Portfolio Review (June 2026)

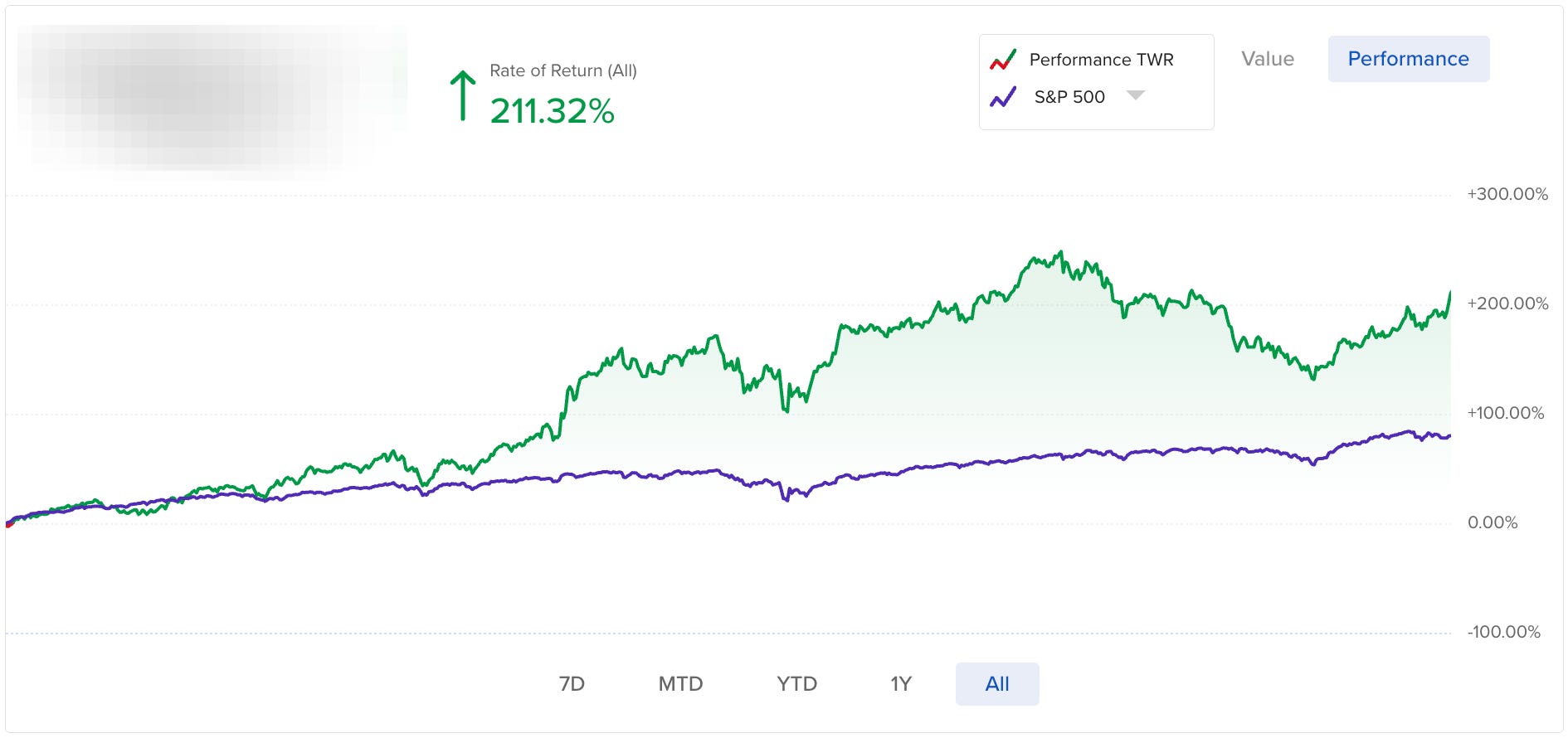

+211.32% Since Inception, +131.48% Outperformance

June 2026 Markets Review

S&P 500: -1.28%

NASDAQ: -0.26%

June was the first red month for the indexes since March. As we can see from the image above, it was largely led by a drawdown across the large-cap space, with MAG7 in particular leading the way. However, it was a mixed month, with many more advancers than decliners. For instance, the financials and healthcare space saw massive gains this month as capital rotated from technology.

Personally, I believe it is a very positive sign for the markets. After an incredible 3 month period of “up-only” action, a little breather and rotation is ideal. In May, the index was led by semis and tech with the MAG7 was up strongly, AAPL up 15%, TSLA up 14%, MSFT up 10%, with the real strength in the AI/Semi/Compute trade (AMD +45%, MU +87%, DELL +101%, QCOM +39%).

Interestingly, the memory players who have led the rally continued to do so this month with countless banks increasing their price targets as the market continues to price in a massive inflection in profitability for these businesses.

In my view, there were 3 main drivers:

Doubts around continued heavy CAPEX, worries about model progress due to Fable being blocked by the US government, and Chinese models catching up and outperforming on a cost-efficiency basis.

Conflict with Iran flared again, with fresh tension around the Strait of Hormuz keeping a risk premium in oil and a lid on sentiment, before easing into the final weekend as talks were floated.

There was certainly some quarter-end rebalancing happening with pensions and sovereign wealth funds mechanically trimming the names that had run hardest.

For the year, the indices remain comfortably positive even after the June wobble, with the Nasdaq still leading on the back of the first-half AI run.

The key here, is that this remains an earnings-driven advance, not a multiple-only one. These are the types of rallies that tend to lead much higher for longer.

Portfolio Performance (Since Inception)

(Portfolio Inception Date: 27th October 2023)

Portfolio: +211.32%

S&P 500: +79.84% (Outperformance: +131.48%)

NASDAQ: +109.04% (Outperformance: +102.28%)

Portfolio Performance (YTD)

Portfolio: +4.74%

S&P 500: +8.69% (Underperformance: -3.95%)

NASDAQ: +11.43% (Underperformance: -6.69%)

Personal Thoughts on the Market & Performance

It was a very mixed month for the market. I was publicly cautious, as I shared with subscribers in the lead up to the first Fed meeting by Kevin Warsh. We did get a drawdown in the early part of the month with uncertainty going into it.

However, as predicted, Kevin Warsh led the Federal Open Market Committee (FOMC) to leave benchmark interest rates unchanged in a range of 3.5% to 3.75%. Despite pressures to lower rates, the committee noted that elevated inflation necessitated a steady hand, with some officials projecting a rate hike later in the year.

My personal view is that rates are likely to stay at this range for a long time, and it would be unwise to consider rate hikes. I am leaning towards 1 rate cut around the end of the year as the Iran war fades and prices stabilise. It is not talked about much that oil is currently trading at just $72, down about 35% in just 2 months from $111 in early May.

I believe this has also led to the general uptick in emerging market stocks as markets breathe a sigh of relief that the war is coming to an end. As we discussed in the last portfolio review, many emerging markets, especially in Southeast Asia are huge oil importers, which is of course a major input for many of their products and services.

I am slightly concerned about the market as the index on a YTD basis has been driven by a narrow set of names: MU (+304%), AMD (+171%), INTC (+278%), MRVL (+250%), SNDK (+857%), DELL (242%).

The MAG7 has generally been a mixed bag with MSFT performing poorly at -23% YTD and GOOGL the best performer at +14%. This is especially surprising as the MAG7, hyperscalers in particular have their hands in every corner of AI.

I read a very interesting piece just yesterday that I am still trying to think through more carefully. Generally, I do agree with many points and I will share it here:

I might publish a longer-form article to discuss my thoughts on who I believe will be the long-term beneficiaries of AI.

I remain optimistic for the rest of the year, but with caution on certain pockets of market. For instance, memory. While I understand that there is a massive bottleneck which will enable them to earn excess profits in the short to medium term, here is my belief:

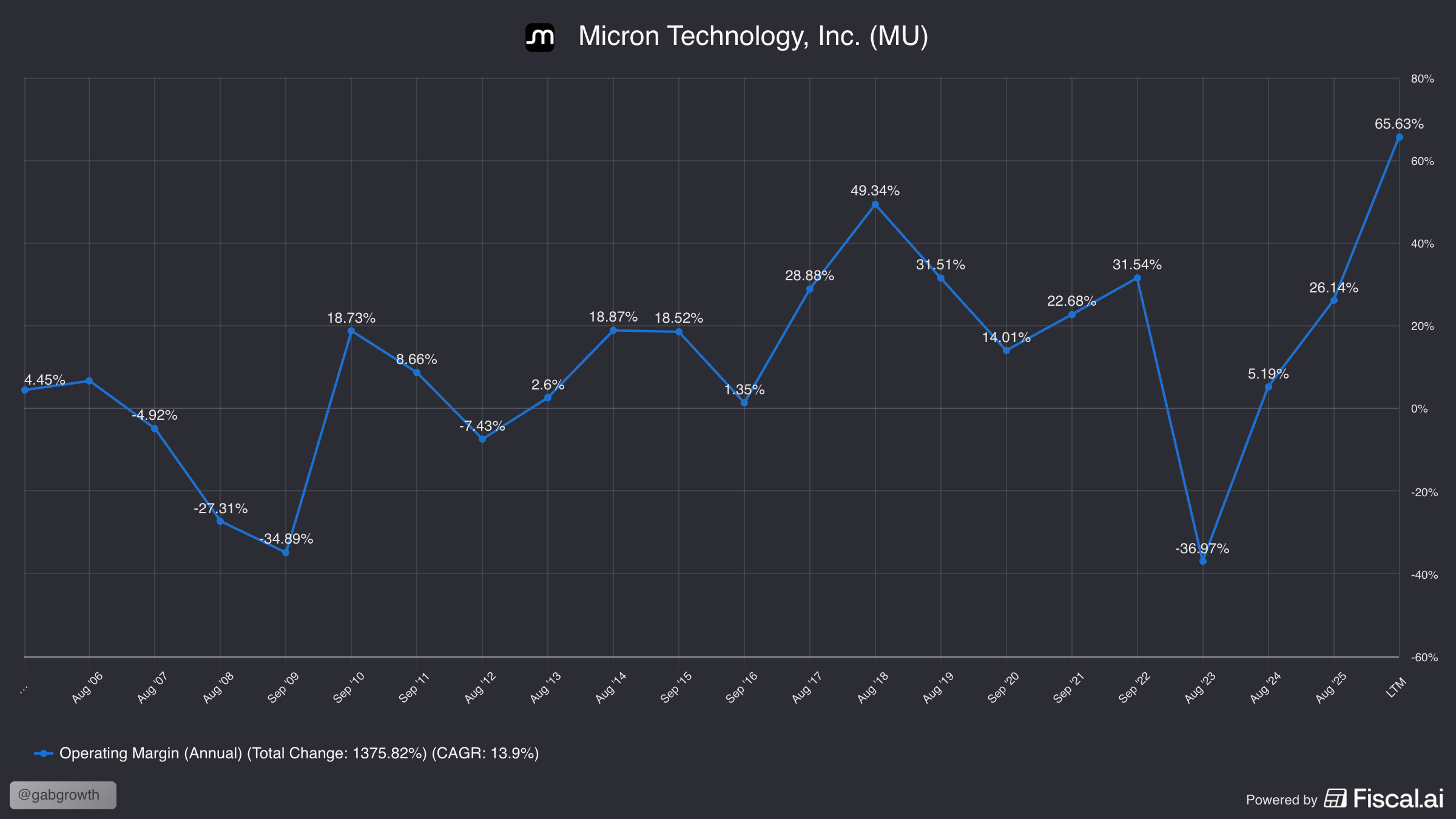

In the past few quarters, Micron’s gross margins have grown from ~40% to 86% in the latest quarter. They have gone from an unprofitable business to a wildly profitable one which will the 3rd most profitable US company next year, only behind Nvidia and Google, within just 1 year.

This is not exactly new, Micron and memory at large is a cyclical business, we saw that in 2010. It is even clearer when we look at operating margins.

To bet that Micron will continue to earn these supernormal profits is to assume that the hyperscalers, who are footing the bill, and the broader AI industry that depends on HBM will do nothing for the next 5 years to solve this bottleneck. I am highly doubtful.

We have already seen hyperscalers take a hit as their ROIC drops massively over CAPEX concerns. If ROIC continues to be weak, would we see hyperscalers continually pouring in money to memory? Would they continue to fund this bottleneck?

To this point, we have also seen two very interesting things happen last week. Apple raised prices on multiple products (iPad, Macbook etc) due to rising memory costs. Microsoft also did the same with the Xbox. Now the interesting part is that these are not their core products, especially in the case of the Xbox. So why would they do this, and publicise it at such a time? I believe it is to let it be known to consumers and thereby the government that these bottlenecks will have a huge impact down the value chain.

We saw further evidence as Apple was reportedly lobbying the government to buy DRAM from CXMT that is currently blacklisted. They might not necessarily be successful in their efforts, but it shows they are clearly attempting to do something about it, and not sitting idly by and paying increased prices.

Price gouging is never a sustainable tactic, especially when memory players will be relying on hyperscalers for years to come. It is clear that the relationship between both parties are not the best, and I would not bet that these high memory prices continue for the next couple of years.

July

July has been one of the strongest seasonal months.

Under Trump, July has been positive (5 for 5), and up 2.9% on average.

I am cautiously optimistic for this month and have plans to add to multiple positions with the cash in hand, I will detail those positions below.