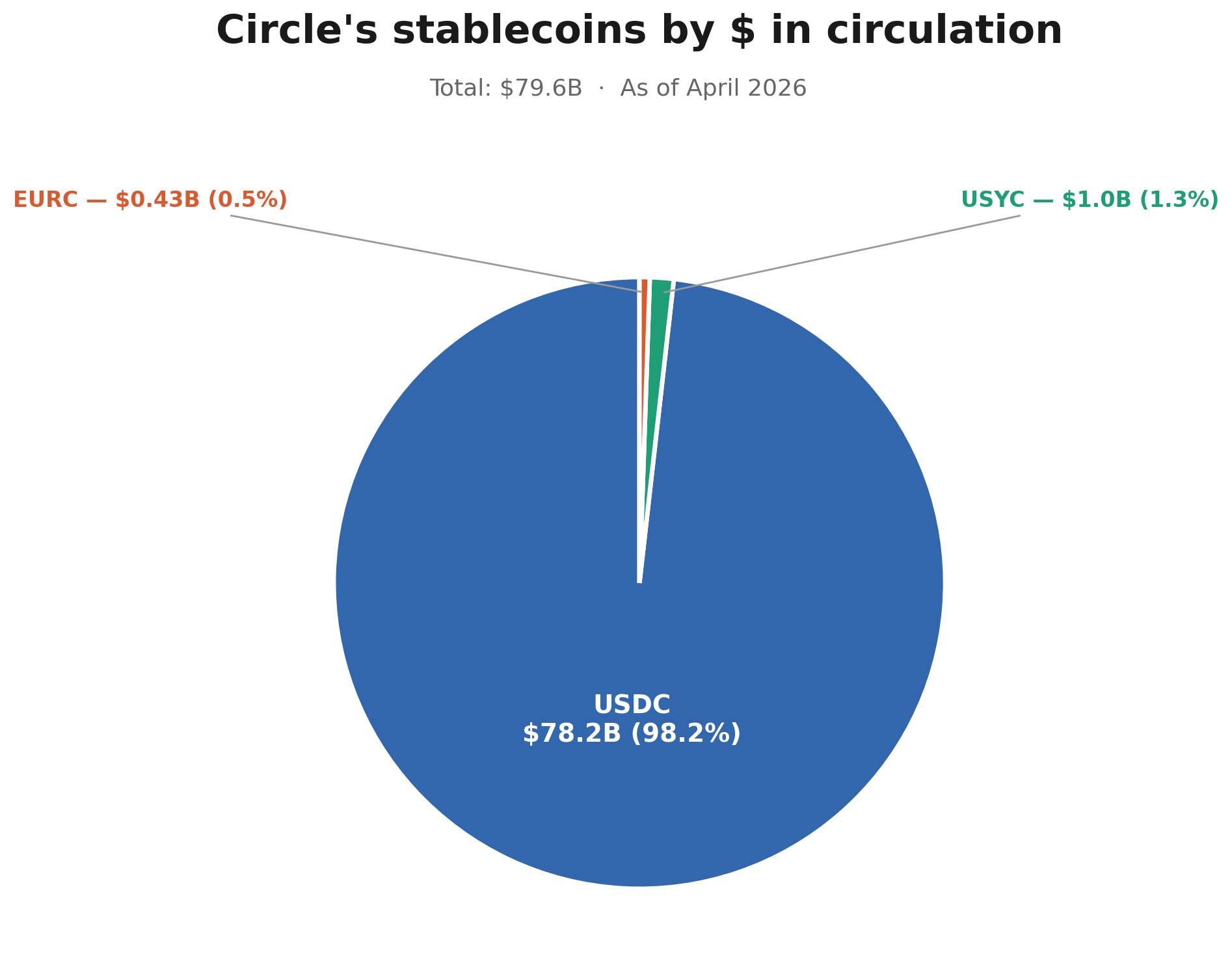

Today, the core layer remains USDC, which by year-end 2025 had rebounded to $75.3 billion in circulation, up 72% year-over-year, with nearly $12 trillion in on-chain transaction volume in Q4 alone. Circle also issues EURC (the largest regulated euro stablecoin at €310 million) and acquired Hashnote to gain USYC, a tokenised money market fund that grew to roughly $1.7 billion.

Below that, Circle launched Arc in Q4 2025, a new Layer 1 blockchain designed as an economic operating system for regulated financial activity, with over 100 major companies in its testnet including Goldman Sachs, Deutsche Bank, Visa, and Mastercard. Arc is pre-revenue and pre-mainnet. It's a bet on the future, not a contributor to today's financials.

Above the core, Circle built Circle Payments Network (CPN), an application layer for cross-border money movement. By February 2026, CPN had 55 financial institutions enrolled, $5.7 billion in annualised volume, and was live in 14 markets with 11 more planned. It also launched StableFX in production beta for on-chain foreign exchange.

The evolution from Bitcoin wallet to crypto exchange to stablecoin issuer to full-stack internet financial platform is what I believe most investors miss when they look at Circle's simple-looking P&L. The 13 years of regulatory groundwork, painful pivots, and infrastructure investment have formed the foundation of the business, and is the moat today.

2. Value Proposition

Before we start with Circle’s value proposition, it is important to discuss the value proposition of stablecoins and how they work, as it is crucially important to the Circle thesis.

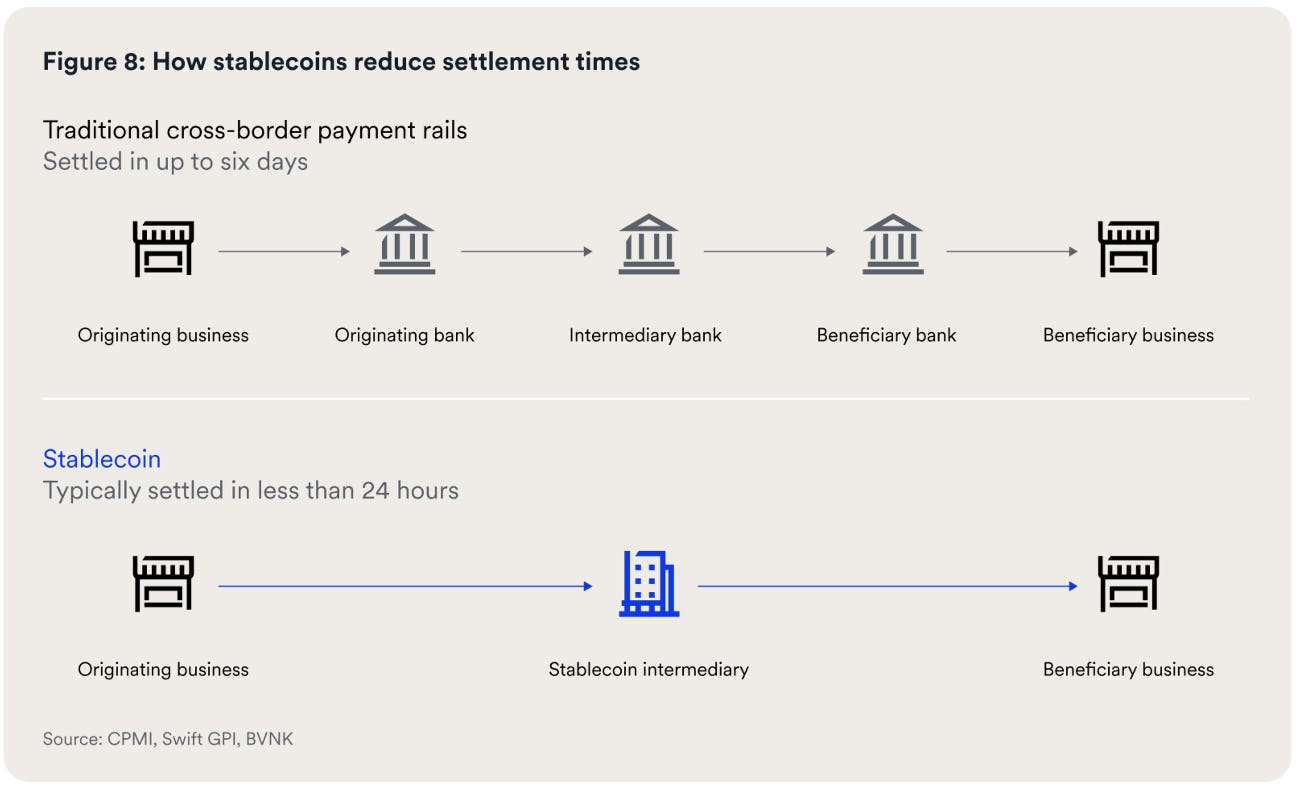

Moving money on the internet is still shockingly slow. A wire transfer takes 1 to 3 business days. It costs $25 to $50. Cross-border is even worse due to correspondent banks, FX spreads, compliance checks, and 3 to 5 day settlement windows. The system runs on bank hours which closes on weekends and this hasn't meaningfully improved in decades.

Stablecoins close that gap. A stablecoin is a digital token on a blockchain, pegged 1:1 to a real currency like the US dollar. For every token in circulation, there's a matching dollar sitting in reserve, typically held in cash and short-term US Treasuries. You can think of it as a dollar that lives natively on the internet.

When you send a stablecoin from Singapore to Argentina at 2am on a Sunday, it settles in seconds, costs fractions of a cent with no banks in the middle. There is no waiting for business hours and the blockchain is the settlement layer which never closes.

This matters for 3 reasons:

Speed and Cost. Stablecoins do what the traditional banking system does, but faster and cheaper. A cross-border payment that used to take days and cost tens of dollars now takes seconds and costs nearly nothing. For businesses moving money globally, this is a step change improvement.

Access. Most of the world doesn't have easy access to dollar-denominated savings or payments. In countries with high inflation, capital controls, or weak banking infrastructure, a dollar-pegged stablecoin on a phone is transformative as it acts as a savings account, a remittance rail, and a payment method in one.

Programmability. Unlike a dollar in a bank account, a stablecoin can be programmed. For instance, it can be held in escrow and released automatically when goods are delivered. It can also be streamed as payroll by the second or used as collateral in lending protocols.

The stablecoin market is around $320 billion today, with projections to reach trillions of dollars in a few years. Transaction volumes could hit $100 to $200 trillion annually, while Visa and Mastercard are already integrating stablecoin settlement. Stablecoins are a game changer and have a very enticing value proposition.

Circle's value proposition is fundamentally different from most FinTech companies because it doesn't serve end consumers directly. Instead, it is infrastructure that enables services to be built on top of it. This distinction matters enormously for understanding who Circle actually creates value for and why the network keeps growing without Circle needing to acquire every user itself.

For Developers and Technology Companies:

If you're building any product or service that needs to move, store, or programme dollars on the internet, USDC is essentially the default choice. It operates across 32 blockchain networks, more than any other stablecoin, making it the most portable and interoperable digital dollar available. Circle provides SDKs, APIs, smart contract templates, and programmable wallets that allow developers to embed dollar-denominated financial functionality into their products without needing to build banking infrastructure from scratch.

This is a massive unlock. A startup in Southeast Asia building a remittance app doesn't need to negotiate with correspondent banks, obtain money transmission licences in every jurisdiction, or build settlement infrastructure. They can integrate USDC and plug into a globally available, near-instant, near-free payment rail that already has deep liquidity. The same applies to AI developers who need their agents to make and receive micro-payments, e-commerce platforms that want to offer stablecoin checkout, or capital markets firms building tokenised products that need a cash settlement layer.

Importantly, most of these integrations happen without any commercial relationship with Circle. Tens of thousands of products and services use USDC today, and the vast majority simply build on the open protocol. This organic, developer-driven adoption is what creates the utility network effect and makes USDC’s position so hard to displace.

For Financial Institutions:

This is the cohort that I believe will drive the next phase of Circle's growth, and where the value proposition is most compelling relative to the legacy system.

To understand this, we have to give an analogy of what cross-border money movement looks like today. A business in Portugal sending payment to a supplier in Brazil goes through multiple correspondent banks, each taking a cut, with settlement that can take days, requires pre-funded nostro/vostro accounts, and involves significant FX spread on top.

The capital tied up in these intermediary positions is enormous. For instance, JPMorgan alone moves north of $10 trillion per day in gross money settlement.

Stablecoins collapse this entire chain as settlement happens in seconds. There's no pre-funding requirement because the value moves atomically. The capital efficiency gain is what’s driving major institutions to Circle’s doorstep. Firms like Fiserv, FIS, Corpay, and Matera, infrastructure providers that serve tens of thousands of banks, have all announced integrations with Circle's technology. Visa and Mastercard have launched products around USDC settlement. Even G-SIBs are leaning in to improve their own international money movement using stablecoin rails.

What Circle offers these institutions is not just the stablecoin itself, but the trust infrastructure around it. Circle holds regulatory licenses across 49 U.S. states plus dozens of international jurisdictions. It also has elite reserve transparency (BlackRock-managed Treasuries, audited monthly) and conditional approval for a National Trust Bank charter. No other stablecoin issuer comes close on this dimension.

For Enterprises and Corporates:

Large enterprises that operate across geographies face constant friction in treasury management, collecting revenue in multiple currencies, repatriating funds, managing FX exposure, dealing with settlement windows and bank cut-off times. USDC offers a way to unify treasury operations onto a single, programmable rail. We're seeing adoption from firms like Brex, Deel, and Gusto for payroll and corporate payments, and from companies that want to move money across subsidiaries without waiting for SWIFT to process.

For Dollar-Hungry Populations:

This is perhaps the most under-appreciated use case. In countries with high inflation, capital controls, or unstable banking systems, holding dollars is not really an investment, but a priority for survival. USDC provides a way for individuals and businesses in these markets to access, hold, and transact in dollars without needing a U.S. bank account.

Allaire has spoken about this as a continuation of American monetary policy goals. For instance, the GENIUS Act itself was partly motivated by the strategic value of extending dollar reach globally through digital means.

3. Business Model

At a high level, Circle's business model today is very simple. The target is to grow the amount of USDC in circulation, earn yield on the reserve assets backing it, and re-investing a portion of that yield into distribution partnerships and platform expansion to grow circulation further. A perfect flywheel.

However, it isn’t that simple of course. There are important nuances around distribution economics, margin structure, and the emerging revenue lines that will determine whether Circle can evolve from a one-dimensional reserve income business into a multi-revenue platform.

Reserve Income (The Core Engine)

Circle holds cash-equivalent assets, primarily short-term US treasuries and repurchase agreements managed by BlackRock to back every USDC in circulation. It earns the prevailing short-term interest rate on these reserves. In Q4 2025, the reserve return rate was 3.81%, down 68 basis points year-over-year as SOFR declined.

This is the business in its simplest form. More USDC in circulation x the risk-free rate = more revenue. In Q4 2025, total revenue and reserve income was $770 million, up 77% year-over-year, driven overwhelmingly by the growth in average USDC circulation (which ended the year at $75.3 billion, up 72% YoY) partially offset by the lower reserve rate.

The obvious bull case here is volume growth. Circle's own internal model assumes a 40% CAGR in USDC circulation, which they describe as their "conservative" base case. Third-party research CAGRs range from 25% at the low end to 90%+ at the high end, with a median around 60%.

The equally obvious risk is interest rate sensitivity. If the Fed cuts aggressively and short-term rates fall to, say, 2%, Circle's revenue per dollar of USDC roughly halves. This is the single biggest vulnerability in the current model and the reason why diversifying into non-rate-dependent revenue is strategically critical.

Distribution Costs (The Coinbase Question)

This is where the P&L gets complicated and where I think most investors should spend their time.

Circle doesn't acquire most of its USDC circulation directly. It grows distribution through partnerships with exchanges, wallets, neobanks, payment companies, and other financial institutions. Many of these partnerships involve revenue-sharing arrangements where Circle pays a portion of reserve income to the partner as an incentive to hold and distribute USDC on their platform.

The largest and most scrutinised of these is the Coinbase relationship. Coinbase took an equity stake in Circle and is the co-creator of the original Centre Consortium. Under their agreement, Coinbase receives a share of reserve income on USDC held on its platform. As Coinbase holds a significant portion of total USDC circulation, this is a material cost line. In Q4 2025, total distribution, transaction, and other costs were $461 million (roughly 60% of gross revenue).

The resulting metric that matters is RLDC margin (Revenue Less Distribution Costs). In Q4 2025, RLDC margin was 40.1%, up modestly quarter-over-quarter. For FY 2025, RLDC margin was 39.4%, exceeding the company's guidance of approximately 38%.

There are two ways to think about this. The bear case and the bull case.

The bear case is that RLDC margins stay compressed or get worse as Circle has to pay more partners to drive growth, essentially giving away the economics to grow a network it doesn't fully control. This is a structural disadvantage that Circle faces due to its position of dependency.

The bull case is that three tailwinds provide structural support to RLDC margin over time. First, growing network effects mean that as USDC becomes more dominant, new partners integrate it organically without needing incentive deals. Many products are built and launched using USDC without any commercial relationship with Circle. The stronger the network, the less Circle has to pay to grow it. Second, growth in on-platform USDC (i.e., dollars held within Circle's own infrastructure rather than on partner platforms) that carries better economics. On-platform USDC grew 5.6x YoY to $12.5 billion at year-end, representing 17% of total circulation, up from roughly 3% a year prior. Third, growth in other revenue (covered next) adds high-margin dollars on top of the reserve income base, improving blended margins.

Other Revenue (The Emerging Layer)

Circle has begun monetising transaction flows and network infrastructure beyond pure reserve income. In FY 2025, other revenue reached $110 million, exceeding their guidance of $90-$100 million. These revenues come from two buckets.

Subscription and services revenue is primarily from blockchain network partnerships. When Circle deploys USDC onto a new blockchain, it often receives both upfront integration fees and ongoing recurring revenue. Circle added 12 new chains in 2025. This revenue stream is relatively “lumpy” because of the upfront component, although the recurring base is growing steadily underneath.

Transaction revenue comes from blockchain rewards (Circle runs validator infrastructure, including a super validator on the Canton Network), USYC redemption fees, and emerging payments-related fees. The Canton Coin trading launch drove an outsized Q4 contribution.

What matters most about this revenue segment is not the dollar amount ($110M). Rather, it is that these revenue streams are high margin and scale with network adoption and transaction volume rather than interest rates. For FY 2026, Circle guided other revenue of $140-$160 million, implying 27-45% growth. I think this is conservative given the pipeline of new products (CPN monetisation, Arc Mainnet fees, StableFX), but the base is still small relative to reserve income. This segment needs to scale meaningfully before it moves the needle.

4. Product Offerings

Circle's products span four core areas today, with two emerging platform layers that are pre-revenue but strategically important to the thesis.

USDC (The Core)

This is very much the core revenue driver for the business. USDC is a fully reserved digital dollar that operates across 32 blockchain networks. Every token is backed 1:1 by cash-equivalent assets, primarily short-term U.S. Treasuries and repurchase agreements managed by BlackRock. 96% of total revenues in 2025 came from reserve income, tied directly to stablecoins, of which USDC is the largest driver by far.

The question is, what gives USDC a moat? Why can’t other players simply enter with their own stablecoins and take share?

The beauty of USDC lies with the infrastructure stack built around it.

Circle Mint provides enterprise-grade minting and redemption, the primary market where institutions can create or destroy USDC by depositing or withdrawing dollars through Circle's banking infrastructure.

Circle has facilitated over $1 trillion in mint/redeem volume since 2018, and in Q4 2025 alone, mint/redeem volume was $163 billion. This primary liquidity, backed by relationships with systemically important banks globally, is one of Circle's deepest moats.

CCTP (Cross-Chain Transfer Protocol) is another critical piece of USDC infrastructure. It enables native burning and minting of USDC across blockchains, eliminating the need for "wrapped" or "bridged" versions that introduce counterparty risk. CCTP volume grew approximately 640% year-over-year in Q3 2025 to $31.3 billion. By Q4, CCTP represented over 50% of all bridged volume across all assets and all bridge providers, not just USDC.

EURC (Euro Stablecoin)

EURC is the largest regulated euro-denominated stablecoin, with €310 million in circulation at year-end 2025, up 3.8x year-over-year. This is still small in absolute terms, especially when compared to USDC.

As CPN scales cross-border payments, having native stablecoin pairs for on-chain FX (dollar-to-euro, dollar-to-other currencies) becomes a building block for payments infrastructure. Circle was the first stablecoin issuer to register as an Electronic Money Institution under MiCA in the EU, which gives EURC a regulatory head start in Europe.

I’m skeptical on the take-up rate of non-USD stablecoins in an environment where even European, Asian and South American users typically use USDC/USDT.

USYC (Tokenised Money Market Fund)

USYC is a tokenised U.S. Treasury and money market product that Circle acquired through its purchase of Hashnote in January 2025. It grew to approximately $1.7 billion and became the second-largest tokenised money market fund in the world. USYC is designed to serve as yield-bearing collateral in digital asset markets.

Institutions can hold USYC to earn yield and seamlessly swap into USDC when they need cash for trading or settlement. The integration with Binance to accept USYC as collateral in June 2025 was seen as a significant milestone. Circle's long-term vision is that the architecture of "yield-bearing collateral + digital cash" will become the standard for capital markets, on both crypto-native and traditional exchanges.

Personally, I’m not convinced that either EURC or USYC will be significant contributors. I think investors have to view both of these as call options and not ascribe any value to it. For the foreseeable future, USDC is and will remain the core driver for reserve income.

Circle Payments Network (CPN)

CPN is an application layer for cross-border money movement built on top of the stablecoin network. It is essentially the SWIFT of the stablecoin world.

As of February 2026, CPN had 55 enrolled financial institutions (up from 29 in Q3 2025), with 74 more in eligibility reviews and a pipeline of over 500. It was live in 14 markets with 11 more planned. Annualised payment processing volume (PPV) reached $5.7 billion, up 68% since the prior quarter.

The initial use cases for CPN are B2B cross-border merchant settlement (businesses exportign from Asia and importing into emerging and developed markets), along with south-to-south and north-to-south remittance applications.

What makes CPN architecturally different from Visa or SWIFT is that it's an open, extensible network. Third-party developers can deploy modules onto CPN. The first third-party apps are already launching, including a trade receivable credit module. Circle has built a refund protocol (transaction reversibility) and a companion insurance protocol for underwriting reversals. These are composable building blocks that don’t exist in closed payment networks.

CPN is still not monetised yet. Circle is currently focused on growing the network and its flows, with monetisation expected to follow as scale develops. I think this is the right call strategically.

Arc (Layer 1 Blockchain)

This is Circle’s most ambitious and speculative product. Arc is a new Layer 1 blockchain purpose-built for regulated financial activity. Layer 1s are notoriously competitive. Thousands of Layer 1s have been built in the past, but as of today, only a handful have succeeded. Arc’s angle here is to include sub-second deterministic settlement finality, low-cost USDC-denominated gas fees, and configurable privacy controls with opt-in confidential transfers. To put it in layman terms, it means to be very quick, very cheap, payable in USDC for zero complexity, and to allow for privacy.

Arc launched into public testnet in Q4 2025 with over 100 companies participating including Goldman Sachs, Deutsche Bank, Visa, Mastercard, Apollo, AWS, BlackRock, HSBC, and Standard Chartered. The testnet achieved near-100% uptime, half-second settlement finality, and over 166 million total transactions. Mainnet launch is planned for 2026.

Circle is also exploring a native token for Arc to drive utility, incentives, and governance. This hasn't been confirmed, but if launched, it could represent meaningful additional value for Circle, though it also introduces complexity around token economics and regulatory considerations.

The truth is that Arc remains entirely pre-revenue and is a speculative project. It could be a potentially transformative new business segment, but I do not expect it to be a needle-mover anytime soon. I will discuss the bull and bear case for this in later segments.

Developer Tools & Infrastructure

Apart from these consumer-facing products, Circle also provides a full stack of services for developers from programmable wallets, a smart contract platform, Circle Gateway for cross-chain USDC activities, and xReserve for supporting USDC expansion across blockchain ecosystems.

These are underrated tools that help to make the rest of the product stack usable for enterprises, especially those that have never touched blockchains before. These tools are not monetised and therefore won’t show up in financial statements, but are essential to the platform strategy.