Sea Limited Q4 2025 Earnings Review

The Real Reason Behind the Selloff

Revenue: $6.85B v $6.43B (+38.4% YoY) 🟢

EPS: $0.63 v $0.62 (+61.5% YoY) 🟢

Selected Key Metrics

Total Gross Profit: $3.0B (+36% YoY)

Total Net Income: $410.88M (+72.9% YoY)

Total Adjusted EBITDA: $787.14M (+33.2% YoY)

Cash & Cash Equivalents: $11.1B (up from $10.4B in Q4 2024)

E-Commerce (Shopee)

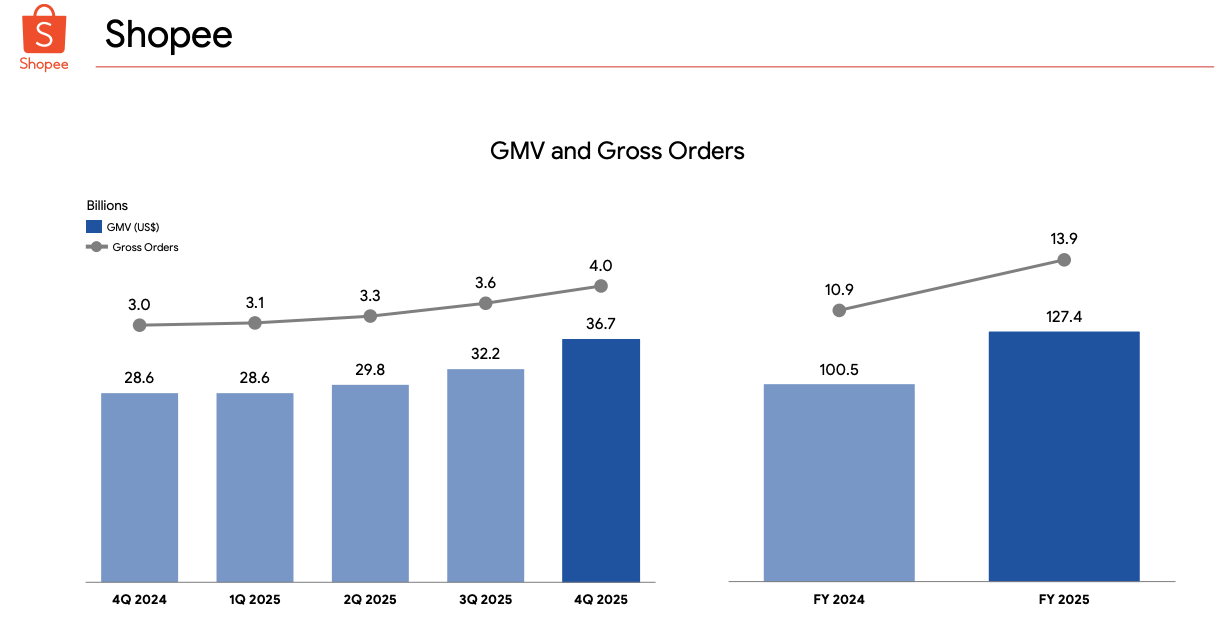

Gross Orders: 4.0B (+30.5% YoY)

GMV: $36.7B (+28.6% YoY)

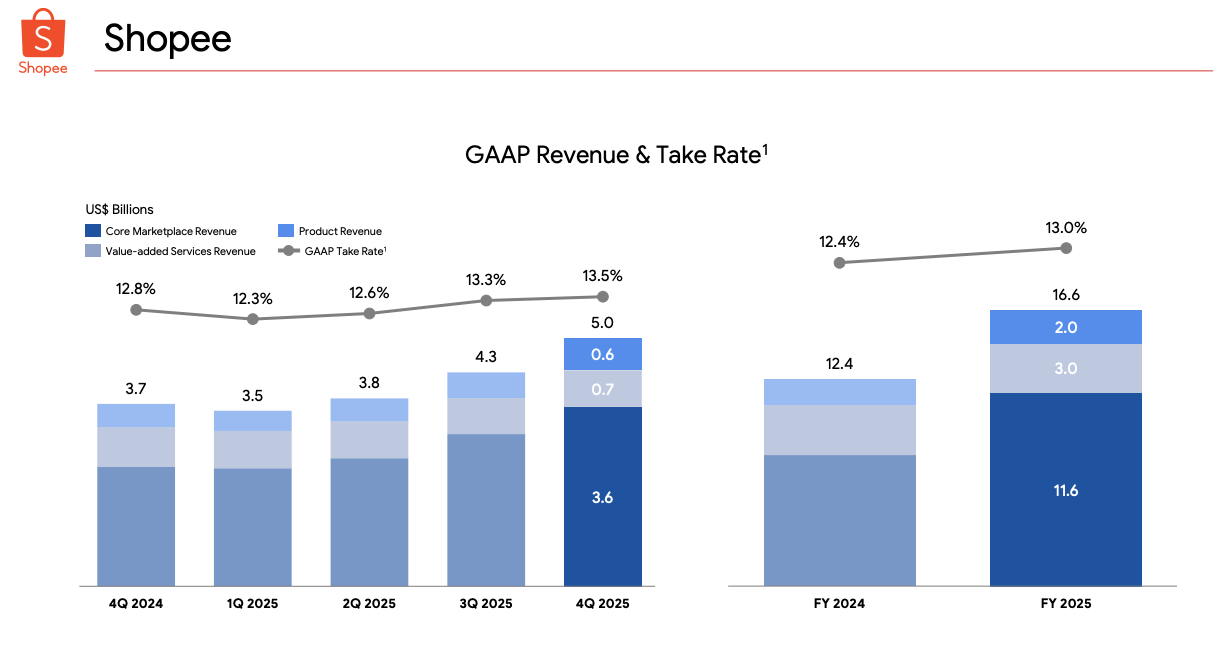

Revenue: $5.0B (+35.8% YoY)

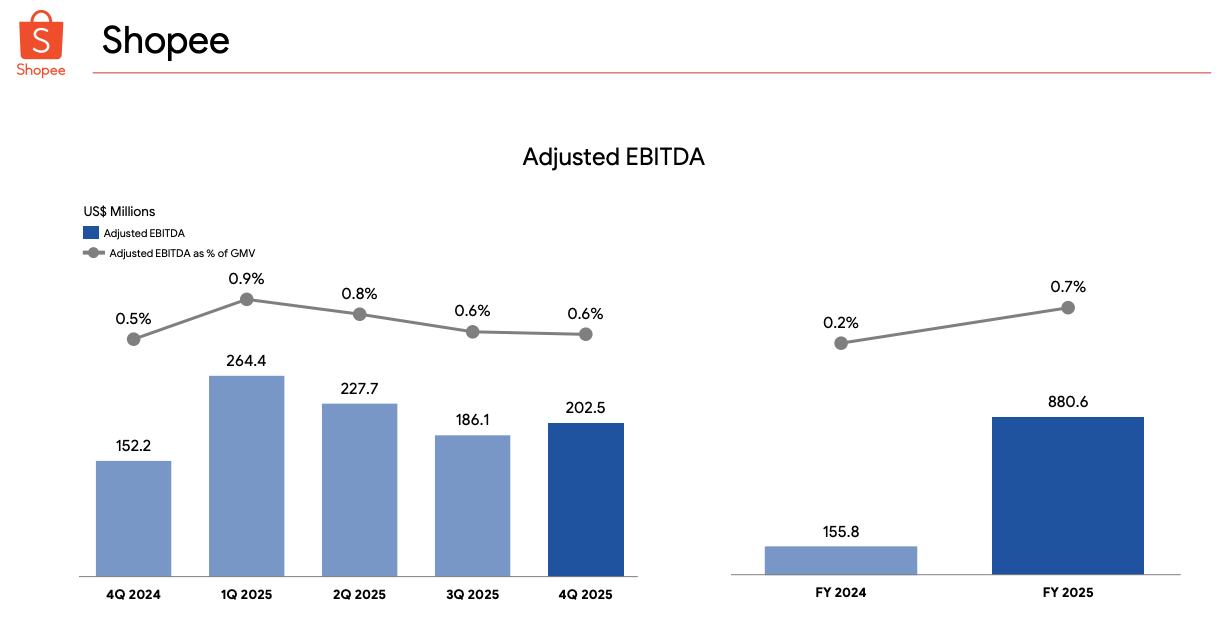

Adjusted EBITDA: $202.5M (+33% YoY)

Digital Financial Services (Monee)

Consumer & SME Loans Outstanding: $9.2B (+80.4% YoY)

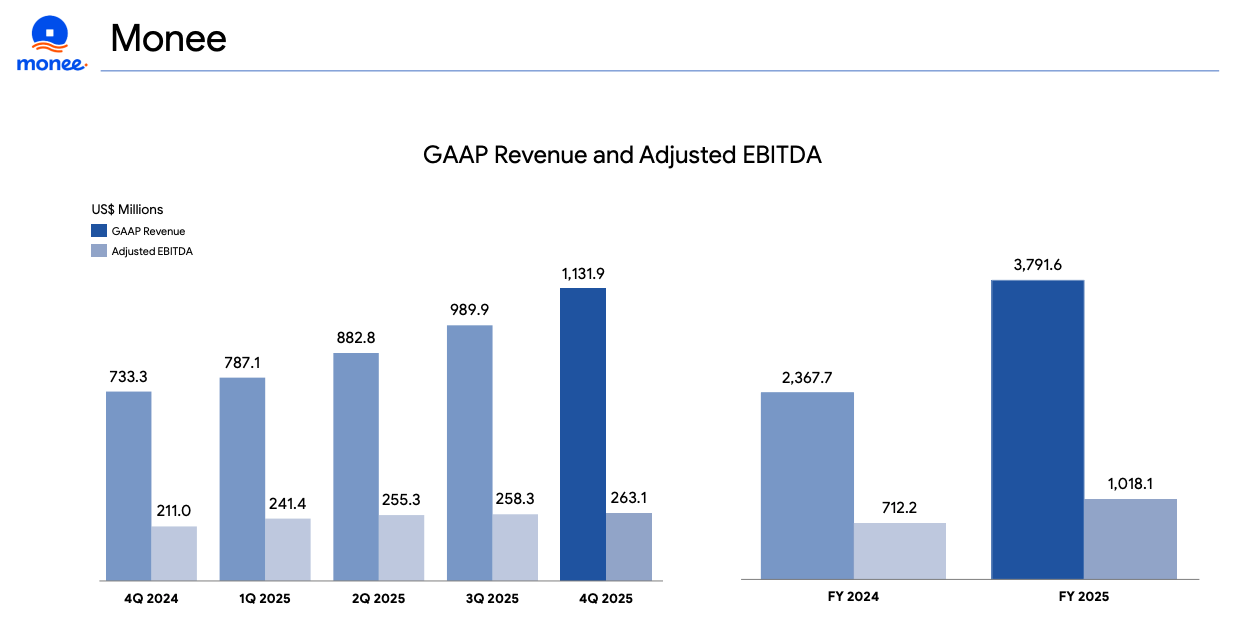

Revenue: $1.13B (+54.3% YoY)

Adjusted EBITDA: $263.1M (+24.7% YoY)

Digital Entertainment (Garena)

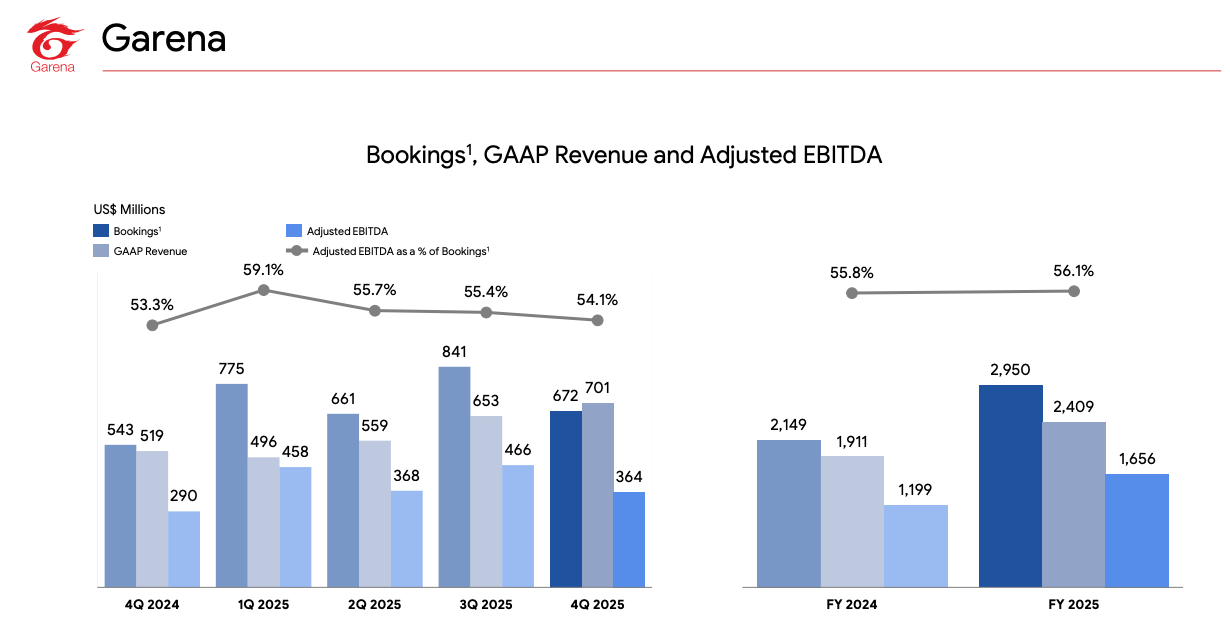

Bookings: $672.4M (+23.8% YoY)

Revenue: $701.0M (+35.1% YoY)

Adjusted EBITDA: $363.8M (+25.6% YoY)

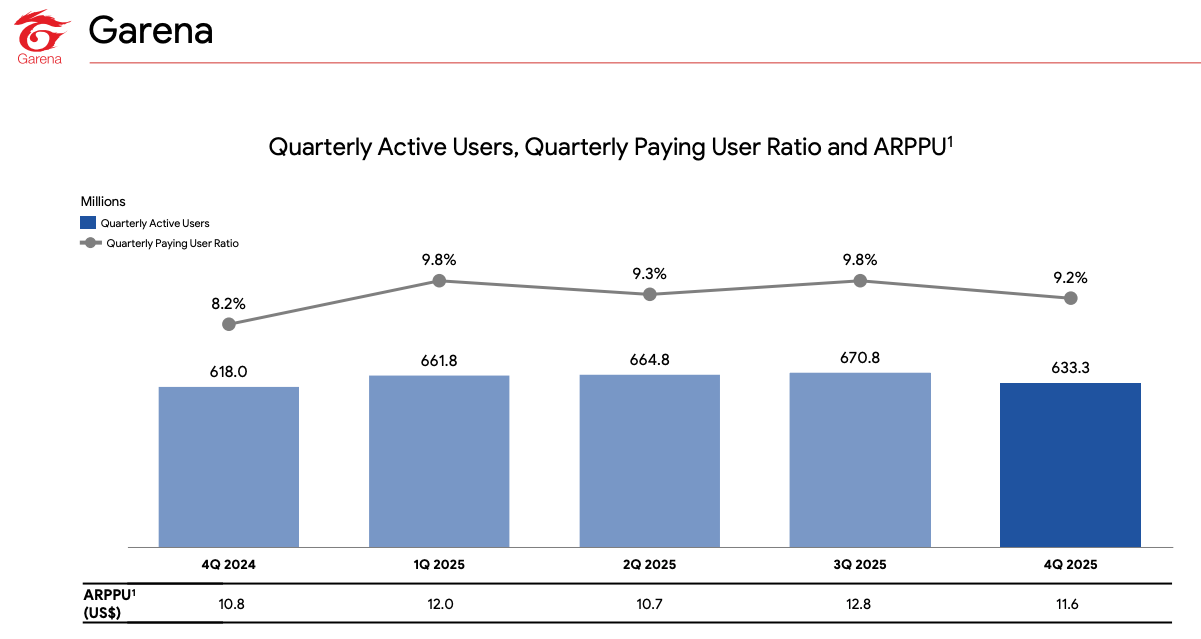

Quarterly Active Users: 633.3M (+2.5% YoY)

Quarterly Paying Users: 58.0M (+15.0% YoY)

Sea Limited beat on the top and bottom-line, though consensus estimates for the bottom-line range widely due to the lack of sell-side coverage on the stock.

As I’ve discussed often, my base case is >20% growth for the decade to come. I don’t see any signs of it slowing so far. In Monee, Sea has a business that is now reaching scale to move the needle. Shopee is not slowing down either with 25% GMV growth guidance and Garena guiding for double-digit growth again.

In this piece, I will break down the full report, earnings call and discuss my personal thoughts on the quarter.

Table of Contents

Shopee (E-Commerce)

Monee (Digital Financial Services)

Garena (Digital Entertainment)

Management Commentary

Concluding Thoughts

1. Shopee (E-Commerce)

Shopee’s GMV continued climbing to record highs, with GMV now at an annualised $146.8B run-rate. Sequentially, GMV grew 14% QoQ, compared to 4% QoQ in Q2 2025 and 8% QoQ in Q3 2025, signalling yet more acceleration in the business.

For FY2026, Shopee is guiding for 25% GMV growth. This was above sell-side consensus of 19%, which is obviously great news. Personally, I thought management would guide for 20% GMV growth as they did last year (eventually raising to 25% mid-year and then closing the year at 26.8%), so I am very happy with 25%.

Shopee’s GAAP take rate continued to climb, up to 13.5% this quarter. This brings FY2025 take rate to 13%, up 60bp from FY2024. Again, this was expected, as I predicted in last quarter’s review.

There is still much more room for take rate to go up and I expect this to continue, albeit with some quarter to quarter fluctuation.

Of course, what concerned the market in particular in Q3 2025 was Adj. EBITDA margins for Shopee. This continued into Q4 2025, with 0.6% margins, compared to Q1 highs of 0.9%.

Management guided for “full year adjusted EBITDA no lower than that of 2025 in absolute dollar terms”. This spooked the market as that would mean 0.55% margins for FY2026, compared to sell-side analysts consensus at 0.9%.

Personally, I am of the belief that management is sandbagging guidance here. For instance, when we look back to Q4 2024 where management shared guidance for FY2025, here is what they said:

“We remain confident about our ability to continue delivering profitable growth in 2025 and expect Shopee’s full year 2025 GMV growth to be around 20%, with improving profitability.”

In actuality, top-line beat massively (28.6% v 20%) while Adj. EBITDA for Shopee actually grew 465% (slightly more than improving profitability).

Yet, a lot of this will depend on the rollout of the Shopee VIP program, the equivalent of Amazon Prime. Shopee has been re-investing heavily into their logistics network and anecdotally, I have noticed a very aggressive push for the VIP program. This could be leading to short-term margin pressure, which will continue for a quarter or two, hence the cautious guide.

Shopee Ads

In Q4 2025, ad revenue grew 70% YoY and ad take rate increased by over 80bps. Ad-paying sellers increased by over 20% YoY and their average ad spend increased by over 45% YoY.

Ads will be an increasingly large contributor to the bottom-line and I believe next year should be a key inflection point.

Shopee Logistics (SPX Express)

Management shared that SPX Express now processes on average over 30 million parcels a day. This ranks it 2nd in the region, behind J&T Express which is the key supplier for Shopee’s main rival: TikTok Shop.

Shopee has begun expanding instant delivery into additional use cases, including partnering with local supermarkets and suppliers to deliver fresh groceries in Thailand in as little as 1 hour.

Management shared that buyers using instant and same-day delivery spend around 15% more on average after adoption, this is to be expected as I have shared in the quick commerce deep dive.

“We scaled economical shipping to serve buyers seeking affordability. In Indonesia, orders using economical shipping more than doubled year-over-year in the fourth quarter. With our delivery capability well-scaled, we started to roll out fulfilment service in various markets across 2025. We are seeing encouraging adoption trends from both buyers and sellers, with double-digit order penetration in some markets. In 2026, we plan to expand fulfilment further across all our markets and aim to double our fulfilment order penetration by the end of the year.”

-Forrest Li, CEO of Sea Limited

Shopee VIP

In Q3 2025, management revealed that there were over 3.5 million Shopee VIP members, growing 75% QoQ. In Q4 2025, this went up to over 7 million members, implying 100% QoQ growth.

It is clear that management is prioritising Shopee VIP as a means of access to stable revenue/earnings and a sticky user base. I am fully in support of this, though it will likely lead to continued weakness in margins.

Management shared that across every market it has launched, the program has consistently produced double-digit spending uplift by members after joining and in Indonesia, VIP members have been spending 30-40% more than before joining. In fact, in some markets, VIP members already contribute to more than 15% of total GMV in Q4. This is massive when you consider it is just 1.75% of users.

There is still much room for growth re: the Shopee VIP program. Management shared that in 2025, Shopee served around 400 million active buyers. This implies that Shopee VIP is only at a 1.75% penetration rate. For reference, here are the take-up rates of other popular e-commerce subscription services:

Amazon Prime: 65%

Coupang Rocket WOW: 65-68%

Walmart+: 43%

Alibaba 88VIP: 5%

JD Plus: 4-5%

There is huge variability here, with the likes of Amazon Prime, Coupang Rocket WOW offering many more services than just free shipping. However, it is clear that Shopee has huge runway to go.

Interesting to note too, is the synergy between Monee and Shopee in enabling a successful subscription business here. Chris Feng (President of Sea) noted during the call that historically, one of the core challenges for similar programs in the region, is the payment success rate month to month due to the lack of credit card availability. However, due to Monee, there is a smooth payment process for the VIP program, which has led to increase in subscription retention rate from 40% to 70% in Indonesia for instance in the past few quarters.

YouTube & Meta Partnership

In Q4 2025, orders driven by YouTube content more than tripled YoY. Since the launch in October, the collaboration with Meta has seen huge success, with more than 3 million affiliates linking their Shopee and Facebook accounts.

2. Monee (Digital Financial Services)

Monee continued with yet another record quarter of loans principal outstanding. Its loan book grew ~80% YoY to $9.2B while the NPL ratio held steady at 1.1%.

Management shared that they added 5.8 million unique first-time borrowers in the quarter, up from 5 million adds in the previous quarter. Monee now has 37 million active credit users, up more than 40% YoY. Average loan outstanding per user was ~$240, up 27% YoY.

GAAP revenue for the quarter came in above $1B for the first-time. Adjusted EBITDA continued climbing, albeit at a low margin, owing to interest rate declines in SEA markets.

Importantly, Sea is continuing to grow its off-Shopee SPayLater loan book, citing over 300% YoY growth, accounting for over 15% of the total SPayLater portfolio. For FY2025, Adj. EBITDA is now over $1B. Quite a feat.

There is a concerning aspect to Monee though. Off-book loans have barely grown for a year now. While on-book loans have grown from $5.1B to $8.2B YoY, off-book loans have only grown from $0.9B to $1B. (Off-book loans principal outstanding mainly refers to channeling arrangements, which is lending by other financial institutions on Monee’s platform)

Building off-book loans takes time of course, as 3rd party financial institutions will need a few things before they’ll commit capital again. For instance, a long enough default history across economic cycles, regulatory approvals in each individual market, and typically a minimum track record on the specific product.

Right now, Sea is essentially funding most of its loan growth off its own $11B cash pile. That works while the cash is abundant, but it's capital-intensive and creates a ceiling on how fast Monee can scale without either diluting shareholders or constraining other investments.

Long-term however, off-book loans will be key. It will enable Monee to keep growing without cannibalising the rest of Sea’s strategic optionality. Distributing credit risk to 3rd party institutions also acts as a structural hedge. The market will also likely re-rate Monee meaningfully the moment off-book becomes a material portion of the funding mix.

3. Garena (Digital Entertainment)

Garena had probably the weakest results of the 3 segments. Q3 2025 was certainly an anomaly in terms of bookings numbers. Bookings for that quarter came in at $841M, which was a massive increase over Q2. Q4 was more moderated, with a slight reversion to the mean as bookings came in at $672M. GAAP revenue hit a multi-year high of $701M.

Garena remains a very lucrative cash cow for the business.

QAUs fell to 633.3M which was the lowest for the year, albeit with a modest 2.4% increase over last year. QPU ratio fell to 9.2%, also the lowest for the year, but a full point above last year’s Q4 numbers.

4. Management Commentary

This section focuses mainly on questions during the earnings call, with key highlights of what I believe are important points to takeaway. I may adjust a few words here and there for clarity purposes, (English is not the first language for the majority of Sea’s management team) but I will not change the meaning of these quotes.

On Shopee’s GMV Growth:

“If you look back, at the start of 2025 we guided for around 20% top-line growth. As the year progressed, we realised we could grow the business faster and ended up delivering well above that. In Q4, year-on-year growth was much higher than 20%.

Over the year, we identified areas where we could further drive market growth and learned which levers we can pull to accelerate it.”

On Shopee’s EBITDA margins:

“I believe we can continue expanding profitability and margins, and that this trend will persist over the years. We have previously guided toward a 2–3% margin for the e-commerce business over time, and that conviction remains. We will continue to demonstrate this to the market.

Over the medium to long term, we see a 2–3% EBITDA margin as achievable, based on what we have observed so far.”

On the Competitive Landscape:

“Regarding the competitive landscape, what we have observed is a relatively stable environment across most markets. We have not seen anything materially different from what we observed in previous quarters.”

On Shopee Brazil:

“On AOV, we believe it will grow over time. The gap versus peers may remain, but we expect it to narrow gradually.

For SPayLater penetration in Brazil, it is still at a very early stage. While we have seen strong growth, we entered Brazil much later than other markets. Current penetration levels are comparable to the early stages we observed in our initial markets. We expect penetration to continue increasing in 2026, following a trajectory similar to what we saw in our Asian markets.”

On Garena:

“Regarding Garena’s outlook, we continue to expect double-digit growth in 2026.

On the collaboration pipeline, we are very encouraged by the strong performance of our partnership with IPs such as Naruto. We plan to extend this collaboration this year, with delivery currently targeted around Q3. We are also actively exploring additional IP partnerships.

In addition, this is a major football year with the FIFA World Cup. We see significant overlap between the global football community and our global gamer base, and we plan to launch a series of football-related promotions during the tournament period.”

5. Concluding Thoughts

This was far from a perfect quarter from Sea. As I write, the stock is down 23%.

My belief is that the guidance for Shopee Adj. EBITDA being flat for the year is the main culprit. That would imply Shopee Adj. EBITDA margin falling from 0.7% in FY2025 to 0.55% in FY2026. The market clearly doesn’t like it.

But I think this misreads what management is actually doing. At 1.75% penetration and already contributing over 15% of GMV in some markets, Shopee VIP is the priority. Investing in the infrastructure and incentives to make that program work costs money in the short term. Sacrificing profitability in the short-term is a clear choice to build the sticky, recurring revenue base that makes the long-term margin target more durable.

The harder question is whether this is an offensive investment or a defensive one. Shopee is aggressively building out logistics and VIP at the same time TikTok Shop is scaling across the region. If the answer is "both," that's not necessarily a bad thing as the best moats are often built during periods of competitive pressure. It is a fair debate, and one worth monitoring over the next few quarters.

One thing that I guess some investors may be spooked about was the optics of the margin trajectory. Going from Adj. EBITDA margins of 0.2% in FY2024 to 0.7% in FY2025 was the narrative that brought many investors back to the stock. Guiding that back down to 0.55% disrupts that story, even if the underlying business is in better shape than ever. Management arguably could have communicated this better.

Personally, I’ve long said that I intend to hold Sea Limited for a decade. The path to 2-3% EBITDA margins, which I actually think is conservative, was never going to be linear. There will be quarters like this one, where the market punishes short-term optics while the business continues compounding in the background.

The top-line growth in Shopee of 25% is very pleasing to hear (ahead of 19% consensus), and shows a clear push toward growth over profitability for the year ahead. As management reiterated during the call, they have levers to pull on either side, and they can ultimately decide which to prioritise. The fact they are prioritising growth despite knowing the market will not like it in the short-term, reinforces my conviction that this is a long-term minded management team.

The main concern over the next year is that the stock lacks a clean catalyst to move higher while the margin overhang persists. In short, I believe this is a fantastic buying opportunity for the long-term investor.

Paid Subscription Upgrade

If you’d like to support the work I do, consider becoming a paid subscriber. Your support will allow me to spend more time finding asymmetric opportunities in the market, writing and analysing various businesses.

As a reminder, paid subscribers get access to:

Monthly Portfolio Updates (+98% in 2024, +26% in 2025)

Earnings Reviews on Portfolio Companies (SE, GRAB, DLO, MELI etc)

Archive of Deep Dives and Posts (13 Deep Dives and counting)

Southeast Asian coverage of industries and companies

With margins this thin, even a small change can have an outsized impact.

Either way, I think it was an overreaction.

Hi GabGrowth,a nice view on Sea Limited Q4,we are also writing a research article on it. Would u mind we recommend each other?Thank you.