SpaceX (S-1 Deep Dive)

The largest IPO in history. Is it worth buying immediately?

A couple weeks back, I wrote my first IPO deep dive on Cerebras (CBRS). As shared in the article, I believed Cerebras was massively overvalued, and since the IPO, the stock is down over 33%. While the business is truly brilliant, valuation always matters.

Today, we’re diving into the largest IPO in history. On 20 May 2026, Space Exploration Technologies Corp. (or SpaceX for short) filed its S-1 with the SEC, formally kicking off the road to what is expected to be a 12 June 2026 listing on NASDAQ under the ticker $SPCX.

Reuters and WSJ are pegging the targeted valuation at $1.75T to $2T, with an intended raise of approximately $75B.

This is a massive raise, and to put it in context:

It would be ~3x the size of Saudi Aramco’s 2019 IPO, the previous record

SpaceX would instantly be one of the top 8 most valuable companies in the world

The synthetic SPCX-USD contract on Hyperliquid is implying a $2.2T valuation

SpaceX reported $18.7B in revenue in 2025, with the proposed $1.75T valuation implying 94x P/S.

The counter-argument would be that SpaceX is three massive businesses, with huge addressable markets. In this piece, we will work through the growth prospects of each segment, determine what the moats are, whether they are truly differentiated and defendable, and most importantly, determine a fair value for the business.

Table of Contents

Introduction

Company History

Business Model

Value Proposition

Product Offerings

Moats & Differentiation

Market Context & Industry Positioning

Competitive Landscape

Financials

Ownership & Management

Valuation

Bull and Bear Case

Concluding Thoughts (What I am personally doing)

1. Introduction

Most of us know the founding story of SpaceX, about how Elon tried to purchase ICBMs from the Russians. But for the benefit of those who don’t, here’s a very short backstory.

If you tried to ship something into orbit in 2002, you had two real options, pay Boeing or Lockheed in the US, or pay the Russians. The price was about $18,500 per kilogram to LEO (Low Earth Orbit). The industry had not had a serious cost innovation in 30 years, and the rockets were expendable.

Basically after each launch, the rocket would be disposed of. Imagine flying for a holiday and the plane you were travelling in gets disposed of immediately after. That was the launch industry barely 20 years ago.

SpaceX broke that and set off a new space race that we haven’t seen since the Cold War in the 60s. SpaceX’s Falcon 9 in 2010 reduced the cost to orbit by 85%, dropping payload prices to $2,700 per kg. With Falcon Heavy in 2018, it fell by another half to $1,400 per kg. (The numbers above show the latest vintage cost per kg by year, not the first-version cost, and with reuse maturing + economies of scale, costs have come down massively.)

Starship is SpaceX’s latest launch vehicle that is designed to be fully reusable and is described as a super heavy-life launch vehicle. In documents from Voyager, we found that SpaceX charged just $90M for usage of Starship, which can reportedly support a 150-ton payload. At those numbers, it would equate to a cost per kg of $600.

In about 2 decades, SpaceX has reduced the cost to orbit by 97%. Almost every other business SpaceX has built since exists because of this launch cost collapse:

Starlink would have been economically impossible without Falcon 9 reusability. Even today, 73% of SpaceX’s Falcon 9 launches in 2025 were dedicated to deploying its own satellites (165 launches, only 43 for external customers).

Starlink Mobile (direct-to-cell) sits on top of Starlink.

Orbital AI compute, which is the headline ambition in the S-1, is only economically viable if Starship works at scale and reduces launch cost by another 99%.

The lunar economy and Mars are entirely dependent on Starship.

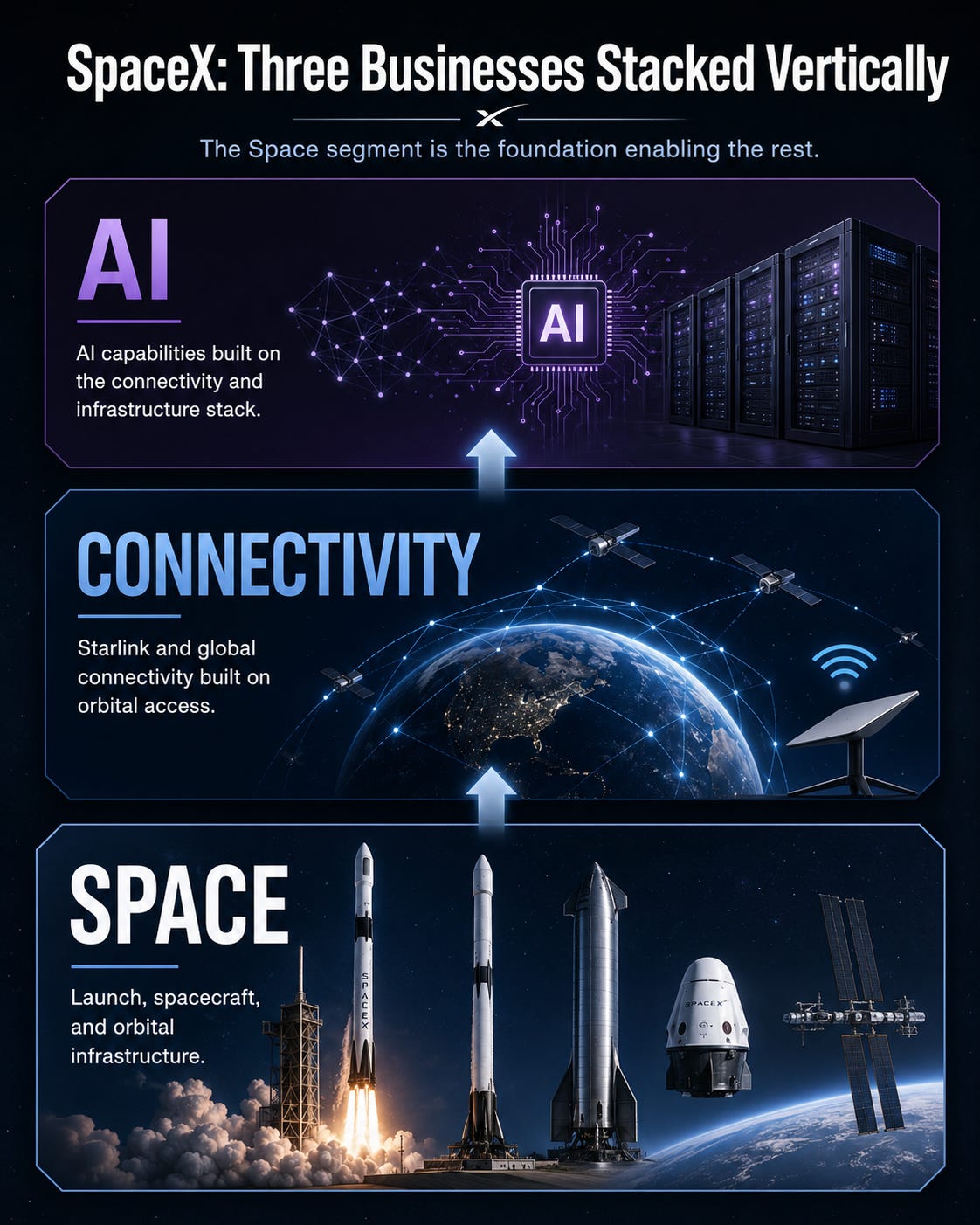

Hence, when we evaluate SpaceX as a business, we are basically evaluating a stack with Starship at the bottom, Starlink in the middle, AI compute at the top with X, Grok, Macrohard, Cursor and Terafab layered on.

2. Company History

SpaceX was founded in March 2002 by Elon Musk, who put in $100M of his PayPal exit proceeds. The original founding team also included Tom Mueller (propulsion), Gwynne Shotwell (who joined in 2002 as VP of Business Development and is now President & COO), and a small group of engineers Musk recruited largely from TRW, Boeing, and JPL.

The early years were brutal, as to be expected for a business attempting to do the impossible. The first launch vehicle, Falcon 1 failed three times between 2006 and 2008, and SpaceX was reportedly weeks from insolvency before the fourth attempt succeeded in September 2008.

The same year, NASA awarded SpaceX a $1.6B Commercial Resupply Services contract, which kept the company alive.

What followed was a 17-year run of step-function milestones.

Timeline Highlights:

2002: SpaceX founded by Elon Musk in El Segundo, California

2006: First Falcon 1 launch (failure)

2008: Falcon 1 reaches orbit (first private liquid-fuel rocket to do so); NASA awards $1.6B CRS contract

2010: Falcon 9 first flight: Dragon becomes first private spacecraft recovered from orbit

2012: Dragon docks with the ISS, first private spacecraft to do so

2015: First successful Falcon 9 booster propulsive landing, “the impossible thing”

2017: First re-flight of a flight-proven Falcon 9 booster

2018: Falcon Heavy maiden flight, putting the Tesla Roadster into solar orbit

2019: First Starlink launch (60 satellites)

2020: Crew Dragon Demo-2: first private company to fly humans to orbit

2023: First Starship integrated flight test; SpaceX launches >80% of global mass-to-orbit

2024: First successful “chopstick” booster catch at Starbase

March 2025: xAI acquires X (formerly Twitter), valuing the combined entity at ~$113B

July 2025: SpaceX invests $2B into xAI as part of a $5B equity round

December 2025: SpaceX completes secondary at ~$800B valuation (per Bloomberg)

Feb 2, 2026: SpaceX acquires xAI in all-stock deal: xAI now SpaceX’s AI segment

March 2026: Terafab announced with Tesla (Intel joins April 2026); SpaceX Bridge Loan of $20B signed with Goldman

April 2026: Cursor compute & option agreement signed (implied $60B equity value)

May 12, 2026: FCC approves $17B EchoStar spectrum acquisition for V2 Mobile

May 2026: Anthropic Cloud Services Agreement signed: $1.25B/month through May 2029 (~$45B total)

May 20, 2026: S-1 filed

The two most important recent events on this timeline are the xAI merger and the Anthropic deal, both of which I will keep coming back to.

3. Business Model

SpaceX now reports three operating segments. The simplest way to think about the business is as three businesses stacked vertically, with the Space segment at the foundation enabling the rest.

Space (22% of 2025 revenue, $4.086B)

This is the legacy launch business, of which the launch vehicles are Falcon 9, Falcon Heavy, and (soon) Starship. Dragon is the reusable capsule that sits on top of a rocket and holds up to 8 people and thousands of kilos of cargo. The Space segment sells launch services to commercial customers, the U.S. government (~20% of total SpaceX revenue), and other governments.

The key thing to understand here is that the Space segment’s reported revenue dramatically understates its strategic value. Of 165 Falcon 9 launches in 2025, only 43 were for external customers.

The other 122 launched Starlink satellites. Those internal launches don’t generate Space segment revenue, as they get capitalised into the Connectivity segment (discussed later). Space, in other words, is partly a captive launch vehicle for Starlink and for orbital AI compute in the future. Reported Space revenue is essentially what is left over after SpaceX feeds itself.

Connectivity (61% of 2025 revenue, $11.387B)

This refers to Starlink, the main revenue and profit driver for the business today. Starlink is a satellite internet constellation that provides global mobile broadband and the nascent Starlink Mobile direct-to-cell business.

As of March 31, 2026, Starlink has the following traction metrics:

~9,600 broadband and mobile satellites in LEO (≈75% of all active maneuverable satellites in orbit globally)

10.3M Starlink Subscribers across 164 countries (up 105% YoY from 5.0M)

7.4M monthly unique devices on Starlink Mobile across 30 countries

Median peak download speed: 225 Mbps; median latency: ~25 ms

For reference, the typical global fixed broadband speed is ~95 Mbps with 30-50 ms latency while US fixed broadband speed is ~290 Mbps with 15-30 ms latency.

However, the target market for Starlink is the rural customer who might be on 25 Mbps in the US, or an Indonesian customer outside Java with no fixed line at all. 225 Mbps / 25 ms is transformational for many.

ARPU: $66/month (down from $86/month a year earlier as the subscriber mix shifts to lower-priced international tiers and lower-ARPU developing markets)

~60%+ of Connectivity revenue is from consumer subscribers, the rest from enterprise and government. It is key to note that ARPU is declining quite fast, although margins continue to expand because of network density (no marginal cost to serve).

AI (17% of 2025 revenue, $3.201B)

This segment was bolted on in February 2026 via the xAI merger and includes:

Compute infrastructure: COLOSSUS + COLOSSUS II, ~1 GW of nameplate compute in Memphis, TN

Grok: xAI’s frontier model (Grok-4 currently deployed, Grok-5 in training)

X: Social platform with ~550M MAUs and 350M daily posts

Recent additions: Cursor (via option), Macrohard (co-owned with Tesla), the future Money Product

The key here is probably the Anthropic deal that was announced just a couple weeks ago. Anthropic has been extremely low on compute for several months and have therefore enforced sudden throttling and dynamic 5-hour session limits during peak hours. As such, Anthropic signed a $1.25B per month (once fully ramped) deal through May 2029 with xAI for access to COLOSSUS I. This equates to $15B yearly, which is 80% of SpaceX’s 2025 revenues. It is a massive deal.

That said, there is certainly room for concern. The deal states that either party can cancel the deal with 90-days notice. With the massive ramp up in compute, it is a possibility that Anthropic finds other available compute and decides to cancel the contract prematurely, especially as it would prefer to avoid funding a direct competitor.

This translates to 300+ MW of compute capacity with 220,000+ NVIDIA GPUs that will ramp to full utilisation within this month. At these prices, Anthropic is paying about $50M per MW per year, which stacks against Neoclouds that are charging ~$10-12M per MW per year, a whopping 4x premium.

Basically, Anthropic is paying a major scarcity premium for immediate, large-scale, contiguous AI compute. This may seem irrational, but due to the demand for compute being excessive at the moment, they seemingly have no other option.

This does, however, say something about Grok. Clearly, the demand for compute at Grok has been lackluster hence them being willing to rent out the whole Colossus I cluster to Anthropic.

4. Value Proposition

SpaceX’s pitch is fundamentally about owning the physical stack of the future: launch, satellites, energy, chips, compute, models, and applications, all under one roof.

Firstly, space is the next frontier not just for exploration but also for infrastructure. With Falcon 9 reusability already in production and Starship targeting another 99% cost reduction, things that were uneconomical 5 years ago are becoming economical. The most obvious example is global broadband from LEO. The next examples are direct-to-cell and orbital AI data centers.

Secondly, AI is becoming compute-bound and energy-bound. Reasoning models can be 10-100x more compute-intensive per query than chat. Inference is growing 2x+ faster than training. Meanwhile, US electricity generation has grown at less than 3% annually since 2023 while AI data center demand has roughly tripled. The Sun produces 99.8% of the solar system’s energy and if compute can be put in Sun-synchronous orbit, you will be able to bypass the terrestrial grid bottleneck entirely. Of course, making this happen is a multi-year or even multi-decade challenge.

Thirdly, SpaceX is uniquely positioned to capture this. They already build, launch, and operate the world’s largest satellite constellation, and also operate the largest coherent AI training cluster on Earth. They are building a chip fab (Terafab) with Tesla and Intel, while owning one of the four frontier models (Grok), and a major distribution channel (X). Recently, their purchase of Cursor, which is the most engaged developer workflow also fits seamlessly in this.

5. Product Offerings

A. Launch Vehicles

Falcon 9 (Fully Operational)

This is the workhorse. Two-stage system with a reusable first stage.

23 metric tons to LEO when fully expendable, ~17.5 tons reusable.

~620 launches as of March 31, 2026 with >99% mission success.

Boosters now demonstrated to re-fly 34 times.

Falcon Heavy (Fully Operational)

Partially reusable super heavy-lift.

64 metric tons to LEO. 11 launches with 100% success rate.

Used for the most demanding missions (NSSL heavy, Europa Clipper, Psyche).

Starship (Active Testing & Development Phase)

Fully reusable super heavy-lift.

Designed for 100+ metric tons to LEO in reusable mode (vs. ~150 tons fully expendable).

33 Raptor engines on the Super Heavy booster + 6 Raptors on the upper stage.

This is the biggest and most important bet. Starship is in active testing and has done 12 test flights so far. The most recent was just last week, the first of its V3 iteration that was launched from Starbase.

It deployed a clutch of mock satellites and executed a controlled splashdown of the spacecraft in the Indian Ocean. But it failed to achieve a controlled landing of the Super Heavy booster, which tumbled into the Gulf of Mexico.

If Starship works as intended (full reusability + airline-like turnaround), SpaceX will be targeting multiple launches per day per pad. Currently, Starship is the largest and most powerful of the heavy-lift rockets, easily towering over competitors.

B. Spacecraft

Dragon

Sends crew and cargo to LEO and the ISS.

78 crew members from 20 countries flown since 2020.

V1 Mobile

Direct-to-cell satellites (~650 in orbit).

Provides SMS, light data, and OTT voice today.

V2 Mini

Current broadband satellites.

V3

Next-gen broadband, 1 Tbps downlink per satellite, 60 deployable per Starship launch (vs. ~22 V2 Minis per Falcon 9).

Expected to be deployed in H2 2026.

V2 Mobile

Next-gen direct-to-cell with full 5G NR-NTN compliance.

Targeting 2027 deployment on Starship.

Requires the EchoStar spectrum to close (Nov 2027 expected) and handset manufacturer adoption of new RF front-ends.

C. AI Compute

COLOSSUS I

130 MW initial cluster brought online in 122 days, ~100,000 H100s. Currently, Colossus I has over 300 MW of capacity, with 220,000 NVIDIA GPUs, consisting of a mix of H100, H200 and GB200 accelerators.

This is currently rented out to Anthropic for $1.25B per month.

COLOSSUS II

Memphis + Southaven, MS. Combined ~870 MW. Initial 110,000 GB200 cluster brought online in 91 days with a follow-on 110,000 GB300 cluster in 64 days.

Future expansion: +220,000 GB300s and +400 MW. This is currently training Grok-5.

Combined: ~1 GW of coherent compute today, with line of sight to multi-GW.

Terafab

Chip manufacturing JV with Tesla and Intel.

xAI is targeting 1 terawatt of compute hardware per year.

This however, is extremely aspirational and is a far stretch today.

D. Software & Models

Grok

Grok-1 was launched in Nov 2023 with Grok-4 currently in production. xAI is training Grok-5 using Colossus II.

While Grok is a capable model, it is still behind the leading frontier labs: OpenAI and Anthropic.

SuperGrok, SuperGrok Heavy, SuperGrok Lite: Consumer Subscriptions

Grok Business, Grok Enterprise, xAI Gov: B2B Subscriptions

Grok API: Developer Access

Imagine: Image/Video Generation

Grok Voice: Real-time speech.

Macrohard: Early-stage AI workflow platform being co-developed with Tesla.

E. Future / Speculative

As with every Elon company, there is a long list of potential businesses in play. These are some that have been listed in the S-1.

Orbital AI compute (target deployment from 2028)

Lunar mass driver (electromagnetic launch from the Moon)

Money Product on X (payments + banking)

Asteroid mining, in-space manufacturing, lunar/Mars passenger transport