Southeast Asia's Race for the Unbanked

From Monee's $9B loan book to Grab's 50M monthly transacting users and what it means for investors.

There is a new financial system being built from scratch across Southeast Asia, one that is vastly different to the traditional system we see in New York and London.

These are not banks, nor PayPal clones, and definitely not crypto projects.

Instead, they are ecosystems that began as ride-hailing apps or e-commerce platforms with the ultimate goal of becoming the primary financial institution for hundreds of millions of people who have never had a bank account to start with.

The scale of the opportunity is massive. More than 70% of Southeast Asia’s adult population remains either unbanked or underbanked, lacking access to credit, insurance, investments and even basic savings products.

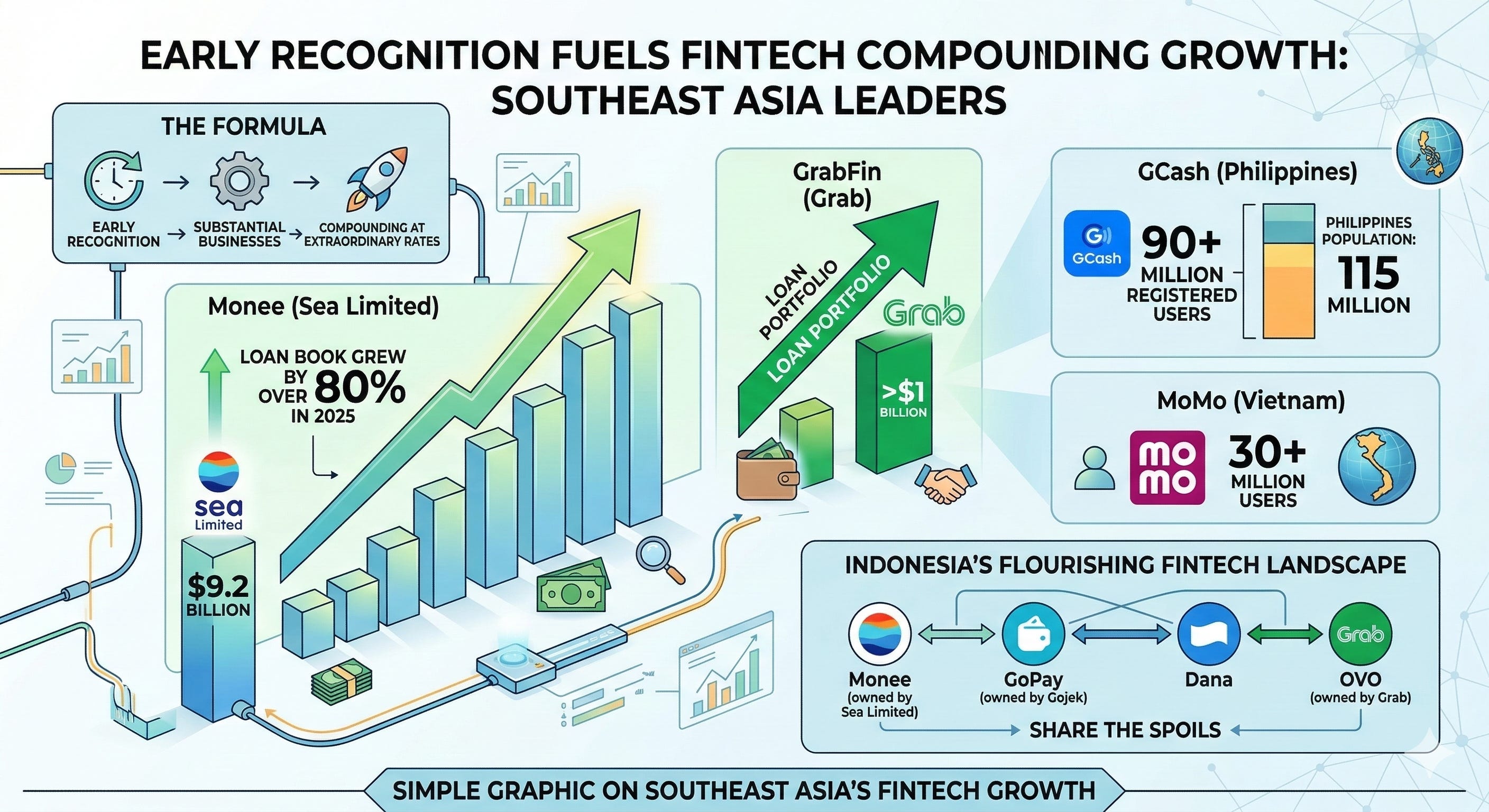

The companies who recognised this earliest have now built substantial businesses off the back of this, compounding at extraordinary rates.

Monee, Sea Limited’s FinTech arm, grew its loan book by over 80% in 2025 to reach $9.2 billion. GrabFin, Grab’s FinTech arm ended the year with a loan portfolio larger than $1 billion. GCash has over 90 million registered users in the Philippines, a country of 115 million people. MoMo in Vietnam has over 40 million users while Indonesia has a flourishing FinTech landscape with Monee (owned by Sea Limited), GoPay (owned by Gojek), Dana and OVO (owned by Grab) sharing the spoils.

In this piece, we will discuss the Southeast Asian FinTech landscape. Specifically:

Who the players are

How they differ structurally

Where the competitive edge is being built

We will then move from the macro context down to individual company profiles, and close with a framework for thinking about this space as an investor.

Why This Market Is Different

Most Western fintech narratives are about convenience. The winners are typically players that make it slightly easier to move money that people already have access to.

However, in Southeast Asia, it’s a different story. It is more about access than convenience. For a delivery driver in Jakarta or a market vendor in Ho Chi Minh, a digital wallet is not just a better version of what they already have, but rather the only formal financial product they have ever used, or have access to.

To make this clear, here’s an example. In the West, companies like PayPal, Block or Apple have succeeded by making it slightly easier or cheaper to move money that people already had sitting inside the banking system.

In Southeast Asia, most consumers did not have bank accounts, credit histories, or even reliable ways to store money digitally.

That is why companies like Sea Limited, Grab and GCash did not start by competing with banks. They started by solving everyday problems such as ride-hailing, food delivery or e-commerce. Only after they had millions of users transacting on their platforms did they begin layering financial services on top.

Why does this distinction matter so much?

When a company acquires a customer in an underserved market, the switching costs are high because there is no alternative. There is often no incumbent to displace (the incumbent is cash).

Because these platforms often provide the first credit record a user has ever generated, the data moat compounds with every transaction. Every loan taken and repaid, wallet top-up, and transaction taken slowly builds a credit profile that traditional banks have no access to and competitors find difficult to replicate.

The regulatory environment has been much more constructive than many probably expect. While Southeast Asia is much less developed than most countries globally, many of the governments (Indonesia, the Philippines, Singapore, Vietnam, Malaysia) have all introduced digital banking license frameworks in recent years that give ecosystem players like Grab and Sea a regulated pathway into deposits and lending without having to acquire legacy banks.

This has allowed SuperApps like Grab and Sea to formalise their financial operations, fund their loan books at lower cost, and access interbank liquidity, dramatically improving the unit economics of lending over time.

The Players

There are several players in this space, some of which operate in individual countries while others dominate across the region’s key markets. Each of these companies have a different anchor product, value proposition and competitive moat. In this section, I intend to breakdown the differences between each of them.

Monee (Singapore, Malaysia, Indonesia, Philippines, Thailand, Vietnam, Taiwan, Brazil)

We have to start with Monee. It is by almost any measure, the most advanced digital financial services operation in the region. Monee began as AirPay, a simple top-up feature for Garena and subsequently ShopeePay, a wallet bolted onto Shopee’s e-commerce platform. However, it has since evolved into a full-fledged consumer and SME credit business, which is now Sea’s fastest-growing division and perhaps the most strategically important one.

Sea runs 3 main divisions. The largest, Shopee is the leading e-commerce business in the region with over 400 million active buyers. The most profitable division is Garena, their gaming unit that is responsible for the most played mobile game in the world, Free Fire. Monee is the newest segment and the fastest growing.

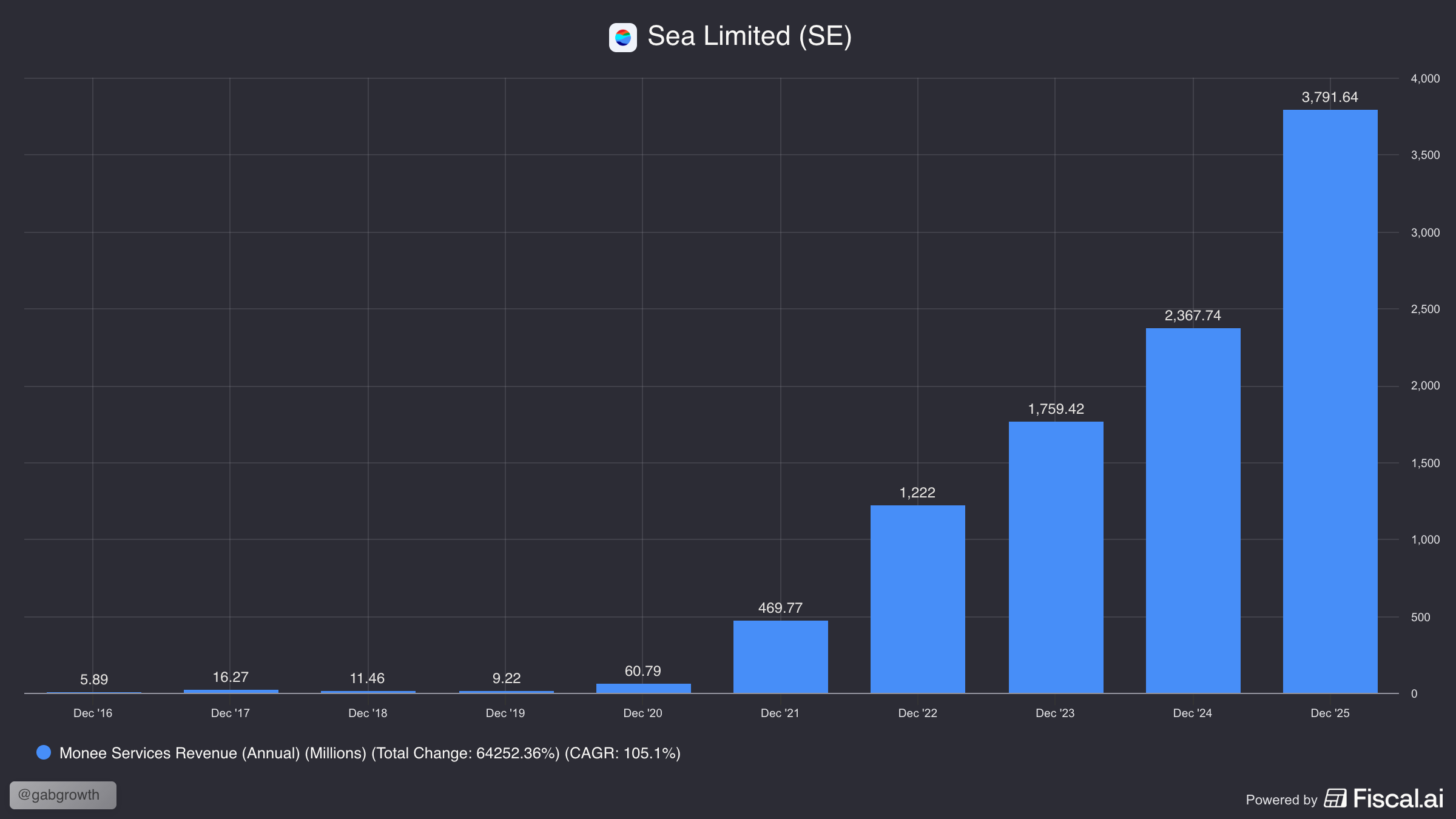

Since 2016, Monee has grown its revenues at a 105% CAGR, roughly doubling each year. Last year, it brought in $3.8B in revenues, with a 25.6% operating margin on a segment basis. This meant it accounted for nearly half of Sea’s entire EBIT for 2025.

At the end of 2025, Sea disclosed that it had over 37 million credit users on its platform. Importantly, despite the massive user base, there is still much room for growth. Shopee has 400 million active buyers and 20 million sellers that generate a continuous stream of target users for the business.

Apart from this, this massive user base also generates a constant stream of behavioural data that is likely to be immensely useful for Monee. For instance, purchase frequency, basket size, repayment history on Shopee PayLater, merchant cash flow patterns, which Monee can use to underwrite credit at a scale and accuracy that no traditional lender can match.

Sea now has a loan book in excess of $9.2 billion, while growing at 80% YoY. Despite the high growth rates, Sea maintains a very healthy 90-day non-performing loan (NPL) ratio of just 1.1%. This is a signal that the credit model is working even as the platform pushes into broader applicant pools and non-Shopee channels. It also has a deposit base of $3.8B, up 40% YoY from the previous year’s $2.7B.

A notable strategic shift in 2025 was the move from an invite-only lending model to an "all can apply" approach. Management opened the doors to everyone, and default rates did not move. They attribute this to Shopee's transaction data feeding AI underwriting models that process purchase patterns, return behaviour, payment timing, and browsing history through transformer-based models trained on long-sequence behavioural data.

This represents a 46% deposit-to-loan ratio which means nearly half of the on-book loan portfolio is being funded by deposits that probably cost Monee somewhere in the 1-3% range. The other 54% is funded out of Sea’s $11B cash pile or other sources, capital that could otherwise be earning a return elsewhere.

Management also noted on the most recent Q4 2025 earnings call that AI-assisted underwriting is enabling expansion to borrower profiles that were previously considered too risky.

Of note, in terms of risk, is that the $9.2B is largely on-book loans, which means a relatively capital-intensive structure. Just $1B of that $9.2B reflects a capital-light structure where Monee originates and services loans while offloading credit risk to third-party investors.

The off-Shopee expansion is worth watching closely. Off-Shopee SPayLater loans surged over 300% year-on-year in Q4 2025 and now make up more than 15% of the portfolio, with roughly 30% usage penetration in Malaysia. This is the key metric for whether Monee eventually gets valued as an independent fintech or remains tethered to Shopee's GMV growth rate. The BCL (Buy-Consume-Later) product for offline retail and direct consumer financial products are the vectors for this expansion.

One area that deserves attention is credit loss provisions, which surged 76.7% to $1.4 billion in FY2025. This outpaced even the 80% loan book growth, which is why Adjusted EBITDA grew only 40% on 60% revenue growth. The NPL ratio is stable, but the provision amount has gone up massively. This has not been stress-tested by a severe regional macroeconomic downturn or rapid FX deterioration. The loan book is largely unsecured consumer credit across emerging markets (Southeast Asia and Brazil), and it is approaching $10 billion in scale. As long as the NPL ratio holds, the provision build is just the cost of growth. If it does not hold, the capital intensity of the on-book model could become a vulnerability.

Long-term, the ideal scenario would be for Monee to become a marketplace for credit, growing the off-book ratio (currently just $1.0 billion of the $9.2 billion total) and enabling it to improve return on equity as the book scales. Management has guided for Shopee GMV growth of 25% in 2026, with Adj EBITDA no lower than 2025 in absolute terms. This implies Shopee margin compression as subsidies ramp, but Monee's continued scaling should partially offset that at the group level.

GrabFin (Singapore, Malaysia, Indonesia, Philippines, Thailand, Vietnam)

The second largest player that also operates on a regional basis is GrabFin, a subsidiary of Grab. Grab is the leading ride-hailing and deliveries player in the region with over 50 million monthly transacting users on its platform. It commands nearly 60% market share in both categories and is a household name.

Grab's financial services strategy is structurally different from Monee's in that it is deliberately multi-entity. Rather than building everything under a single fintech brand, Grab operates a layered system. GrabFin handles lending to its ecosystem partners (drivers, merchants, users), while GXS Bank (Singapore, with Singtel) and GX Bank (Malaysia) operate as fully licensed digital banks, and Superbank (Indonesia, 37.88% effective equity stake) handles deposits and credit locally.

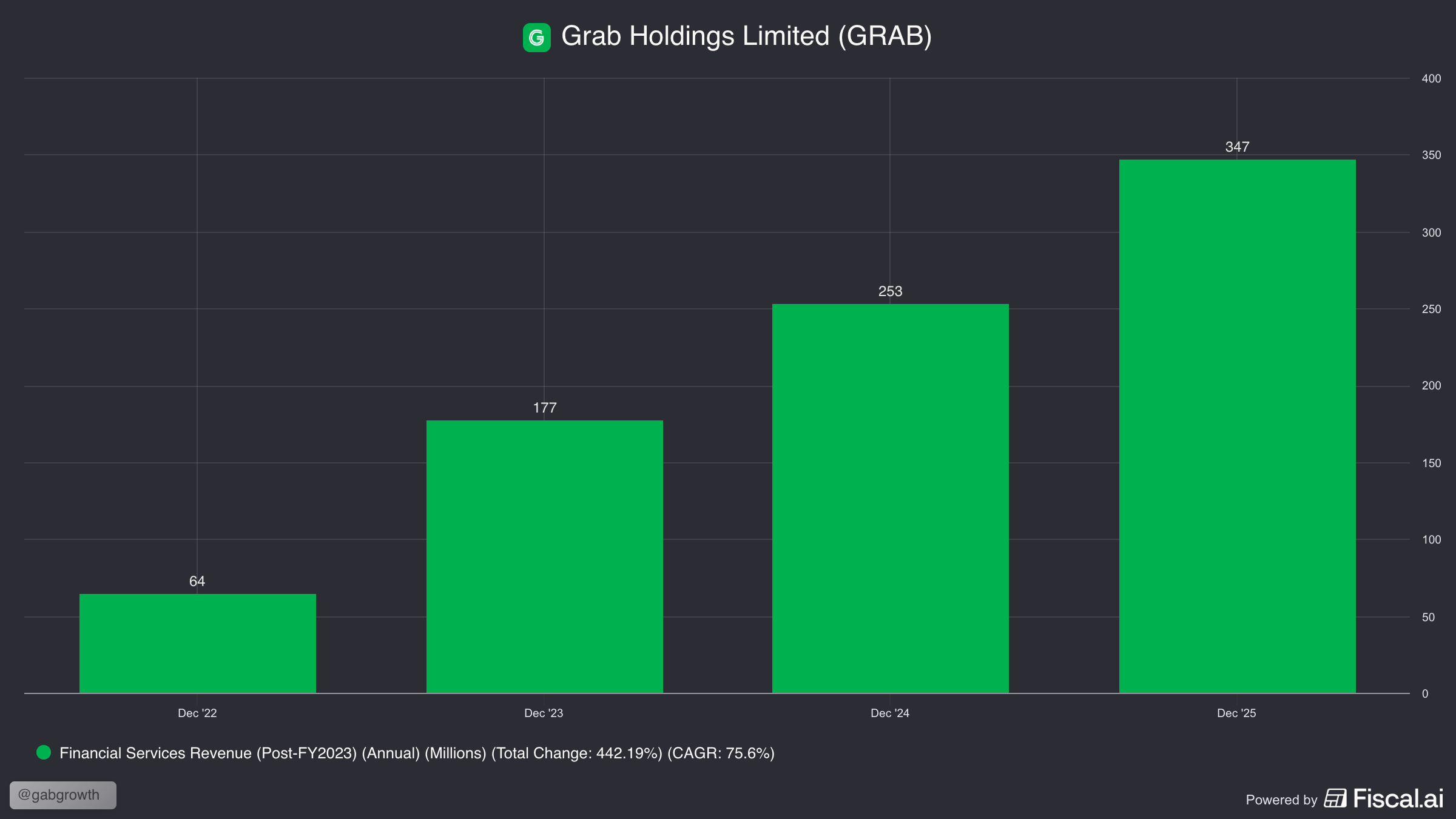

Grab ended 2025 with a gross loan portfolio of $1.3 billion, with a net loan portfolio of $1.18 billion after provisions, up 120% year-on-year. Customer deposits across GXS Bank and GX Bank grew to an all-time high of $1.6 billion at end-Q4, up from $1.2 billion a year earlier. Notably, deposits dipped to $1.31 billion in Q3 2025 from $1.54 billion in Q2 as Grab proactively cut promotional deposit rates to manage funding costs. The Q4 recovery to $1.6 billion on the back of customer growth rather than rate competition is a healthier trajectory.

The deposit base now serves 7.4 million customers across the three banks. Importantly, there is a very clear cross-sell efficiency here. 76% of GXS Singapore depositors, 93% of GX Bank Malaysia depositors, and 60% of Superbank Indonesia depositors were already existing Grab users. This means Grab is converting super-app engagement into banking relationships with minimal incremental customer acquisition cost.

Revenues have grown at a 75.6% CAGR since 2022. However, Grab’s financial services segment remains unprofitable with a FY2025 adjusted EBITDA of -$110M. This is in comparison to Monee’s FY2025 adjusted EBITDA of $1.02B.

There are several reasons for this disparity.

Firstly, Monee had a five-year head start. Sea started building AirPay in 2014 for Garena top-ups. By 2019, they rebranded to ShopeePay and began embedding credit directly into checkout flows. By the time Grab got its Singapore banking license in 2022, Monee already had a multi-billion dollar loan book across seven markets.

Secondly, Monee is not just a bank that happens to be connected to an app. It has designed itself to be a financial layer embedded inside Shopee where credit exists to drive more Shopee transactions. SPayLater increases the basket size and purchase frequency, and seller loans keep inventory flowing. Therefore, every Shopee user (buyer and seller) is a potential Monee customer without any incremental customer acquisition cost.

GXS is structurally a standalone digital bank that happens to be owned by Grab and Singtel. It can be accessed through the Grab app and uses Grab’s data for underwriting. However, the banking product doesn’t exactly drive more rides or food deliveries the way that SPayLater for instance drives more Shopee orders. There is no closed-loop commerce flywheel to drive deposits and loans. Hence, GXS has to compete for deposits against the likes of traditional banks like DBS, UOB and OCBC in Singapore by offering promotional rates which is a traditional banking acquisition strategy, not an ecosystem play like Monee.

Thirdly, Shopee processes 13.9 billion orders a year across 400 million active buyers and 20 million sellers. Each of these transactions generate SKU-level purchasing data, repayment behaviour on SPayLater, seller cash flow patterns etc… that provide granular data that is then used to map to creditworthiness.

Grab also has extremely useful data such as how often rides are taken, food order sizes, discretionary spend, but it is fundamentally consumption data on a much smaller scale. This can be seen in GMV. Shopee generated $127B in GMV compared to Grab’s total on-demand GMV of $22B in 2025. That is nearly 6x difference and explains why the FinTech gap is so wide.

GCash (Philippines)

GCash is the leading digital wallet in the Philippines. It is backed by Globe Telecom and Ant Group (Alibaba’s Financial Arm), and has over 90 million registered users, in a country of 115 million people. They are effectively a national payments infrastructure.

It was first launched in 2004 as a SMS-based money transfer service under Globe Telecom. This was a critical service at the time with ~80% of Filipinos being unbanked. They employed a very simple model where users could convert cash to e-money via sari-sari stores (think small, neighbourhood retail stores) for a transaction fee of about ₱1 (about 1-2 cents in USD).

It expanded into online payments in 2006, relaunched as a fuller mobile wallet in 2009, and partnered with Western Union in 2010 for inbound international remittances (a big deal given the massive Overseas Filipino Worker economy).

The strategic inflection came in 2015 when Mynt was established as a joint venture between Globe, Ayala Corporation, and Ant Financial (now Ant Group). The Ant partnership brought the Alipay playbook to the Philippines. By 2017, GCash launched the country's first mobile money QR payment system, and by 2018 it had surpassed 10 million users. In 2019, GCash evolved from a payments tool into a nascent SuperApp with GSave (savings via CIMB Bank), GCredit (revolving credit), and GInvest (investments).

The COVID pandemic was GCash’s defining moment. Usage surged as millions of Filipinos used GCash to pay for goods and services online and to send/receive money. GCash also partnered with the Philippine government to distribute pandemic financial aid which was massive for user acquisition.

In November 2021, Mynt raised $300M at a $2B valuation, making it the first double unicorn in the Philippines. In August 2024, GCash secured additional funding from Ayala Corporation and MUFG pushing its valuation up to $5B.

Today, 8 in 10 Filipinos use GCash, with 6 million merchants and social sellers accepting payments. In 2025, GCash disbursed ₱323 billion (USD $5.4B) in loans to 10.2 million unique borrowers, a 73% increase year-on-year. GSave serves 15.3 million users, GFunds has 8.6 million, and GCrypto enables 4.4 million to trade digital assets.

GCash is targeting an IPO in the second half of 2026, delayed from an earlier timeline due to the Philippine stock market's weakness and the company is aiming to raise $1 to $1.5 billion, which would make it the largest IPO in Philippine history.

GCash is basically the closest analog to Alipay in Southeast Asia, though it is only present in the Philippines. The real challenge facing GCash now, is whether it can sustain its lending growth and ARPU expansion as it moves from payments (low-margin, high-volume) to financial services (higher-margin, credit risk).

Maya (Philippines)

Maya is perhaps the most under-appreciated player in this landscape. It is backed by PLDT (the Philippines’ largest telco), Tencent, KKR and the IFC (Private arm of World Bank Group). Rather than building financial services on top of an existing SuperApp, Maya obtained a full digital banking license from the central bank of the Philippines in Sept 2021 and converted from a payments wallet (PayMaya) into a regulated digital bank in 2022. It is perhaps the only player in this piece that is a bank first and a platform second.

What makes Maya worth watching closely is the pace of their financial ramp in recent years. Maya Bank launched in 2022 and disbursed just ₱3.1 billion (USD $52M) in loans that year. In 2023, disbursements jumped to ₱21.5 billion (USD $358M). In 2024, ₱68 billion (USD $1.1B). In 2025, approximately ₱164 billion (USD $2.7B), bringing cumulative disbursements since launch to ₱256 billion (USD $4.3B) across 3 million borrowers. That is roughly 141% annual growth in disbursement volume, to a borrower base that grew 95% year-on-year.

The deposit base has tracked a similar trajectory: ₱25 billion (USD $417M) at end-2023, ₱39 billion (USD $650M) at end-2024, and ₱68 billion (USD $1.1B) at end-2025, a 72% increase over the year. The bank doubled its customer base to 10.7 million in 2025. The loan-to-deposit ratio reached 51.1% in Q1 2025, which signals disciplined capital deployment, and the net interest margin widened to 18.9% from 13.9% a year earlier (as of September 2025). That NIM figure is extraordinary by any global standard, and speaks to the spread available in a market where the borrower base has historically had no access to formal credit at all.

It is important to distinguish between disbursements and the outstanding loan book. Maya's cumulative disbursements of ₱256 billion (USD $4.3B) reflect total loans ever made. The outstanding loan book, the actual on-book credit exposure at any point in time, stood at ₱27 billion (USD $450M) as of September 2025, up 59% year-on-year. Most of Maya's lending is short-duration consumer credit (Pay in 4, Flexi Loan, Personal Loan up to ₱250,000 / ~USD $4,200) that turns over quickly, which is why the outstanding balance is a fraction of cumulative volume.

Credit quality is the one area that needs honest scrutiny. In Q1 2025, Maya reported an NPL ratio of 3.8%, comfortably below the Philippine digital banking industry average. By end-2025, that ratio had climbed to 6.1%. That is a meaningful deterioration over the course of a single year and reflects the reality of pushing into broader, riskier borrower pools. It is still not alarming in context. 59% of Maya's borrowers had never accessed formal credit before using the platform, which means there is no prior credit history to underwrite against. The company is building credit profiles from scratch using AI-driven scoring on transaction data. But the direction of the NPL trend matters, and if it continues rising as lending scales into auto loans, housing loans, and supply chain financing (all of which management has flagged as 2026 priorities), that will be the metric to watch.

Maya posted ₱1.7 billion (~USD $28M) in net income in 2025, its first full year of profitability. It booked ₱1.6 billion (~USD $27M) of that in the first nine months. Revenue growth exceeded 100% year-on-year in 2024, and the Q1 2025 top-line accelerated further. This came just three years after the bank launched, which is a remarkably fast path to profitability for a digital bank operating in an emerging market.

On the payments side, Maya processed over ₱1 trillion (~USD $16.7B) in merchant payments in 2024, making it the largest merchant acquirer among Philippine digital banks. Visa has recognised Maya as the top acquirer for merchant transaction volume in the Philippines. The merchant acceptance infrastructure, built initially through the Maya Center agent network (formerly Smart Padala, which reaches deep into provincial and rural areas), gives Maya physical distribution that pure digital players struggle to replicate. 70% of Maya's customers live outside Metro Manila, and regional loan drawdowns surged 137% year-on-year in 2024.

The competitive dynamic between Maya and GCash is extremely tight, no doubt fuelled by the backing of Ant Group and Tencent. GCash has the user base and dominates peer-to-peer transfers and bill payments, while Maya has the banking license and deposit franchise, winning on deposit growth and credit product depth. Each product launched by one forces a response from the other, which has resulted in the Philippines leading the region on digital financial inclusion metrics.

Maya intends to IPO in 2026, targeting a dual listing, first in the US and then on the PSE in the second half of the year. If Maya lists at anything close to the multiples that Southeast Asian FinTech names have attracted in recent years, it would be the largest Philippine-origin tech IPO in history and would create a direct public market comp for GCash ahead of its own expected listing.

MoMo (Vietnam)

MoMo is Vietnam's dominant digital wallet, with over 40 million registered users in a country of 98 million people. It is a rare case of a Southeast Asian fintech that built scale without a SuperApp anchor.

MoMo grew as a standalone financial super-app, aggregating payments, lending, insurance, and investment services under a single brand without the benefit of a ride-hailing or e-commerce parent.

The company was founded in 2007 (as M_Service) and launched as an e-wallet in 2010. It has raised $434 million across five rounds, with the most recent being a $200 million Series E in December 2021 led by Mizuho, which valued the company at $2 billion. The cap table includes Warburg Pincus, Mizuho, Standard Chartered, Goldman Sachs, Goodwater Capital, and Kora Management.

MoMo’s current chairman is Anthony Thomas, the former CEO of GCash, which gives MoMo a direct connection to the operational playbook of one of the region's most successful digital wallets.

MoMo turned profitable for the first time on a full-year basis in 2024, with revenue growing 27% year-on-year. Revenue had grown from approximately VND 6 trillion (~USD $240M) in 2020 to VND 8.5 trillion (~USD $340M) by 2022, and the 2024 figure is likely north of VND 11 trillion (~USD $440M) based on the growth trajectory.

The company partners with over 50,000 businesses and more than 70 banks and financial institutions, with 300,000+ payment acceptance points nationwide. Its QR code infrastructure reaches into rural markets and traditional wet markets that international platforms have not penetrated.

In October 2024, MoMo repositioned itself from an e-wallet to an "AI-Powered Financial Assistant," signalling a strategic shift toward higher-margin financial services. The platform now offers micro-loans (through bank partnerships), insurance, investment products, stock trading, and BNPL with up to 45 days deferred payment. However, MoMo does not hold a banking licence and does not take deposits directly, which is a meaningful structural limitation compared to Maya or GXS. Its lending is intermediated through partner banks, meaning MoMo earns origination and servicing fees rather than net interest income.

The competitive landscape in Vietnam is more fragmented than in the Philippines or Indonesia. MoMo leads with an estimated 47-56% share of e-wallet users depending on the measure, but faces competition from ZaloPay (backed by VNG, Vietnam's largest tech company), ShopeePay (Sea Limited), VNPay (which dominates QR merchant acquisition for banks), and ViettelPay (backed by the military-owned telecom Viettel). The government's VietQR interoperability mandate, which has unified QR payments across 2.1 million merchants, has been a structural tailwind for adoption but also reduces the switching cost advantage that any single wallet player can build.

OVO (Indonesia)

OVO is arguably the most structurally interesting e-wallet in Indonesia. It was originally launched by the Lippo group (one of the largest real-estate conglomerates in Indonesia). It was then adopted by Grab as its Indonesian payments wallet in 2018 after Grab was unable to secure its own e-wallet license from Bank Indonesia.

In 2018, Grab invested in OVO, garnering roughly 40% share in the business. In 2021, it increased its stake to over 90% by purchasing shares from PT Tokopedia and Lippo Group.

OVO’s strategic significance lies in its integration with Superbank, the Indonesian digital bank backed by Grab, Emtek, Singtel and KakaoBank. In May 2025, OVO launched OVO Nabung by Superbank, a product that embeds a regulated bank savings account inside the OVO e-wallet. Users earn 5% annual interest on their balances with no minimum or fees, and can seamlessly use those balances for daily transactions. The product crossed one million users within five months of launch. Users who upgraded to OVO Nabung saw their average balances double and transaction frequency increase by 60%. One in three Grab driver-partners now uses OVO Nabung as their primary wallet and savings tool.

OVO Nabung creates a closed loop where OVO wallet users earn bank-level yield on their balances while Superbank gets sticky deposits with minimal acquisition cost, which it can then lend against. Superbank itself turned profitable for the first time in FY2025 (net income of 99.7 billion rupiah / ~$5.9M), with loans growing 50%, NIM of 10.64%, and gross NPL of just 2.6%. The cost-to-income ratio collapsed from 139% to 70.5% in a single year.

By end-2025, OVO had reached 121 million downloads and 3 million QRIS merchants across more than 800 cities and regencies. Over 40 million QRIS transactions were processed through the Grab ecosystem in 2025, with QRIS adoption growing 61% year-on-year across OVO's merchant base. More than 700,000 SME merchants saw transaction volumes increase by 35% through digital adoption.

Indonesia's QRIS system has been a structural tailwind for the entire wallet ecosystem. Bank Indonesia data shows QRIS is now used by nearly 60 million users across more than 40 million merchants (mostly SMEs), with transaction volumes growing 162.7% year-on-year as of July 2025. Gen Z accounts for 28% and millennials for 26% of total QRIS users.

The key question for OVO is whether the Superbank integration can scale fast enough to establish a deposit-funded lending flywheel before competitors catch up. GoPay is integrated with Bank Jago (GoTo's digital banking partner). ShopeePay has Monee behind it. Dana has the Sinar Mas banking relationship.

Indonesia's 277-million person market is large enough to support multiple winners, but the wallet that converts the most users into depositors and borrowers first will have the most defensible position. OVO's early traction with OVO Nabung suggests it is ahead on this metric but I believe this race is far from over.

GoPay (Indonesia)

GoPay is the fintech arm of GoTo Group, formed from the merger of Gojek and Tokopedia in 2021. It is the most direct competitor to OVO in Indonesia, and alongside ShopeePay, one of three wallets with a captive SuperApp ecosystem in the country.

GoPay launched in 2016 as a payments solution for Gojek users and driver-partners. It has since spun out into a standalone app (launched 2023) designed to reduce data usage and reach mass-market users with less powerful phones.

The standalone GoPay app has seen a growth inflection point, monthly transacting users reached 24.2 million in Q3 2025, up 29% year-on-year, and GoTo surpassed 500 million transactions in a single month for the first time in September 2025. By Q4 2025, digital payments volume hit IDR 120 trillion (~$7.5B) for the quarter.

It also has a relatively large lending business. GoTo Financial's consumer loan book expanded rapidly through 2025, reaching IDR 7.6 trillion (~USD $457M) by Q3 2025, up 76% year-on-year, with management guiding to exceed IDR 8 trillion (~USD $480M) by year-end. For the full year, GoPay's Fintech segment achieved Adjusted EBITDA of IDR 497 billion (~USD $30M), its first full year of profitability. Lending revenue grew 130% year-on-year to IDR 879 billion (~USD $53M) in Q2, and 84% year-on-year to IDR 1.0 trillion (~USD $60M) in Q3. Roughly 60% of loans outstanding originate through the GoPay and Gojek apps, with those in-ecosystem channels growing faster than third-party platforms.

The TikTok partnership has added an unexpected distribution channel. After TikTok acquired 75.01% of Tokopedia in late 2023, GoPay became embedded in the TikTok Shop checkout flow. GoTo launched GoPay Pinjam (instant cash loans) directly within TikTok Shop in 2025, making it the first platform in Indonesia to offer cash lending inside the TikTok ecosystem. BNPL on TikTok Shop and Tokopedia has shown strong momentum, and the partnership with Telkomsel (Telkomsel Wallet by GoPay, embedded in the MyTelkomsel app) further extends distribution.

GoTo holds a 22% stake in Bank Jago, an Indonesian digital bank that serves as GoPay's banking partner. The GoPay Tabungan by Jago product, launched in late 2023, embeds a Bank Jago savings account inside the GoPay and Gojek apps, mirroring the OVO Nabung by Superbank model. Users can open an account in two minutes, earn interest on balances, and use them seamlessly for payments across the GoTo ecosystem and all QRIS merchants. GoTo has also launched GoPay Asuransi (insurance), GoPay Simpanan (investments), and GoPay Pinjam BPKB (collateral-backed loans) on the consumer app, progressively building a full financial services stack.

GoPay turned profitable on an Adjusted EBITDA basis for the first time in FY2025, reaching IDR 497 billion (~USD $30M) for the full year. Financial services revenue nearly doubled in 2024 to IDR 3.7 trillion (~USD $230M). GoTo itself posted its first pre-tax profit in Q3 2025 (IDR 62 billion / ~USD $3.4M) and raised its FY2025 Adjusted EBITDA guidance to IDR 1.8-1.9 trillion.

GoTo's fintech segment is arguably the most under-followed listed fintech asset in the region, given that most international investor attention goes to Sea Limited and Grab. Unfortunately, I do not think GoTo as a whole is investable, due to the declining ride-hailing and food delivery business that makes up a large majority of group revenues.

DANA (Indonesia)

DANA is a digital financial services business based in Indonesia that was founded in 2017 as a joint venture between Emtek (one of Indonesia’s largest media conglomerates) and API Investment Limited, an investment arm of Ant Group. It launched in 2018, later than competitors such as GoPay and OVO but has since built scale.

It first got its start through being deeply integrated with Bukalapak (Emtek-backed Indonesian e-commerce player) and Lazada (Alibaba-owned). In 2022, Lazada purchased $304.5M of DANA shares from Emtek and Sinar Mas Group invested a further $225M to make it one of the largest shareholders.

DANA claims to have over 200M registered users today and as of 2023, processed an average of 10M transactions each day. DANA’s structural challenge is that it lacks a captive ecosystem. GoPay has GoTo (Gojek + Tokopedia) while OVO has Grab, and ShopeePay has Shopee. DANA’s e-commerce partners have either shut down or are not exclusively tied to it. This makes DANA the most exposed of each of Indonesia’s major wallets to the commoditising effect of Indonesia’s QRIS interoperability mandate, which requires all wallets to accept a unified QR standard across over 40 million merchants. (When every wallet works everywhere, wallets with the weakest ecosystem lock-in will be the most vulnerable)

That said, the Ant Group and Sinar Mas backing gives DANA optionality. For instance, if DANA can integrate with Bank Sinarmas for deposit-funded lending (similar to the OVO-Superbank model), it could transition from a pure-play payments wallet into an embedded finance player.

Competitive Landscape

Looking across these players, I believe there is a clear distinction between some of them. The most useful lens to view them is not by country or product vertical as these can easily change overnight, rather I believe it is best viewed through structural origin.

Where these companies originated and their backers, determines the data they have access to, the distribution they can leverage and ultimately what kind of moat they can build.

When comparing across this list, there are a few insights that I believe we can takeaway.