Rubrik Q4 2026 Earnings Review

Another Fantastic Quarter by Rubrik. Are the Software Disruption Fears Warranted?

Rubrik reported Q4 2026* earnings after the market close on 12th March 2026.

Revenue: $377.7M v $342.3M est. (+46.3% YoY, +7.9% QoQ) 🟢

ARR: $1,460M v $1,441.5M est. (+33.6% YoY) 🟢

EPS (Non-GAAP): $0.04 v -$0.11 est. 🟢

*Note that Rubrik’s fiscal year ends on January 21. In essence:

FY2025 = Feb 2024 → Jan 2025

FY2026 = Feb 2025 → Jan 2026

FY2027 = Feb 2026 → Jan 2027

Selected Key Metrics

2,805 customers with $100K or more in subscription ARR, up 25% year-over-year

GAAP Gross Margin: 82%, 6th consecutive quarter of increase

NPS remains in the top 1% of SaaS businesses

Table of Contents

Introduction

Financials

Guidance

Management Commentary

Concluding Thoughts

1. Introduction

Rubrik is an American cloud data management and data security company based in California. It started as a challenger to traditional storage and disaster-recovery vendors, but has since evolved into a cybersecurity-driven data protection platform.

Rubrik helps companies to stay resilient against attacks and recover fast when disaster strikes, protecting enterprise workloads across on-premise, cloud, and SaaS environments.

Rubrik was first pitched to subscribers on 22 September at $80 following the earnings drop of 18% in Q2’26. This is the second earnings report since owning the business. Since the initial pitch, I’ve added to the position multiple times.

It is now my 6th largest position, just outside my 5 core positions in the portfolio. Let’s break down the earnings results.

2. Financials

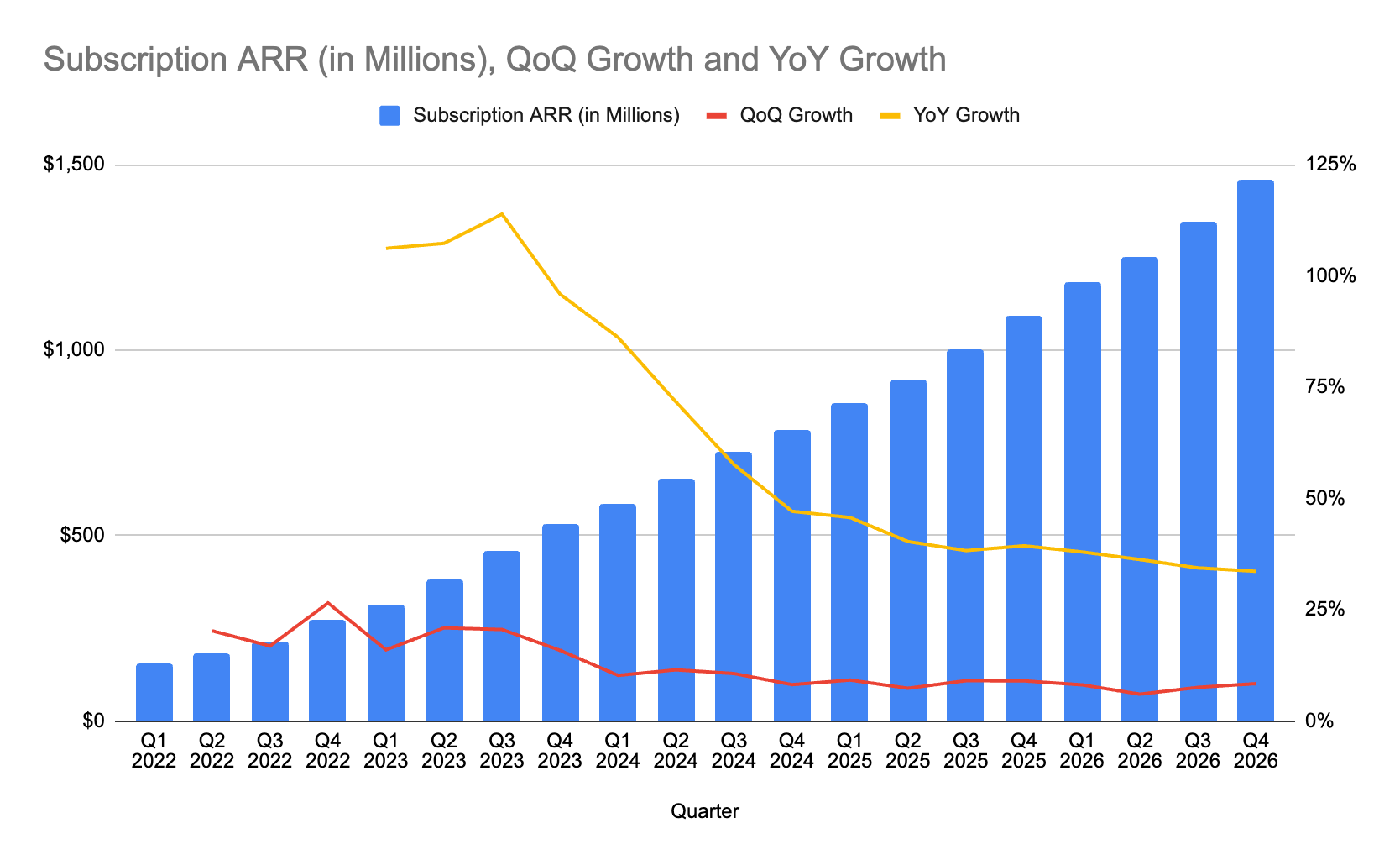

Subscription ARR

This refers to the annual run rate from subscription contracts. For Rubrik this is the core recurring business coming from Security Cloud subscriptions, SaaS protections, and legacy subscription contracts tied to appliances or software. It excludes one-time services and hardware sales, so it is the cleanest signal of recurring scale.

Rubrik’s subscription ARR for Q4 2026 came in at $1.46B, up 34% YoY. Growth has understandably slowed in recent quarters as per the law of large numbers.

That said, it is good to see that growth has somewhat stabilised. If Rubrik maintains its subscription growth rate above 30%, it would be massively encouraging.

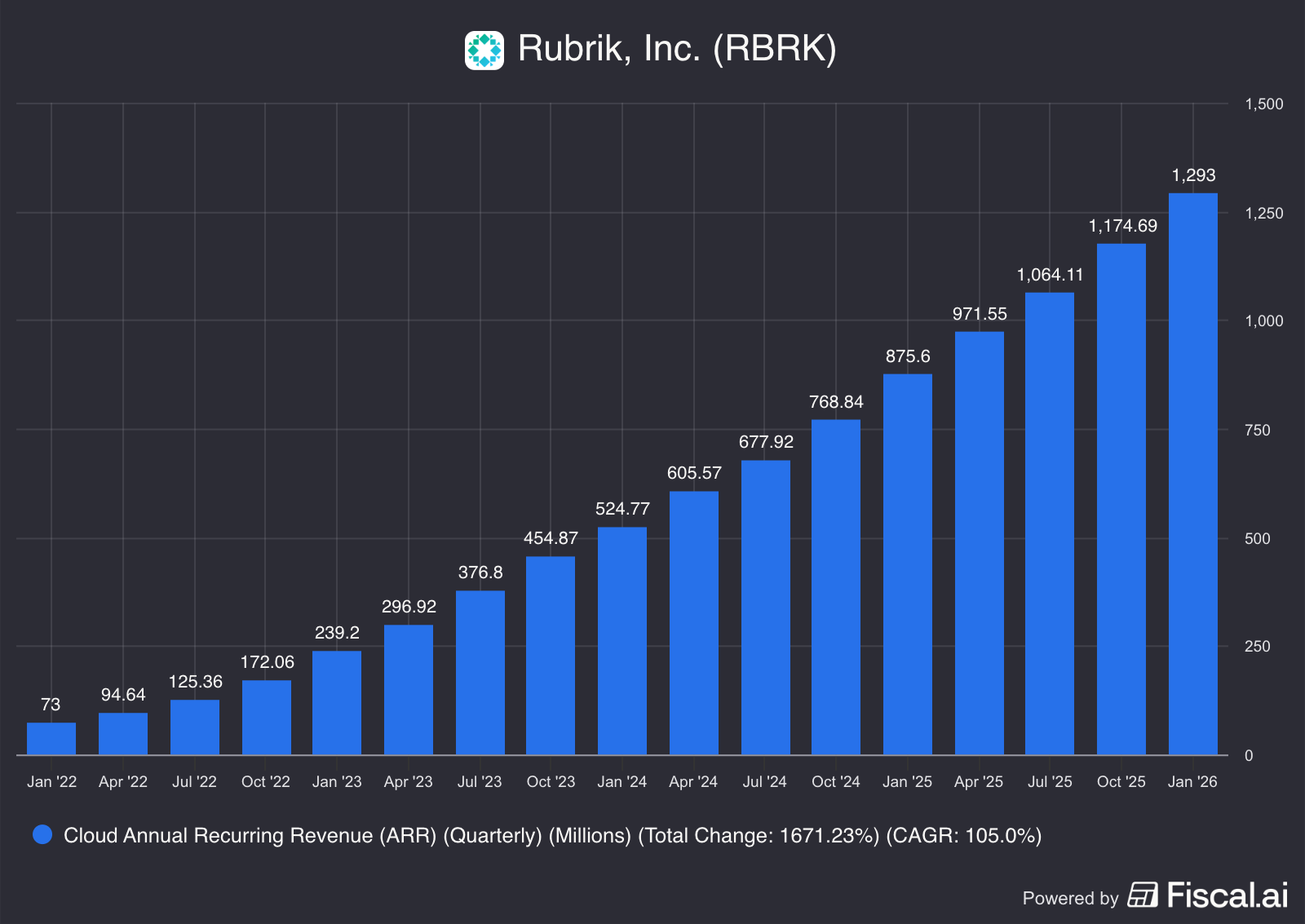

Cloud ARR

Cloud ARR isolates the portion of subscription ARR coming from Rubrik’s cloud native products, principally Security Cloud and other SaaS protections. This is the revenue that validates Rubrik’s move from on-prem backup into cloud first security services.

Cloud ARR this quarter came in at $1.293B and grew faster than total ARR again (48% v 34%). This is a strong sign for Rubrik that customers are buying the cloud offering at scale and that the cloud portfolio is driving a majority of the company’s growth.

Again, this is key as cloud ARR typically has better land-and-expand mechanics and lower cost-to-serve over time. This leads to higher margins moving forward.

Average Subscription Dollar-Based NRR

Rubrik has not disclosed its exact NRR but has maintained >120% NRR for the nth consecutive time. Since disclosing this metric from the S-1, it has never went below 120%. This is a key indicator of strength for the business as it implies existing customers are expanding well beyond what is lost to churn.

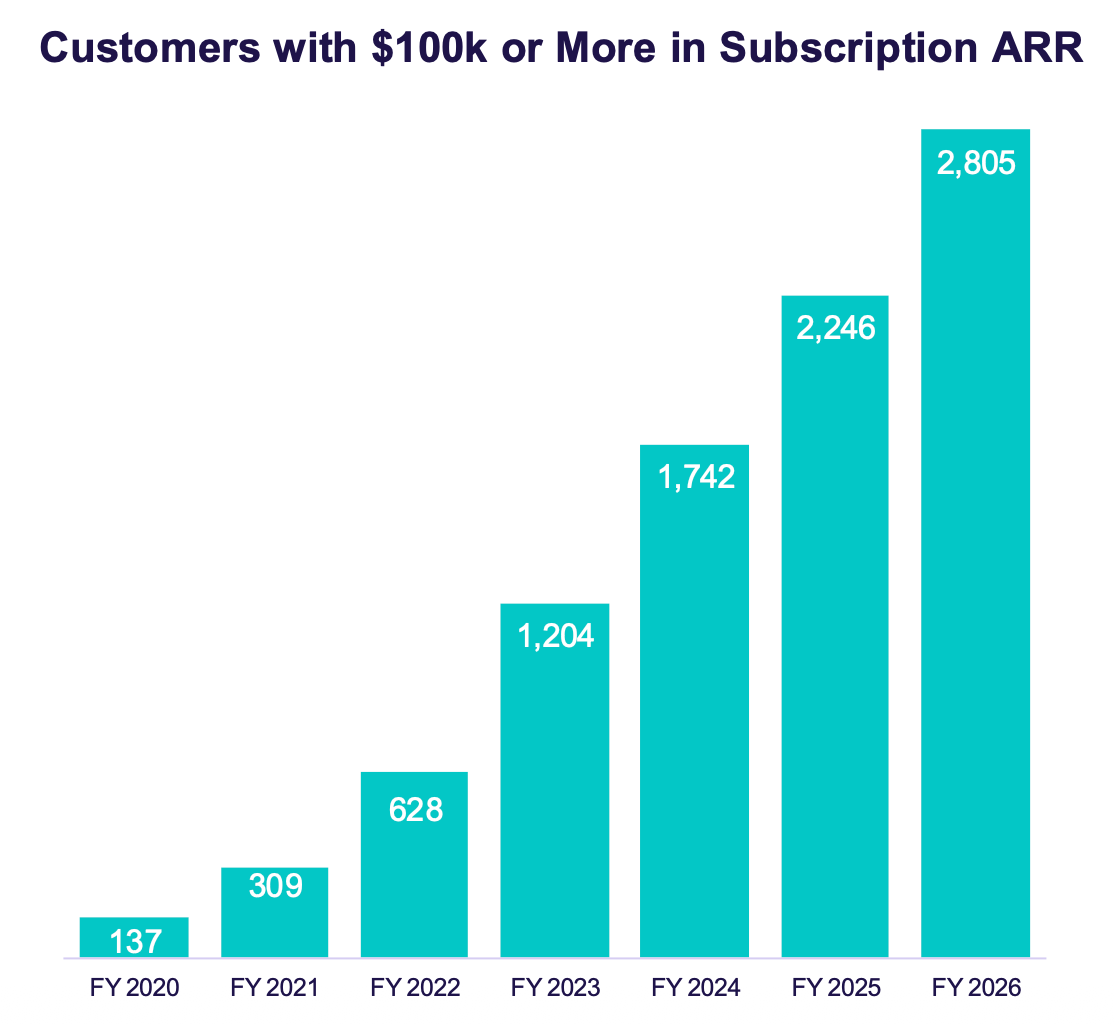

Customers with $100K+ in Subscription ARR

Another key indicator is the number of high-value customers where Rubrik is most likely to land strategic, high-value contracts. For Rubrik these are the accounts most likely to be mission critical and to adopt multiple modules.

As of Q4, Rubrik has 2,805 customers with $100k or more in subscription ARR, up from 2,085 last year. This represents 25% YoY growth, which is a slight drop from prior quarters numbers but is to be expected with the law of large numbers.

3. Guidance

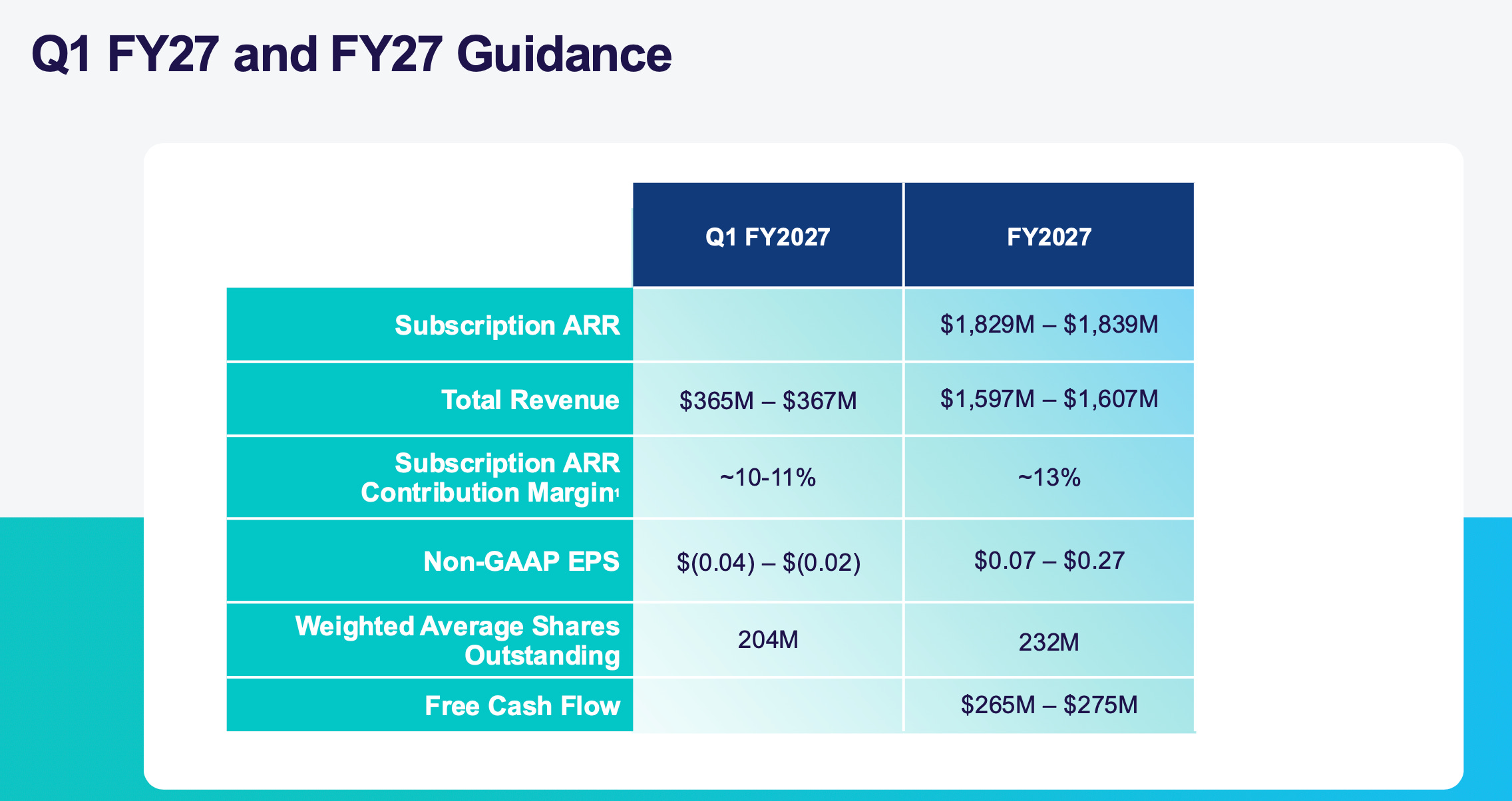

Rubrik’s management are notorious sandbaggers. They’ve guided for a midpoint revenue of $366M in Q1 2027, which implies 31.4% YoY growth. I expect the actual numbers to come in materially higher.

For FY2027, management has guided for subscription ARR of $1.834B and total revenue of $1.602B which would imply 45% and 21.7% growth respectively. While these numbers are sandbagged, it still feels rather low to me at 21.7% (normalising for material rights, ~27-28%), considering FY26 growth came in at 48.4%.

Q4 saw a weighted-average shares outstanding of 200.8M, and it is expected to continue climbing to 204M in Q1’27. For FY27, Rubrik is guiding for weighted average shares outstanding of 232M. That would represent 15.4% growth in shares outstanding.

That represents massive dilution incoming, albeit largely priced in by the market.

*The stock compensation plan first set out by management was planned pre-IPO and with many stock price targets hit in 2024/2025. This accounts for ~15.5M additional shares. If we consider just new SBC alone, the number is closer to 6M shares. At a base of ~200M, that is about 3% dilution, which is rather palatable.

This remains one of the key risks for shareholders.

4. Management Commentary

On Rubrik’s Core Value Proposition

“Rubrik is the system of record of last resort around data and identity when a large bank or hospital faces a ransomware attack. Data infrastructure and recovery capabilities are foundational to enterprise resilience.

Our platform is built through more than a decade of engineering and enterprise feedback. This technology foundation allows organizations to restore business operations quickly when cyber incidents occur.”

On Vibe Coding & LLMs

“You can close the windows and put on the locks, but ultimately, you need a bunker underneath your house to survive the doomsday, so your cloud and AI transformation journey continues uninterrupted. Rubrik Security Cloud is that bunker for enterprises. When ransomware inevitably hits, a LLM or Vibe code will not recover your business, Rubrik will.”

On Rubrik’s Identity Protection Product

“We have been rapidly disrupting the identity protection market. In just a few quarters this business grew to more than 900 customers, making it the fastest-growing product in our company’s history. In Q3, we had reported that we had crossed 400 customers.

Protection for Okta Identity allows Rubrik to span Okta, Active Directory, and Entra ID. Identity infrastructure has become a primary target for cyber attackers.”

On Rubrik’s Competitive Positioning

“Our competitive win rates exceeded 90% in the fourth quarter. Customers are increasingly turning to Rubrik to accelerate AI transformation while strengthening cyber resilience. Organizations can begin with data protection, cloud security, or identity resilience and expand across the platform over time.”

On Rubrik Agent Cloud

“Last quarter, we shared that Rubrik Agent Cloud was in beta. Just a few weeks ago, we made Rubrik Agent Cloud generally available. And we have a number of POCs ongoing across early AI adopters as well as Fortune 500 companies. While we are still in the early innings of multiyear effort to scale our Rubrik Agent cloud suite, we believe that we are building the most consequential security and AI operations company for the AI era.”

Bipul on the 3 Key Takeaways

“First, Rubrik is winning the cyber resilience market across data and identity. Second, we have accelerated our business growth while the competition has stalled. And third, we are defining the enterprise AI market with our unique and differentiated agent control and guardrail solutions.”

On Rubrik’s Competitive Advantage over Legacy Vendors

“My belief is that the traditional cybersecurity companies, or people in those cybersecurity companies will not be suitable for this market because traditional cybersecurity is all about rule-based platform, and they’re not in the real-time control of action. This market is about dynamic control. And you need to bring an AI to control agentic actions. And AI requires model engineers. And most of the cybersecurity company, probably none of the cybersecurity company or these start-ups have any model engineering.

We brought Predibase to solve this problem. We believe we have a unique solution to control agentic action with AI to really drive intent-based understanding of action and stopping it.”

5. Concluding Thoughts

Rubrik delivered a strong Q4, outperforming estimates as expected. Revenue grew 46% YoY and 8% QoQ, a slight deceleration, but nonetheless very strong results.

Whether Rubrik can maintain these high growth rates will depend on the adoption of its new offerings such as Identity Resilience and Agent Cloud. It will take time for these to move the needle, but they do have the potential to be much larger contributors to revenue over the long term.

In the past 3-4 months, Rubrik stock has seen a ~50% drawdown following the impressive earnings beat in Q3. This can be attributed to 2 main reasons: firstly, the fear of software disruption that has wiped out trillions in market cap and secondly, the broader market drawdown in high-growth stocks amidst worries of stagflation and recent Iran-Israel-US conflict.

On the fear of software disruption, I’ve had my say in recent months on where I foresee this going. I believe there is a very real risk of replacement across hundreds to thousands of software businesses who provide non-mission critical software services. This does not include Rubrik.

In fact, Rubrik appears likely to benefit from the proliferation of AI, LLMs, and vibe coding. In an Agentic era, Rubrik’s services will be in greater demand. What gives me confidence, is that Rubrik is a founder-led, young business that is hungry for success. In my view, this is the key determinant in which a winner is to be picked for the coming decade.

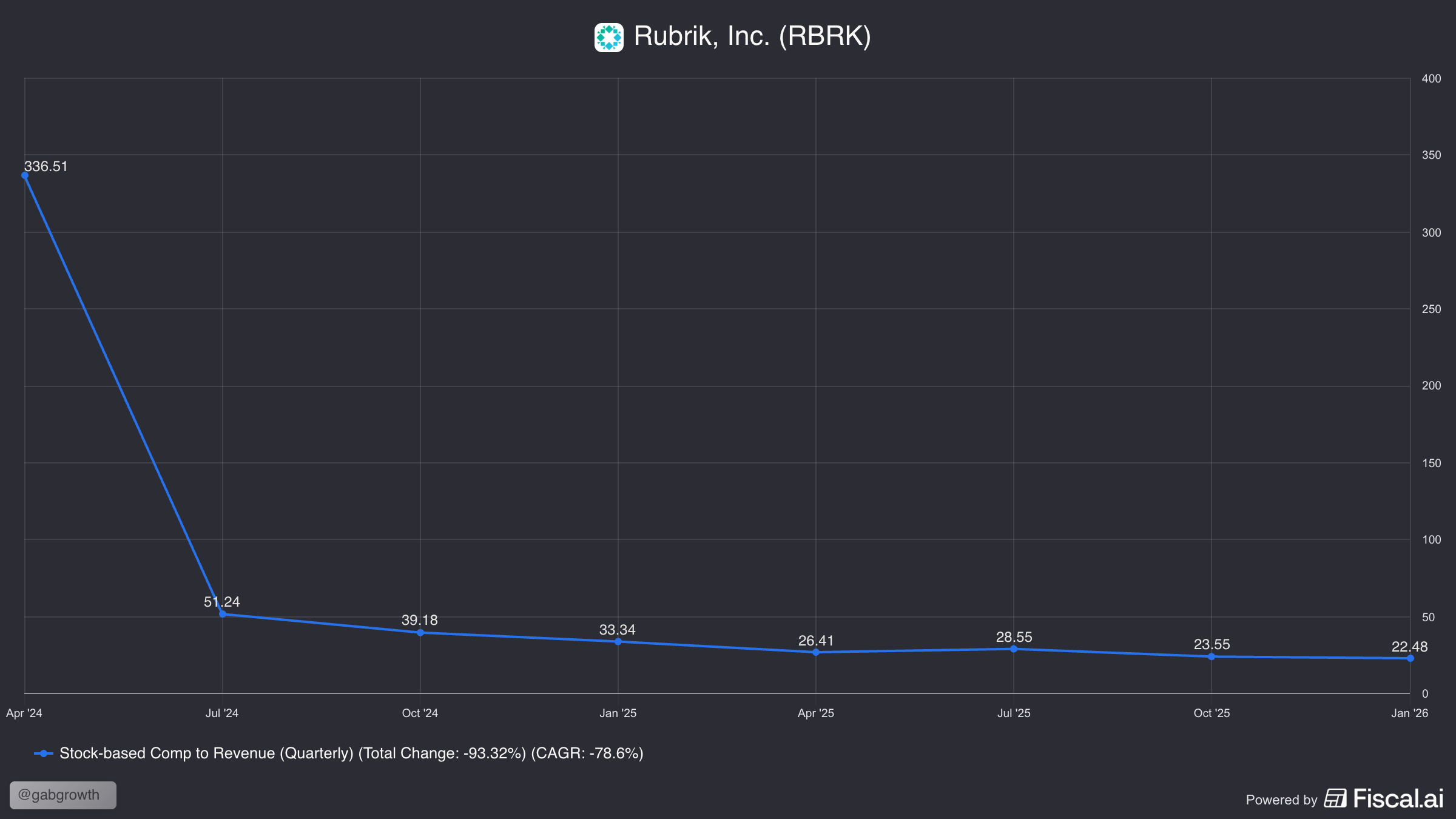

There are certainly risks to be had with regard to Rubrik. Firstly, stock-based compensation and the resulting share dilution is a real dampener on shareholder returns. That said, the pre-IPO compensation plans should come to a head by the end of the new fiscal year. While SBC remains 22% of revenue today, it has come down massively since IPO.

The second major risk in my view, is the ability for Rubrik to become a truly differentiated platform business in cybersecurity. Currently, it remains a backup-focused business. While their new products such as Identity Resilience and Agent Cloud are exciting, they still remain niche products and not a needle-mover.

The third major risk is the ability for these new products to support the growth trajectory that will inevitably falter as Rubrik takes a larger stake of the backup market.

At this point, it is clear to see that Rubrik is a market leader in this rather niche space. That means it is a big fish in a small pond. Now as it graduates into a larger pond, it will have to ensure it remains a big fish.

This quarter reinforces my confidence in the business. Bipul and Co. are clearly moving in the right direction. My thesis remains that Rubrik can be a massive player in multiple growing markets within cybersecurity. Despite fears by the market, cybersecurity remains rooted in a multi-decade tailwind and there is no other sector in SaaS that I would rather be invested in.

Thanks for reading!

- Gab

Paid Subscription Upgrade

If you’d like to support the work I do, consider becoming a paid subscriber. Your support will allow me to spend more time finding asymmetric opportunities in the market, writing and analysing various businesses.

Till the end of March, new paid subscribers will get 25% off the paid plan.

As a reminder, paid subscribers get access to:

Monthly Portfolio Updates (+98% in 2024, +26% in 2025)

Earnings Reviews on Portfolio Companies (SE, GRAB, DLO, MELI etc)

Archive of Deep Dives and Posts (13 Deep Dives and counting)

Southeast Asian coverage of industries and companies

Fiscal AI

Many of the charts I use are courtesy of Fiscal AI, which is in my view, the best platform for financial charting and market intelligence.

I have an affiliate link where you get access to a free 2-week pro trial and 15% off the pro plan.