dLocal Q4 2025 Earnings Review

Exponential Growth, But Margins Are Collapsing... Here Is Why I Believe The Market Is Completely Missing The Point

dLocal reported Q4 2025 earnings after the market close on 19th March 2026.

2026-03-18 | Seeking Alpha")

Revenue: $337.9M v $296.1M est. (+65% YoY, +69% FX-Neutral) 🟢

Adj. EBITDA: $78.4M v $76.9M est. (+38% YoY, +9% QoQ) 🟢

GAAP EPS: $0.18 v $0.18 est. (+87% YoY, +7% QoQ) 🟢

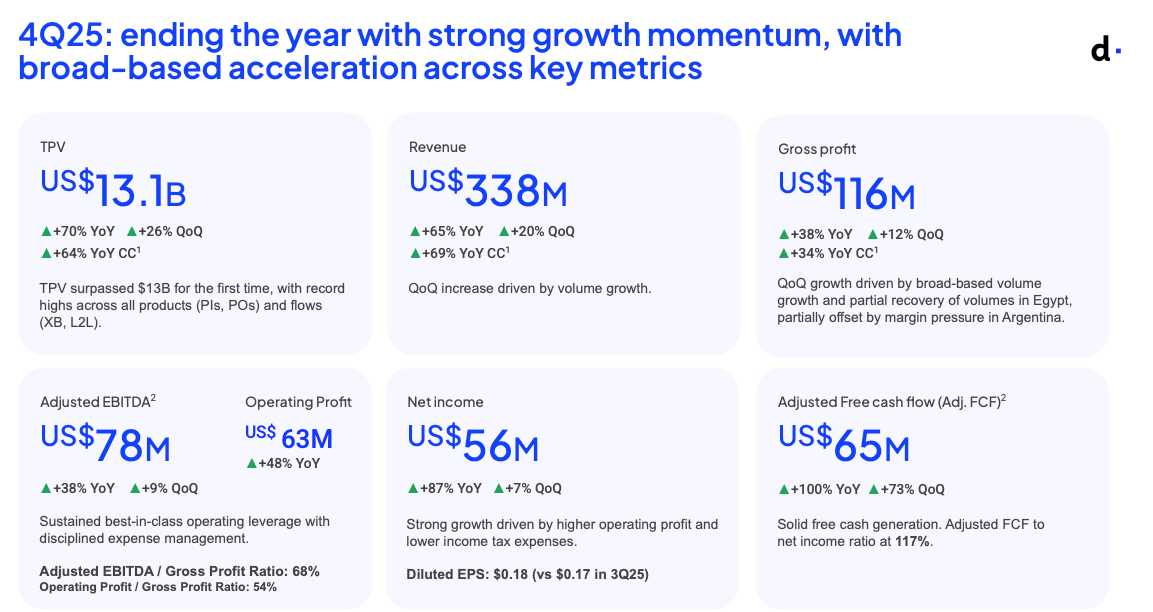

Selected Key Metrics

Again, dLocal saw YoY and QoQ growth across all 6 key metrics. Management also added a new metric that they will be disclosing (operating profit). On that basis, operating profit grew by 48% YoY.

TPV: $13.1B (+70% YoY) ✅

Revenue: $338M (+65% YoY) ✅

Gross Profit: $116M (+38% YoY) ✅

Adj. EBITDA: $78M (+38% YoY) ✅

Net Income: $56M (+87% YoY) ✅

Adj. FCF: $65M (+100% YoY) ✅

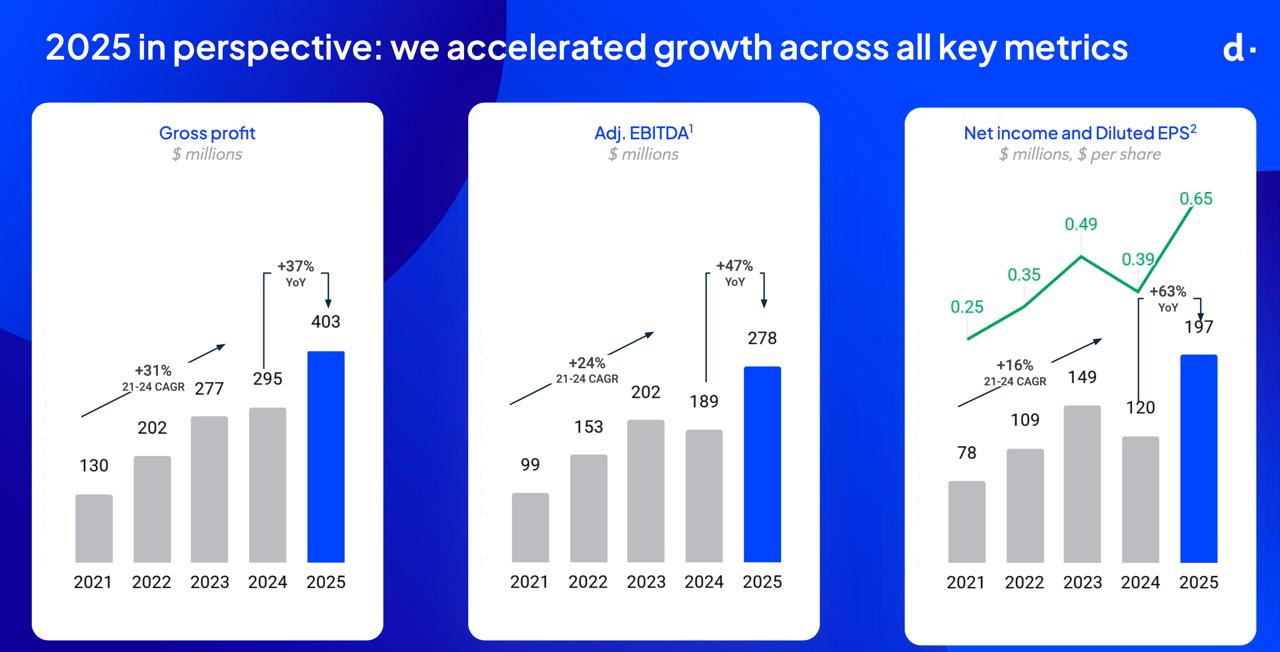

2025 as a whole

dLocal accelerated growth across its key metrics, and have grown operationally too. They now hold 37 licenses across 6 markets, adding 4 in 2025, with a further 16 applications in process.

APMs continue to grow and now represent the majority of EM e-commerce volumes. dLocal also now offers a full suite of stablecoin solutions to merchants, while it is collaborating with all the major agentic payment protocol builders to ensure its merchants are able to process agentic payment mandates.

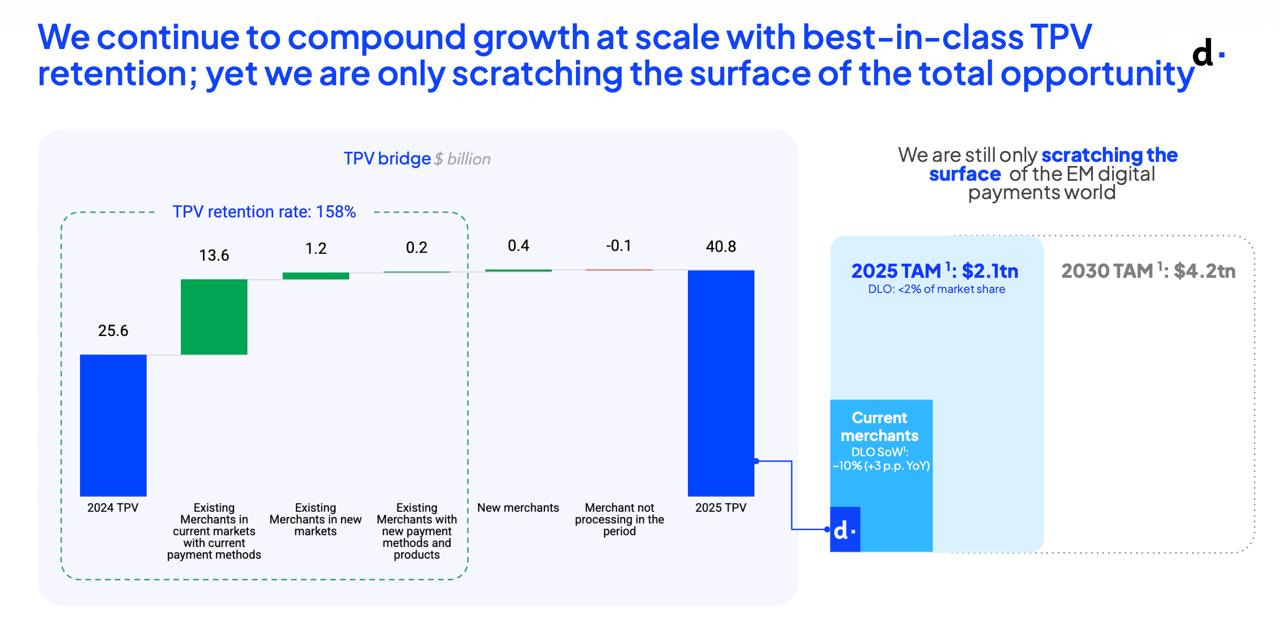

dLocal has a TPV retention rate of 158% with existing merchants clearly seeing the value in the business. However, it is notable that new merchants accounted for a negligible amount of TPV. It appears that dLocal has largely acquired all the merchants it possibly can.

Still, management has called out that it is still only at <2% of its TAM and ~10% of its current merchants. It also expects this TAM to double in 5 years.

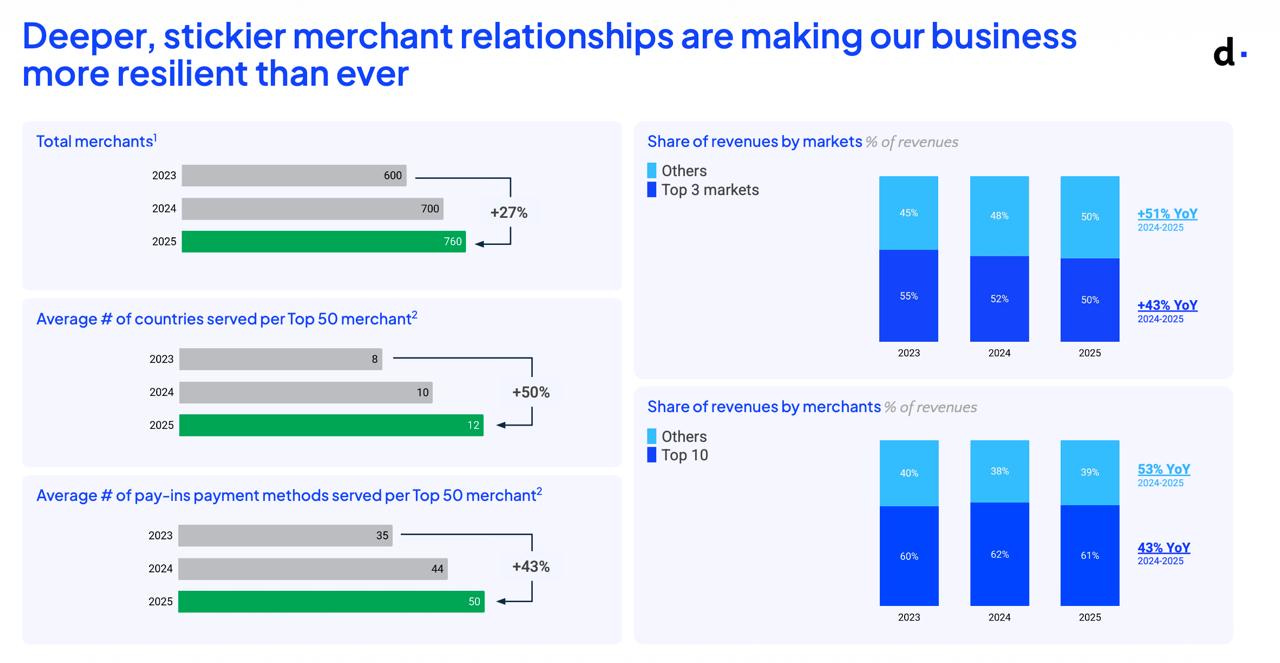

Market and merchant concentration has also fallen slightly year over year, although the numbers remain elevated. Ultimately, this is likely to continue being a concern as large merchants are likely to grow faster than smaller ones.

Table of Contents

Introduction

Financials

Guidance

Product Development

Management Commentary

Concluding Thoughts

1. Introduction

dLocal is a Latin American-based company that facilitates payment flows for businesses ranging from small startups to large conglomerates on a B2B basis, specifically targeting underserved emerging markets.

It thrives in complex payment environments, which are currently a huge tailwind for the business. Effectively, dLocal is a capital-light “toll bridge” business.

dLocal was first pitched to subscribers in July 2025 at $10.98. It has seen volatile stock price performance since but remains a positive returner at this stage.

2. Financials

There are 2 primary metrics to track for dLocal.

The first is total payment volume (TPV). This tracks the total monetary value of all transactions processed through a company’s platform.

The second is take rates. This determines the amount of revenue generated from TPV, which ultimately affects profitability of the business.

Summing it up, we get gross profit, which I perceive as the true top-line of the business. TPV and take rates viewed in isolation are pretty much useless.

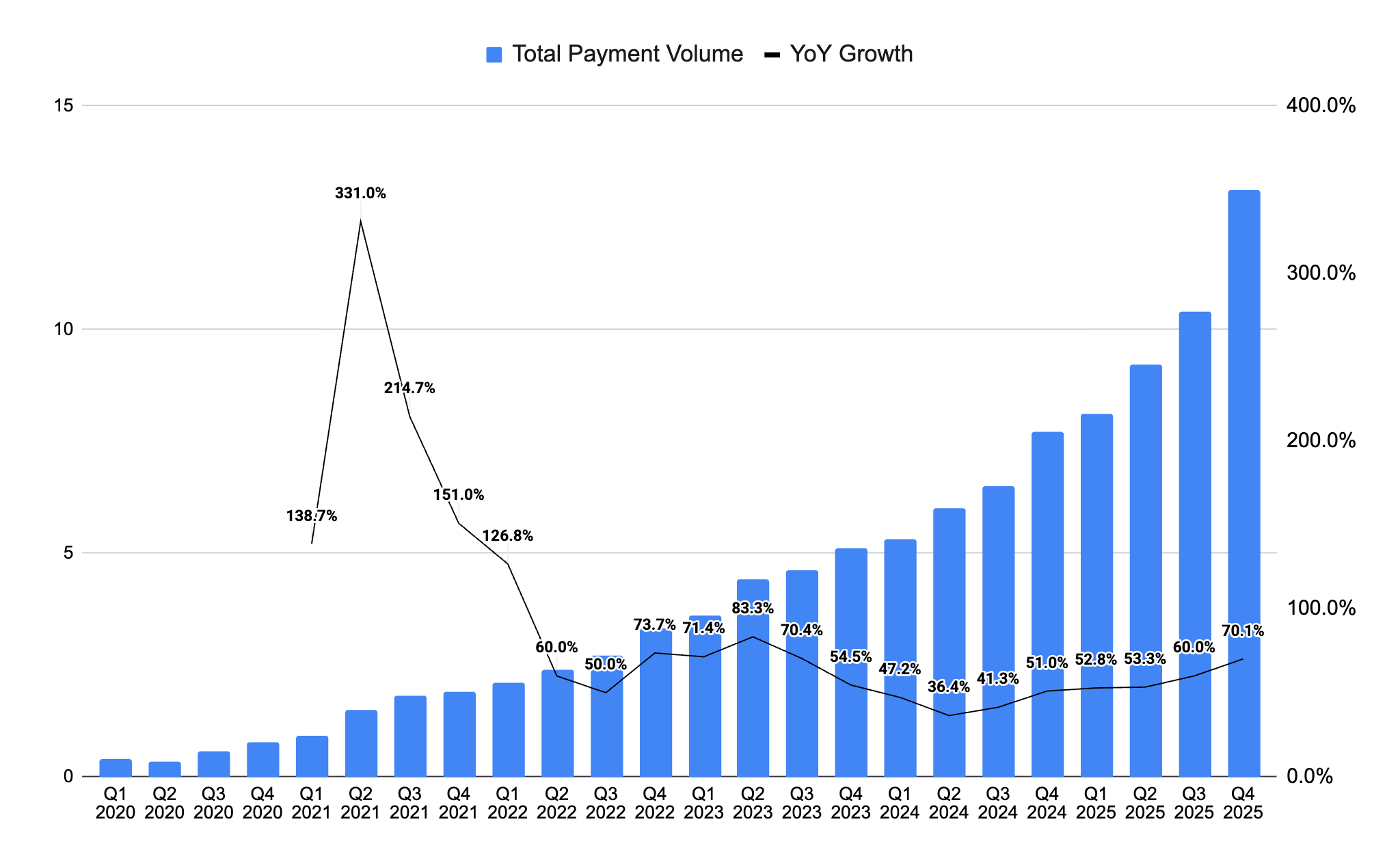

Total Payment Volume

TPV was up 70% YoY and 26% QoQ.

This marked the 6th successive quarter of acceleration in TPV. At the current scale of $13.1B in TPV, this is not an easy feat. IMO, this is very very impressive and shows the clear inflection since Pedro joined.

In Q4 2025 alone, TPV on a QoQ basis grew by more than the prior 3 quarters combined.

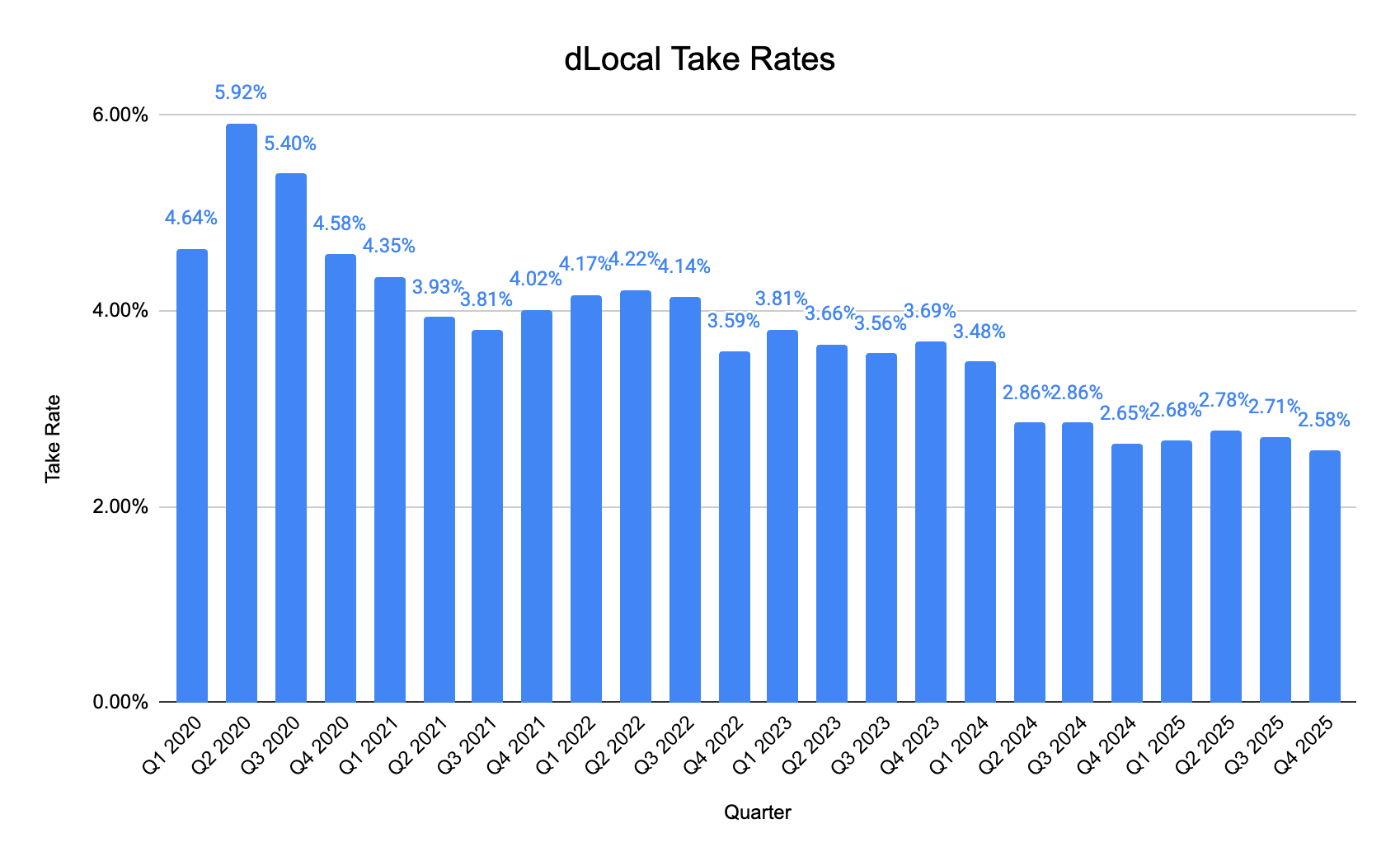

Gross Take Rates (Revenue/TPV)

Gross take rates for the quarter were 2.58%, a 13bp decrease QoQ and 7bp decrease YoY.

Again, this is part of parcel of running a payments business. As TPV increases and customer relationships deepen, factors such as custom pricing negotiations, increased competition, shift in payment mix, and operational efficiencies will affect take rates.

Most importantly, we have to look at the net effect of rising TPV and decreasing take rates.

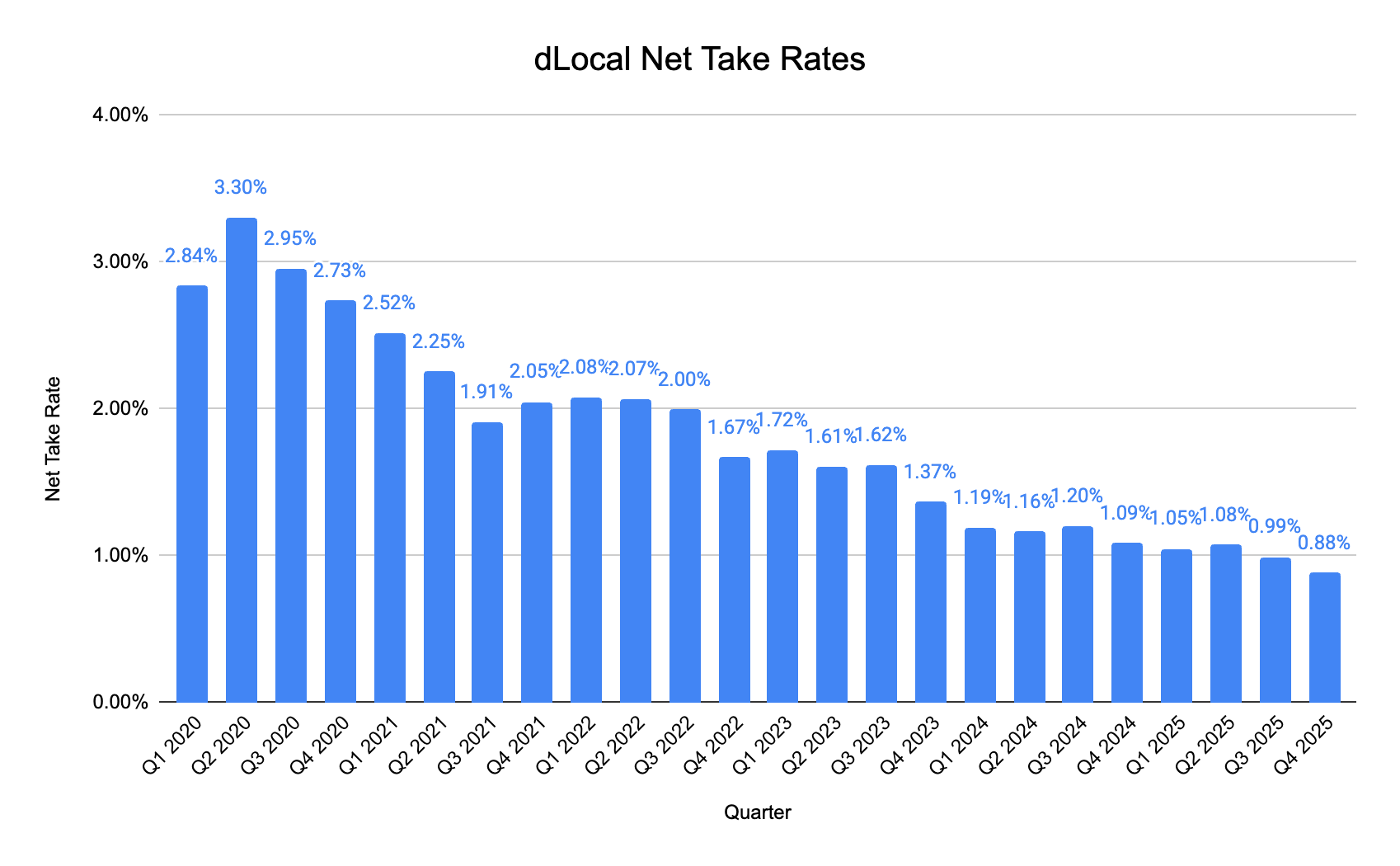

Net Take Rates (Gross Profit/TPV)

Net take rates are arguably more important than Gross take rates as they take into account other costs that dLocal has to pay, such as network fees, partner fees and revenue sharing fees.

It details exactly how much dLocal keeps after all these fees.

Net take rates came down yet again this quarter, falling to 0.88%, an all-time low.

Again, this should not be a surprise. It is clear that dLocal is prioritising TPV growth and that will come with margin compression.

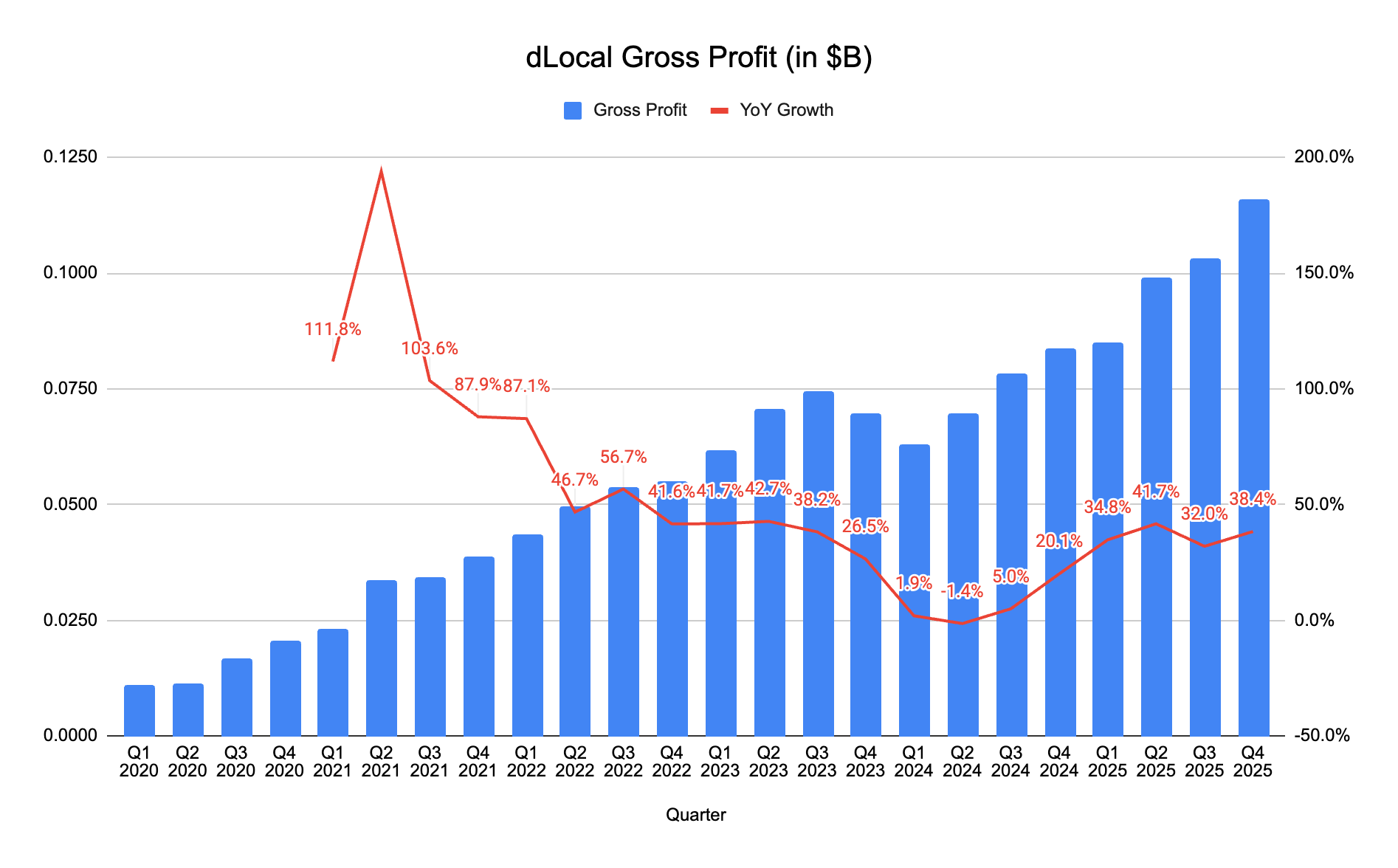

Gross Profit

dLocal’s gross profit continued to grow, up 38.4% YoY, reflecting the increase in TPV, despite the reduction in net take rates.

Ultimately, this will determine dLocal’s long-term profitability and sustainability of its business model. Increasing gross profit dollars is the number 1 priority of the company, and the only way to do so is by increasing TPV or increasing take-rates.

The latter is near impossible, but prioritising TPV will enable higher-margin services in future that could supplement the drop in margins.

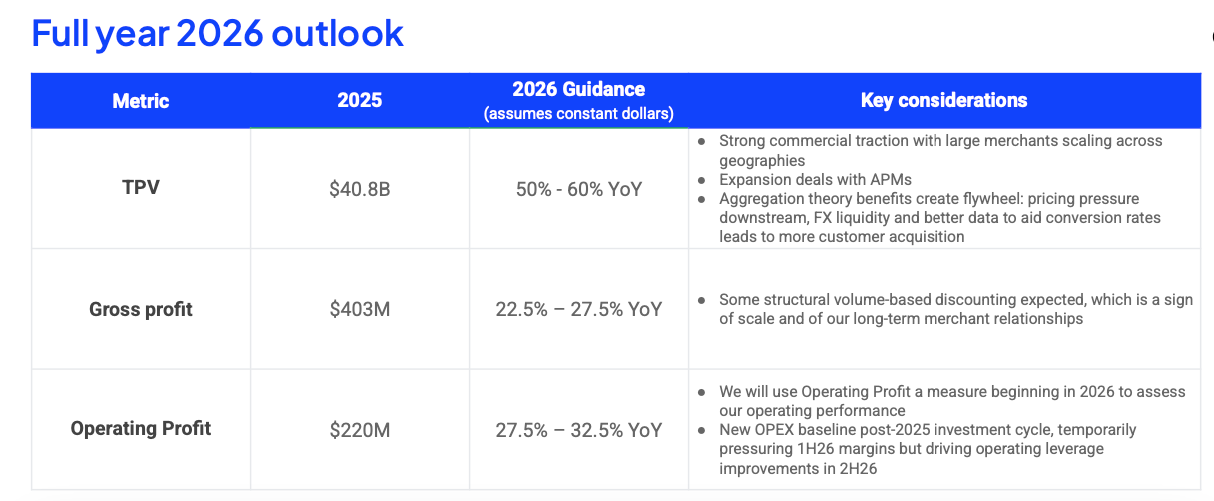

3. Guidance

dLocal has guided for 50-60% YoY growth in TPV for 2026, compared to 59.1% in 2025. Pedro and Co. have sandbagged massively in previous quarters and I expect TPV to come in at the higher range of this guidance.

Gross Profit growth is slightly light, at just 25% at the midpoint. This is compared to 36.7% in 2025. Management noted that this is due to dLocal’s scale and long-term merchant relationships that will inevitably lead to more favourable terms for merchants.

Operating Profit, which is a new metric used by dLocal, is expected to grow 30% at the midpoint.

dLocal also expects new countries to contribute more to the growth of its TPV in % terms in 2026, with significant upside in Africa and Asia.

It also foresees more new merchants in 2026 across high-growth verticals such as Crypto, Travel and Gaming. New products are expected to contribute slightly towards TPV growth, in areas such as BNPL, merchant of record, virtual accounts and card-present.

Buyback and Dividend

dLocal also announced a $300M buyback plan supplementing the previous dividend plan that was shared. Last year, dLocal announced that 30% of the previous year’s Adj. FCF will be returned to shareholders.

The confirmed number is $57M which equates to $0.1939 per share (subject to adjustment according to number of shares outstanding as of record date). This equates to about a 1.6% dividend yield. Furthermore, the $300M buyback will equate to over 8% of shares outstanding.

This is a business that is highly cash generative with massive operating leverage to come.

4. Product Development

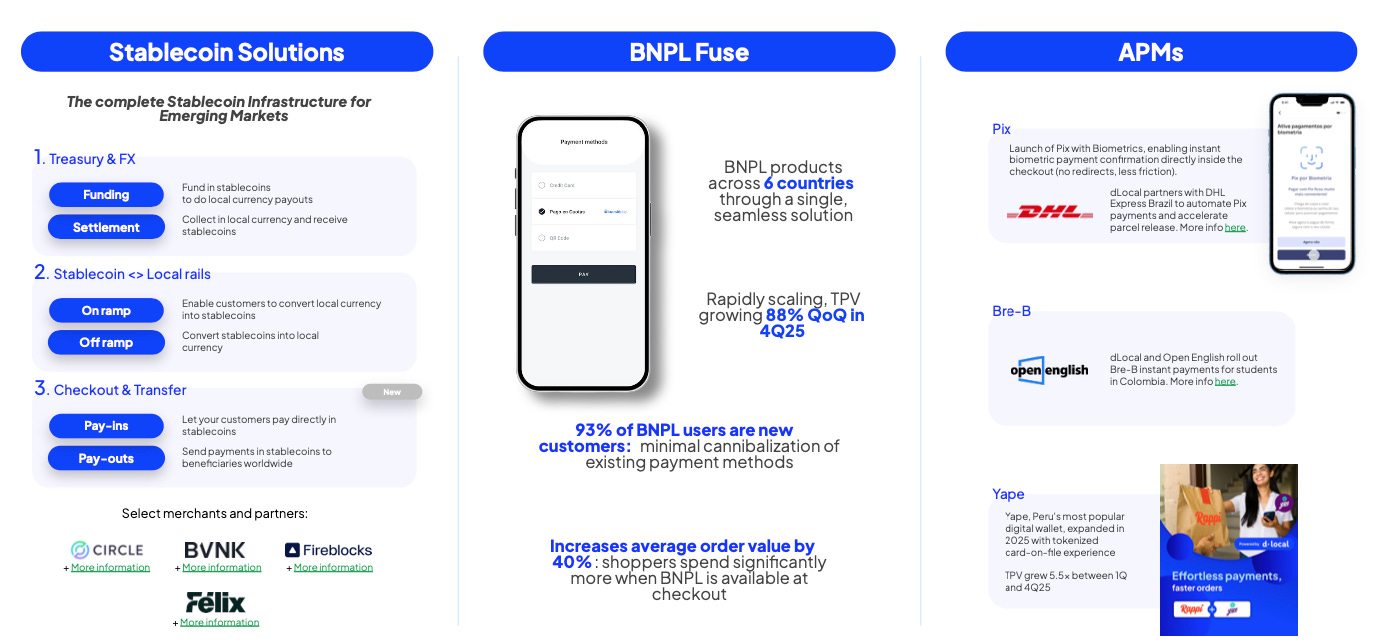

dLocal has prioritised its stablecoin infrastructure in 2025, and has made collaborations with some key players in the market such as Circle, BVNK, Fireblocks and Felix. Stablecoins are clearly a new innovation that will disrupt traditional payments, but dLocal appears well-positioned to participate at the bleeding edge.

It also announced BNPL Fuse which is now operational in 6 countries and scaling rapidly, with dLocal reporting 88% QoQ growth in 4Q25. Importantly, 93% of BNPL users are new customers, which means little to no cannibalisation of existing payment methods.

dLocal has also prioritised APMs through partnerships with DHL Express Brazil to automate Pix payments, Open English in Colombia, and Yape in Peru as some key highlights.

5. Management Commentary

On New Products

“Buy Now Pay Later fused products are now live across 6 countries with solid merchant adoption.

We've completed the launch of our full-service stablecoin suite, enabling merchants to on- and off-ramp fiat to stablecoins, settle and be settled in stablecoins and collect at checkout in stablecoins.

And we continue to add an ever-growing portfolio of APMs, a SmartAPM platform.”

On Stablecoins and AI Agents

“On stablecoins, we've offered a full suite of stablecoin solutions for merchants.

And on AI agents, a possible new frontier for commerce, we are collaborating with Google on the AP2 open standard for interoperable AI engine payments to ensure local payment methods across emerging markets are part of that infrastructure for the ground up.”

On Future Prospects and Take Rates

“Long term, we guarantee that we continue to be one of the scale leaders across emerging markets.

And we feel fairly confident that if you have the merchant relationship and you're processing for them, we will figure out ways to monetize those relationships and all that TPV.

So focused on TPV growth, focused on gross profit dollar growth and being scale leaders across emerging markets is what's implied in the guidance.”

On Prioritising TPV and Future Profitability

“If we have the TPV, we have the merchant relationships as our product portfolio widens, we have that TPV and those relationships to cross-sell new products and also to figure out different ways that we can help our merchants across the markets where we operate with them. So we continue to see take rate as an output metric.

The metrics we manage to our TPV growth which reflect market share, share of wallet and how our merchants choose.

Remember that TPV for us is revenue for our merchants and then be able to drive gross profit growth operating profit growth and earnings growth as a consequence of that sustained high level of compounding TPV growth.”

On 2026 Guidance

“Following a 2025 investment cycle, which has overhang into early 2026 as salaries and wages spend from '25 hirings gets annualized, we expect operating leverage acceleration to become evident more towards the second half of the year and then flow into the following year.”

6. Conclusion

Overall, I thought this was yet another fantastic quarter. Management has proven its ability to spur TPV growth.

Margins will continue to be an overhang, but I am optimistic that the market will change its mind once it realises that gross profit dollars are the true north star metric for the business.

Currently, dLocal is growing gross profit at 37% while trading at just 5.8x NTM EV/GP and 13.6x NTM P/E.

I believe the stock is very undervalued, and the market continues to underestimate the long-term sustainability of its business model and ability to generate operating leverage.

Several months back, I posted a full valuation model on dLocal, detailing my assumptions and stock price output.

The assumptions that I made for FY2025 have been surpassed:

TPV: $37.08B (est) v $40.8B (actual)

Operating Income: $200M (est) v $220M (actual)

Net Income: $164M (est) v $196M (actual)

At these prices, I foresee lots of upside to come. I’d encourage you to check it out.

To conclude, I have no idea when the market will re-price dLocal, but I do believe patience and a huge margin of safety will be rewarded eventually. dLocal is building a payments behemoth that is spitting out cash hand over fist and is entirely shareholder-friendly.

This is a business that I am happy to back.

Thanks for reading!

- Gab

Paid Subscription Upgrade

If you’d like to support the work I do, consider becoming a paid subscriber. Your support will allow me to spend more time finding asymmetric opportunities in the market, writing and analysing various businesses.

Till the end of March, new paid subscribers will get 25% off the paid plan.

As a reminder, paid subscribers get access to:

Monthly Portfolio Updates (+98% in 2024, +26% in 2025)

Earnings Reviews on Portfolio Companies (SE, GRAB, DLO, MELI etc)

Archive of Deep Dives and Posts (13 Deep Dives and counting)

Southeast Asian coverage of industries and companies

Fiscal AI

Many of the charts and numbers I use are courtesy of Fiscal AI, which is in my view, the best platform for financial charting and market intelligence.

I have an affiliate link where you get access to a free 2-week pro trial and 15% off the pro plan. If you are interested, consider signing up. This will greatly help the Substack and help me to continue producing content like this. Thank you!