Sea Limited Q1 2026 Earnings Review

47% Revenue Growth, Highest in 16 Quarters. All 3 Segments Accelerating

Revenue: $7.1B v $6.4B (+46.6% YoY) 🟢

EPS: $0.70 v $0.77 🔴

Sea Limited reporting earnings on 12th May before the market open.

The stock closed the day up 13%.

Selected Key Metrics

Total Gross Profit: $3.145B (+40.7% YoY)

Total Net Income: $438.22M (+6.7% YoY)

Total Adjusted EBITDA: $1.034B (+9.3% YoY)

Cash & Cash Equivalents: $11.1B (up from $10.3B in Q1 2025)

E-Commerce (Shopee)

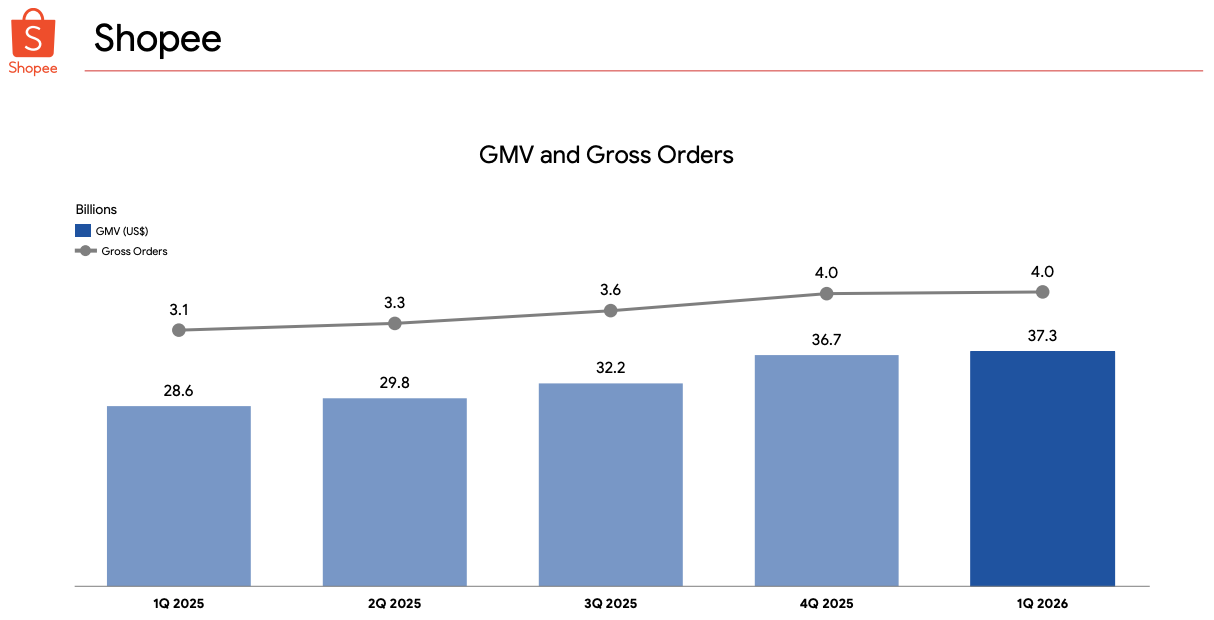

Gross Orders: 4.0B (+29.3% YoY)

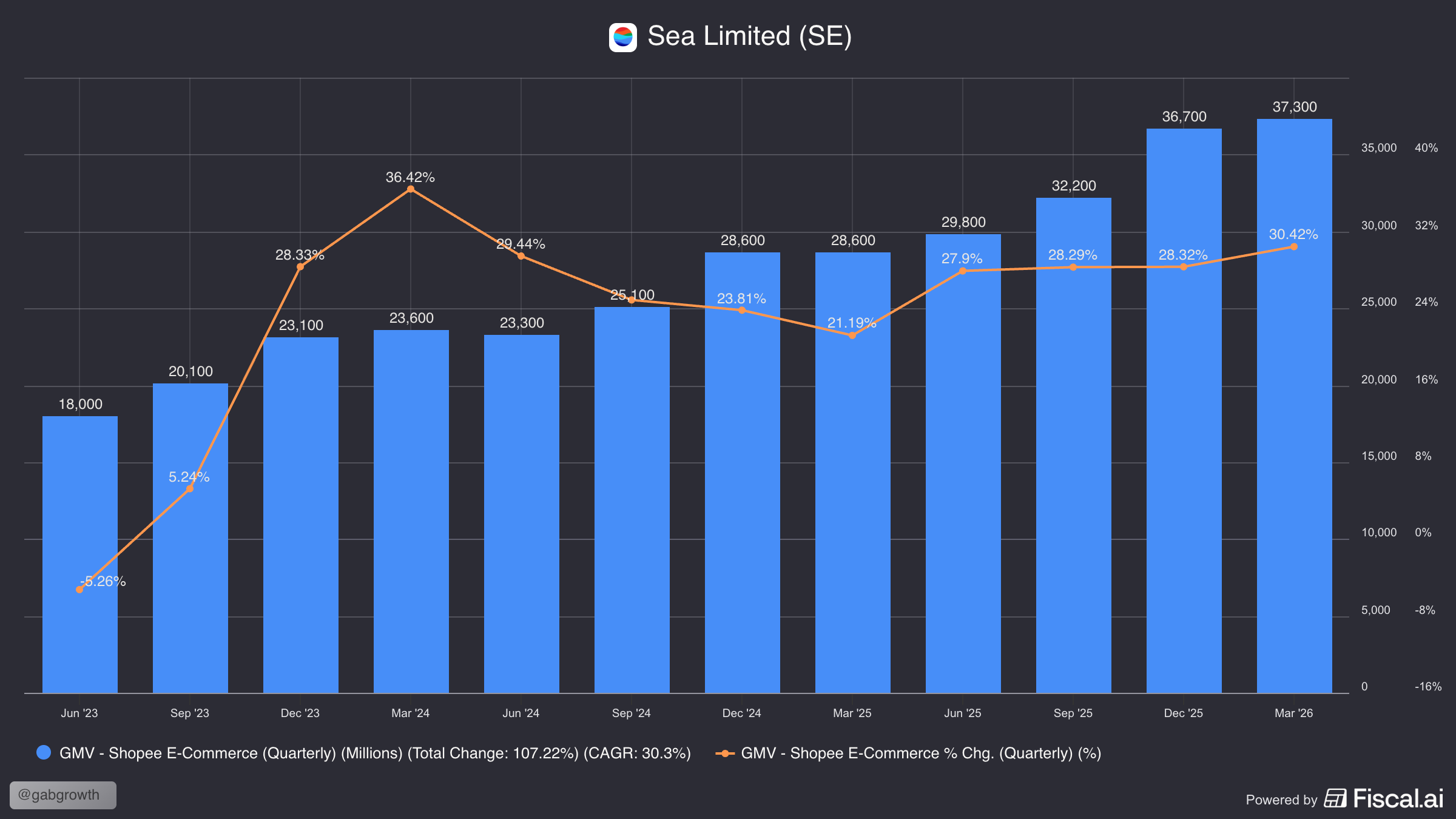

GMV: $37.3B (+30.2% YoY)

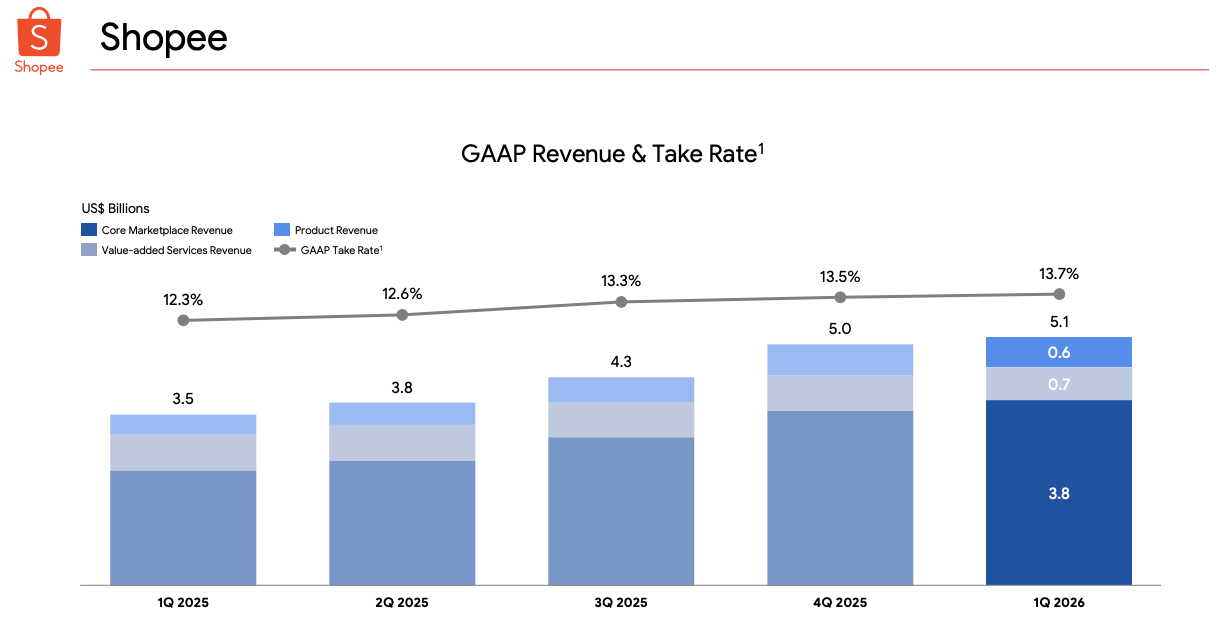

Revenue: $5.1B (+45.1% YoY)

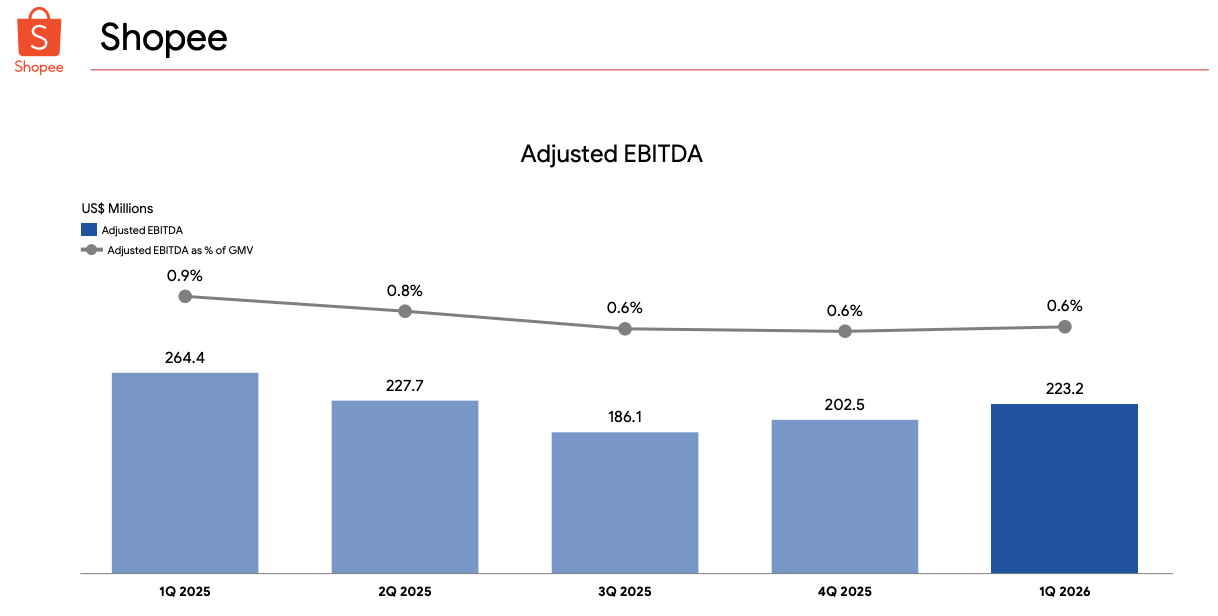

Adjusted EBITDA: $223.2M (-15.5% YoY)

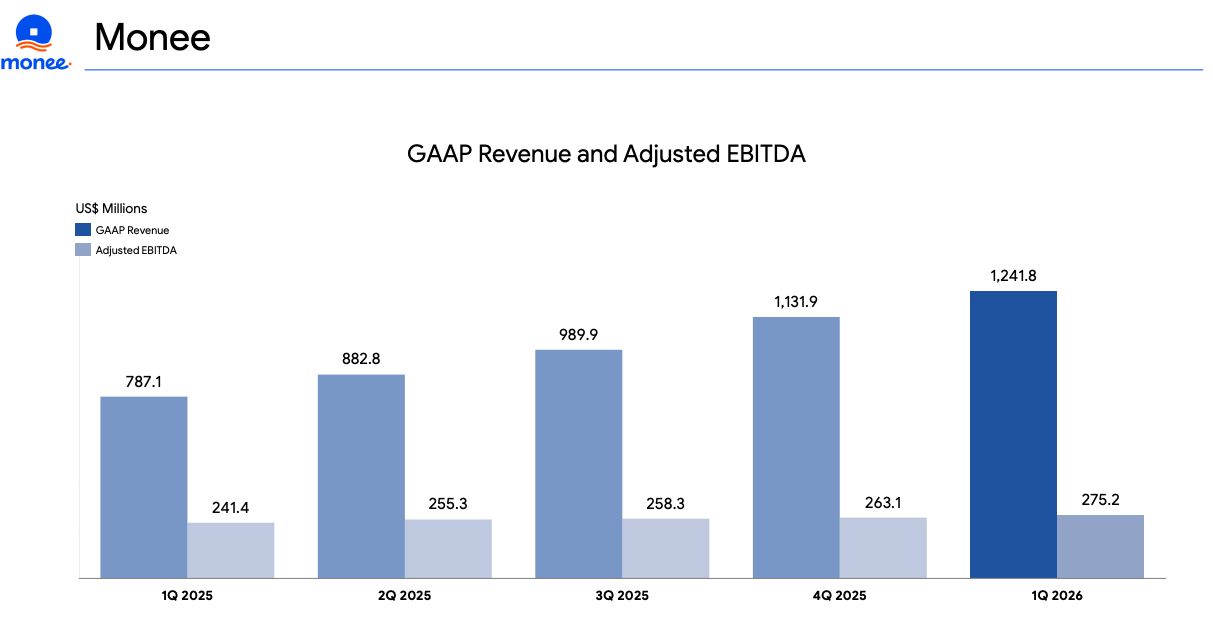

Digital Financial Services (Monee)

Consumer & SME Loans Outstanding: $9.9B (+71.3% YoY)

Revenue: $1.2B (+57.8% YoY)

Adjusted EBITDA: $275.2M (+14.0% YoY)

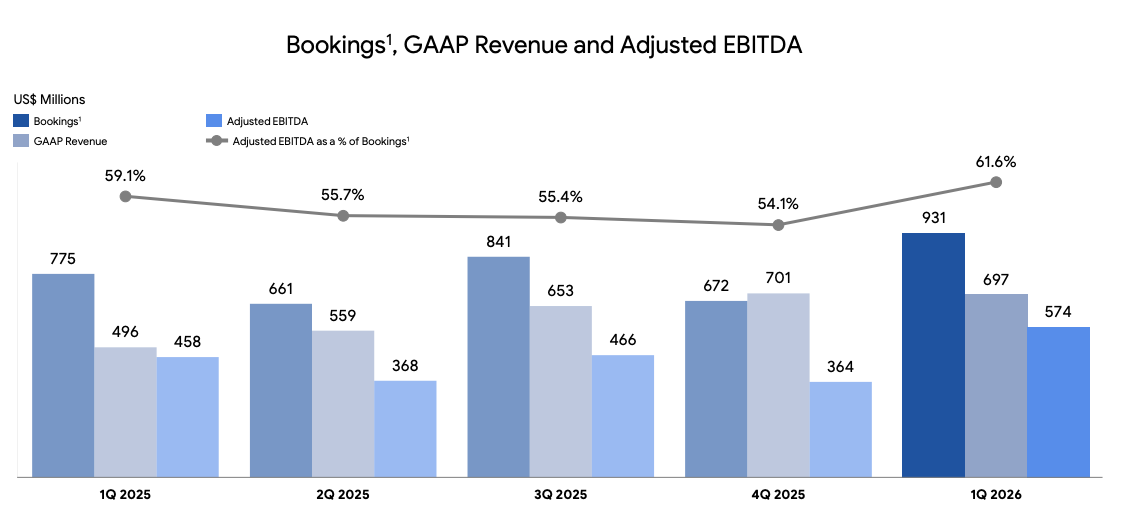

Digital Entertainment (Garena)

Bookings: $931.4M (+20.1% YoY)

Revenue: $696.6M (+40.6% YoY)

Adjusted EBITDA: $573.6M (+25.2% YoY)

Quarterly Active Users: 666.5M (+0.7% YoY)

Quarterly Paying Users: 72.6M (+12.4% YoY)

Quarterly Paying User Ratio: 10.9% (vs 9.8% in Q1 2025)

Share Repurchase Program

Repurchased 1.8M shares for an aggregate of $168.4M = $93.55 per share

Sea Limited saw a massive top-line beat, beating estimates by over 10%. The bottom-line missed, but again, this was to be expected as the focus is on investing in logistics and Shopee VIP to maintain its lead. More on this later.

As I’ve discussed often, my base case is >20% growth for the decade to come. Growth has only accelerated since. All 3 segments are growing top-line over 40%, which is absolutely incredible to see. I continue to think this is one of the most asymmetric investments in the market.

Table of Contents

Shopee (E-Commerce)

Monee (Digital Financial Services)

Garena (Digital Entertainment)

Management Commentary

Concluding Thoughts

1. Shopee (E-Commerce)

Shopee’s GMV hit a new all-time high this quarter, making it the 8th consecutive quarter of growth. Sequential growth of $700M is especially impressive considering seasonality of Q4 to Q1. In addition, monthly active buyers were up 16% YoY and monthly average purchase frequency grew around 12% YoY. So before even considering average order value, Shopee’s buyer activity implies roughly 30% YoY growth in purchase occasions. This shows habit formation is increasing.

Management reiterated guidance of 25% GMV growth, which I expect to be hit relatively easily. As we can see, GMV growth has maintained over 20% for the past 10 quarters, a huge feat in itself.

Shopee’s GAAP take rate continued to climb, up to 13.7% this quarter.

A large reason for the 13% stock price increase was this slide. Adj. EBITDA margin as % of GMV appears to have stabilised at 0.6% following the previous quarters’ drops.

Management reiterated their guide for “full year adjusted EBITDA no lower than that of 2025 in absolute dollar terms”.

The reason for the slowdown in Adj. EBITDA growth is of course due to the Shopee VIP program that has been a huge success. So far, member growth has been exponential:

Q1 2025: 1M members

Q2 2025: 2M members (+100% QoQ)

Q3 2025: 3.5M members (+75% QoQ)

Q4 2025: 7M members (+100% QoQ)

Q1 2026: 10M members (+43% QoQ)

Despite the rapid growth in VIP members, it represents just 2.5% of the entire active user base of Shopee (400M people). Incredibly, these 2.5% of users make up ~20% of total GMV, as revealed by management. This implies that VIP members spend on average 9.75x more than non-VIP members.

Shopee Ads

In Q1 2026, ad revenue grew 80% YoY and ad take rate increased by over 90bps. Ad-paying sellers and their average ad spend both increased by ~35% YoY.

This was an inflection in growth from Q4 2025 which I mentioned in the previous earnings report was something I expected. Ads continue to be a key contributor to the bottom-line and will get larger over time.

Shopee Logistics (SPX Express)

In Indonesia, Shopee’s instant delivery order volumes grew over 35% YoY with cost per order reducing ~20% YoY in Q1 2026. This is the shift towards quick commerce that I have been discussing. Contrarian Perspectives and I wrote a full length article (FREE) on this that discussed how China’s quick commerce landscape was moving to Southeast Asia. Shopee happens to be at the bleeding edge of it:

[Deep Dive] Alibaba, Meituan and JD's Quick Commerce War and How Grab and Sea Will React

![[Deep Dive] Alibaba, Meituan and JD's Quick Commerce War and How Grab and Sea Will React](https://substackcdn.com/image/fetch/$s_!4Mkm!,w_1300,h_650,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Ff095ce3c-1df7-4f3f-8a08-fc995b484668_1200x630.png)

This piece was written in collaboration with Zack Zhu, who publishes Contrarian Perspectives and is one of the sharpest analysts I know. Zack anchored the China section with ground-level insight into how Meituan, Alibaba, JD, and Douyin are actually fighting this battle, and why the unit economics matter more than the headlines.

Management also noted that fulfilment order volumes grew ~25% QoQ in Q1 2026. In Asia, over one third of parcels fulfilled by SPX Express were delivered within the next day in March.

Shopee VIP Program

As we discussed earlier, the Shopee VIP program is front and center of focus now. Management shared that VIP members total over 10 million, growing over 40% QoQ, with program retention averaging over 80%.

This is extremely impressive and only possible due to Monee’s capabilities. Management discussed that for a paid VIP programme, the hard part is not only convincing users to subscribe. It is getting the subscription to renew successfully every month.

In markets with high credit-card penetration, this is easier because the card just gets charged automatically. But in Shopee’s markets, many users do not have credit cards, so subscriptions can fail when moving from one month to the next.

Chris Feng said Shopee solved this by working closely with Monee to create a smoother payment process for Shopee VIP. As a result, Indonesia’s VIP renewal rate improved from around 40% to 70% over the past few quarters.

2. Monee (Digital Financial Services)

Monee continued with yet another record quarter of loans principal outstanding. Its loan book grew ~70% YoY to $9.9B while the NPL ratio held steady at 1.1%.

There are now over 38 million active credit users on the platform, up more than 35% YoY. Average loan outstanding per user also grew to ~$250 at the end of the quarter, up 25% YoY.

Brazil has become the 4th market to cross $1B in loan book size, growing over 250% YoY. As we can see from Mercado Pago’s numbers in the region, Brazil is certainly a massive market for growth.

Brazil is still very early in Shopee’s FinTech monetisation curve. SPayLater GMV penetration is only ~10% in Brazil, well below mature Shopee markets. This suggests that Brazil has much room to grow. SPayLater usually increases conversion rate + basket size + purchase frequency + retention, which is a natural flywheel for Shopee.

GAAP revenue for the quarter came in at $1.24B. Adjusted EBITDA continued climbing, to $275M for the quarter.

The key to watch here is off-Shopee momentum. Management shared that following strong momentum in Malaysia, they are also seeing good traction in Thailand and Indonesia, with off-Shopee SPayLater loans in both markets exceeding 20% as of end-March.

There is also strong growth in higher-value categories such as electronics and two-wheelers in Indonesia, where instalment credit plays a meaningful role in enabling such purchases.

Again, the major worry I have here is off-book loans. They are growing very slowly compared to on-book loans. This will take time, as 3rd party financial institutions are difficult to convince, typically requiring default history across economic cycles, regulatory approvals in each individual market, and a minimum track record on the specific product.

3. Garena (Digital Entertainment)

Garena had a stellar quarter in Q1, with the strong quarter of results since 2021. Bookings came in at $931M, against a significantly high comparable last year. This was driven by a huge increase in the Quarterly Paying User Ratio, up from 9.8% in Q1 last year to 10.9% this quarter.

Management cited strong response to Free Fire’s collaboration with Jujutsu Kaisen, which generated over 700 million official content views. It appears that Garena has mastered IP collaboration, with last year’s NARUTO SHIPPUDEN also being a massive success. They also pointed towards Arena of Valor which delivered record high quarterly bookings this quarter, its tenth year of operation.

Again, the continued success of Free Fire, which is in its 9th year of operation proves that many of these hit games are certainly evergreen.

4. Management Commentary

This section focuses mainly on questions during the earnings call, with key highlights of what I believe are important points to takeaway. I may adjust a few words here and there for clarity purposes, (English is not the first language for the majority of Sea’s management team) but I will not change the meaning of these quotes.

On Quick Commerce:

“In Indonesia, our instant delivery service can deliver orders in as little as 2 hours in urban areas. Order volumes for this service grew over 35% in the first quarter with cost per order reducing by around 20% year-on-year.

Building this service has enabled us to expand our product assortment into higher frequency categories. We expanded partnerships with major convenience stores and the pharmacy chains such as Indomaret.

At the end of March, we had around 7,000 offline stores available on our instant services. This has shifted more offline purchasing behavior online and into the Shopee ecosystem.”

On Shopee Taiwan:

“In Taiwan, our collection point network expanded to over 3,100 locations at the end of the fourth quarter, nearly 50% more locations compared to just a year ago.

We leveraged our growing fulfilment capability to scale initiatives such as shipping directly to lockers without additional packaging, improving speed while reducing costs. With these efforts, average buyer waiting time improved 12% in the first quarter year-on-year.

We reported double-digit GMV growth year-on-year in the first quarter in Taiwan”

On Shopee’s Content Ecosystem:

“Our content ecosystem continues to grow healthily. In the first quarter, orders from live streaming and short-form video grew more than 50% year-on-year.

These orders accounted for more than 25% of total physical goods orders in Southeast Asia. To further strengthen our content ecosystem, we continue to deepen our content partnerships.

Orders driven by YouTube more than doubled year-on-year. Our collaboration with Meta is scaling well with over 4.5 million affiliates across our market, up nearly 30% quarter-on-quarter. In Indonesia, we have extended our Meta collaboration to enable seamless product promotion and checkout, not just on Facebook, but also on Instagram.”

On Shopee Brazil:

“We continued to improve delivery time by more than 1 day in the first quarter compared to last year. We opened 3 new fulfilment centers, bringing our total to 5.

This effort allowed us to onboard more merchants, especially to Shopee Mall, supporting stronger spending among buyers. In the first quarter, GMV from Shopee Mall sellers more than doubled year-on-year and now contributes around 15% of GMV.

We remain confident in Brazil’s long-term growth potential and in our ability to further strengthen our competitive position in this market.”

On Shopee Brazil’s Profitability:

“We have been profitable in Brazil for the last few consecutive quarters. I don’t foresee any change towards that at this point in time.

We will continue to grow healthily in Brazil, likely with the profitable kind of margins we see right now.”

On Shopee Brazil’s Fulfilment Potential & Plans:

“On the fulfilment business, especially in Brazil, we do expect fulfilment to become a larger percentage of the business as we continue to build it out.

We only started not too long ago, so we are still in the early stages of scaling our fulfilment operations. Typically, we do not overbuild too aggressively. Our fulfilment centre capacity utilisation is relatively high because we are able to forecast fulfilment volumes well ahead of time, and then build our fulfilment centres according to that timetable.

So it is unlikely that we will build a lot this year, stop next year, wait for demand to catch up, and then start building again. Instead, we expect this to be a continuous process as we scale our fulfilment network.

Ultimately, we would like our fulfilment network to be larger than our closest competitors in the market, in terms of absolute volume.

In terms of the return on investment, if you look at individual fulfilment centers, typically, the CAPEX is actually not that high as we don’t own the fulfilment center itself.

We typically rent a fulfilment center. The CAPEX essentially is to make sure the fulfilment center is well equipped. So if you look at that particular part of investment, the return on investment is pretty fast.

It’s not that long ahead of the time. The other product investment we’re doing for the fulfilment businesses is more about moving the seller to be a part of the fulfilment center and advocating the buyers to understand the fulfilment business that we have. So that’s part of the ongoing investment we use to drive business growth.”

On the Impact of Oil:

“The first-order impact is the absolute oil price, which does affect our operating costs.

The positive is that, in many of the countries we operate in, we benefit from government subsidies that help absorb part of the cost increase, especially in last-mile delivery, which is the largest component of delivery cost. We also work closely with our partners, such as our line-haul and airline partners, to manage costs together.

So overall, if you look at actual costs, higher oil prices do have an impact. But we believe we can manage this within the guidance we have provided. And from a timing perspective, you are right that Q2 will likely see a larger cost impact than Q1.

The second-order impact is that higher oil prices could affect consumer spending power in some countries, especially if people have to spend more money at the gas station. That said, we are generally seeing only a moderate impact on our platform.

The main reason is that our platform is one of the cheapest places for consumers to find the products they need. So when people are looking to save money, they actually tend to come to us more. Our platform is also more focused on essential products, rather than luxury or highly discretionary spending. Compared to offline spending and other discretionary categories, our platform is less exposed to that kind of pullback.

All of this helps reduce the second-order impact we see from higher oil prices.”

On Monee/SPayLater’s Expansion Beyond Shopee:

“On the split between On-Shopee and Off-Shopee, SPayLater usage on Shopee was the majority of the business when we first started. Today, it is already less than half of the business.

Even when you compare SPayLater usage on Shopee versus off Shopee, SPayLater on Shopee now represents only around 20% of total expenditure across both On-Shopee and Off-Shopee channels. This is a significant milestone for us.

It proves that we are not only able to drive credit adoption within the Shopee ecosystem, but that we have also successfully expanded it beyond Shopee. In fact, we are seeing higher growth in the Off-Shopee ecosystem compared to the On-Shopee part of the business.”

On Factors Driving Monee’s Growth:

“There are three key factors driving this growth.

First, within our existing user base, we still see significant room to drive more credit adoption. This will come from more product rollouts, better credit assessment as we accumulate more data over time, deeper integration with Shopee, and the expansion of more non-Shopee use cases for these users. Essentially, even within the same user base, there is still a lot of room for us to deepen credit penetration.

Second, we are expanding into new usage scenarios beyond what we have today. This includes partnering with more online merchants that can accept SPayLater, as well as more offline merchants that can accept SPayLater.

In some markets where credit card usage is more developed, we have also rolled out a debit card product that leverages the user’s existing credit limit. This allows users to spend their SPayLater credit through the card network as well. All of this expands the addressable market for our existing user base.

Third, we will continue to expand into new user segments. This is also very important for us. As Forrest mentioned in the opening remarks, we initially started more with the subprime segment. But as we accumulate more risk data and improve our risk models, we are able to expand into more prime user segments with slightly different products across different markets.

These users may have slightly lower ROA, but they give us access to a much larger outstanding loan pool.

Overall, we believe these factors will continue to drive the growth of our lending business across our markets in the coming years.”

5. Concluding Thoughts

As I write this, the stock is down over 3% today, following a 2% down day yesterday, wiping out a large portion of gains.

We are clearly in an environment where the market is focused on companies on the AI train. That, combined with the uncertainty of oil, in my view is what has led to the weakness in Sea Limited stock in the past couple of months. Of course, there is also the overhang of TikTok Shop, Mercado Libre and other competitors, and what it does to Shopee’s margins.

Personally, I think these set of results that Sea has displayed, shows that reinvesting in the business today, both in logistics and the VIP program are the right decisions. Much of my conviction in continuing to buy Sea is trust in the management team. They have proven their ability to out-hustle and out-compete their closest rivals in the past. I believe this is no different.

From a simple SOTP or a very conservative discounted cash flow, Sea is a steal at these prices. Frankly, I have been flabbergasted by the reaction of the market to its extremely strong earnings results. However, this is simply how the market reacts in the short term.

As long-time followers will know, this does not faze me, and I hope it doesn’t faze you either. If there was a deterioration in the quality of the business, I would certainly highlight it. Yet, I believe this was possibly one of the best quarters the business has put up. All 3 segments are firing on all cylinders.

Should the stock revisit the $70s, I will certainly be a buyer again.

Paid Subscription Upgrade

If you’d like to support the work I do, consider becoming a paid subscriber. Your support will allow me to spend more time finding asymmetric opportunities in the market, writing and analysing various businesses.

As a reminder, paid subscribers get access to:

Monthly Portfolio Updates

Earnings Reviews on Portfolio Companies (SE, GRAB, DLO, MELI etc)

Archive of Deep Dives and Posts (16 Deep Dives and counting)

Southeast Asian coverage of industries and companies

Disclaimer: The content presented in this thesis is for informational and academic purposes only and does not constitute financial advice. The analysis and opinions expressed are based on research and should not be interpreted as a recommendation to buy, sell, or hold any security. Readers should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.