Manchester United (Deep Dive)

Before we start, I must preface that this is a very different business from the type that is typically covered on this Substack.

I’m covering a football club (soccer, if you’re from the U.S.), more specifically, Manchester United Football Club, a storied English football club and global sports brand. The club claims to have a global following of over 1.1 billion people, which would equate to about 13% of the population.

The club is publicly traded and listed on the New York Stock Exchange as MANU, with an estimated market capitalisation of $3.86B.

This deep dive will provide a comprehensive investment analysis of Manchester United. We will cover the company’s history, business model, competitive positioning, financial performance, management and governance, valuation and more.

P.S. I am a fan of Manchester United Football Club (yes unfortunately, as you will come to see if you aren’t familiar with the happenings in the past decade), but rest assured, this will be an unbiased deep dive.

Table of Contents

Company/Club History

Business Model

Commercial

Matchday

Broadcasting

Competitive Positioning and Moat

Financials

Ownership and Management

Valuation

Bull and Bear Case

Concluding Thoughts (What I'm personally doing)

1. Company/Club History

Early Beginnings (1878-1902)

Manchester United, commonly known as United (and how I will refer to it for the rest of this article), traces its origins back to 1878 when it was founded as Newton Heath L&YR Football Club by workers from the Carriage and Wagon department of the Lancashire and Yorkshire Railway depot in Newton Heath.

In its early years, the team played matches against other railway departments and companies. Their first recorded game took place on 20 November 1880, when they donned the railway company’s green and gold colours, losing 6-0 to Bolton Wanderers’ reserve side.

By 1888, Newton Heath became one of the founding members of The Combination, a regional football league. After the league folded a year later, the club joined the newly established Football Alliance, which lasted three seasons before merging with The Football League. This merger placed Newton Heath in the First Division for the 1892-93 season, by which time it had separated from the railway company and dropped “LYR” from its name. Two seasons later, the club was relegated to the Second Division.

Renaming and the first 40 years (1902-1945)

Shortly after in 1902, with debts of £2,670 (equivalent to £370,000 today), the club was served with a winding-up order. The captain of the team at the time, Harry Stafford, found four local businessman who were each willing to invest £500 in return for a direct interest in running the club. As part of the deal, they changed the name of the club, and on 24 April 1902, Manchester United was officially born.

Manchester United saw relative early success, finishing 2nd in the Second Division and being promoted to the First Division in 1906, and subsequently winning the First Division in 1908.

In 1910, it moved to the iconic Old Trafford stadium where a rich tradition was to be built by legendary managers like Sir Matt Busby and Sir Alex Ferguson.

In this period, United saw some success but was not considered a leading club in the country. That was to change in 1945 when United appointed Matt Busby to be the manager of the football club.

The Busby Years (1945-1969)

In October 1945, World War II had just ended, and football was set to resume. United hired Matt Busby, who interestingly was a player for 2 of United’s biggest rivals: Manchester City and Liverpool.

Busby demanded an unprecedented level of control over team selection, player transfers and training sessions. That control led to a team built in his image, where they finished 2nd in the league in 1947/48/49, and an FA Cup (the most prestigious cup competition in England) victory in 1948.

In 1952, the club won the First Division league title for the first time in 41 years, and then back to back titles in 1956 and 1957. The squad was incredibly young and was full of potential, with an average age of 22, fondly nicknamed “the Busby Babes” by the media, a testament to Busby’s faith in his young players.

In 1957, Manchester United became the first English team to compete in the European Cup, despite objections from The Football League, who had denied Chelsea the same opportunity the previous season.

1958 was to be a season that every United fan would never forget. On the way home from a European Cup quarter-final victory against the Serbian champions, Red Star Belgrade, the aircraft carrying the Manchester United players, staff, officials and journalists, crashed while attempting to take off after refuelling in Munich, Germany.

This was known as the Munich Air Disaster, which claimed 23 lives, including those of eight players and injured several more, some of which were never able to play football again.

Matt Busby was spared, but seriously injured and left with a depleted squad. However, he was determined to rebuild the team through the 1960s. He signed a few experienced players like Denis Law and Paddy Crerand, who combined with the next generation of youth players like George Best, helped them to win the FA Cup in 1963.

United won the league title again in 1965 and 1967, and finally became the first English club to win the European Cup, beating Benfica 4-1 in the final. Matt Busby had finally delivered the trophy 10 years after the fatal Munich crash. He resigned as manager the year later and was replaced by the reserve team coach.

Mediocrity (1969-1986)

After Matt Busby’s resignation, United went through a flurry of managers (even persuading Busby to come back temporarily). However, they never performed quite as well and were even relegated to the second division for a season.

They had moments of brilliance, from winning the FA Cup in 1977, 1983 and 1985, but the period was relatively mediocre by Manchester United’s high standards.

Fans were desperate for a league title again after going through nearly 20 years of not winning it. That was about to come from the appointment of the next legendary manager in charge of the club.

The Fergie Years (1986-2013)

With United desperate to go back to winning ways, they hired Alex Ferguson who arrived from Aberdeen, having won the European Cup Winners’ Cup against Spanish giants Real Madrid. He also broke the duopoly in Scotland of Celtic and Rangers and was highly regarded.

Ferguson’s career at United started on a mediocre note with a 2nd place finish in his 2nd year sandwiched by two 11th place finishes. He was on the verge of being sacked before his job was saved by victory over Crystal Palace in the 1990 FA Cup final. The following season, Manchester United won their first UEFA Cup Winners’ Cup title.

Ferguson was a strict disciplinarian and took charge of all aspects of the club. He built the club in his image and famously fielded many academy prospects, balancing the team out with some experienced players. The likes of David Beckham, Ryan Giggs, Paul Scholes, Gary and Phil Neville came through in the early 1990s.

In 1992, the Premier League was founded, replacing the old English Division, where United won their first league title since Sir Matt Busby left in 1967. A year later, they won a 2nd title alongside the FA Cup to complete the first “Double” in United’s history.

In 1999, United became the first team to win the Premier League, FA Cup and Champions League in the same season, nicknamed “The Treble” and Ferguson received a knighthood that summer for his services.

At the turn of the year, United continued to dominate, with Ferguson constantly refreshing his team, bringing in fresh young talent to bolster the squad. In 2003, Ferguson purchased a young Cristiano Ronaldo from Sporting Lisbon in Portugal. He would go on to have one of the most amazing careers of any footballer in history (he is still playing now!).

A pivotal change occurred in 2005, when American businessman Malcolm Glazer acquired control in a £790 million leveraged buyout. The takeover loaded the club with debt and was met with intense fan opposition. The Glazer family’s ownership period saw continued on-pitch success in the late 2000s, but also rising debt and fan unrest over financial management. In 2012, Manchester United made a return to public markets with an IPO on the New York Stock Exchange, raising ~$100 million.

The IPO was partly aimed at paying down debt (which stood at over £420 million in 2012).

In 2013, after 26 years at the club, Ferguson made the decision to retire at age 71.

During his 26 years at Manchester United, Ferguson won 38 trophies, including 13 Premier League titles, 5 FA Cups and 2 Champions League titles.

Ferguson has written several books, including 3 autobiographies, with his latest book “Leading” co-written with Sequoia chairperson Michael Moritz, a billionaire Venture Capitalist that I’m sure most investors are aware of.

Post-Fergie Years (2013 - Now)

Since Ferguson’s retirement, United have again gone through a whole host of managers, each attempting to bring the club back to its glory days.

Great managers have come and gone: Jose Mourinho, Louis van Gaal, Erik ten Hag. All of whom had success away from the club but failed to achieve the league title with the club.

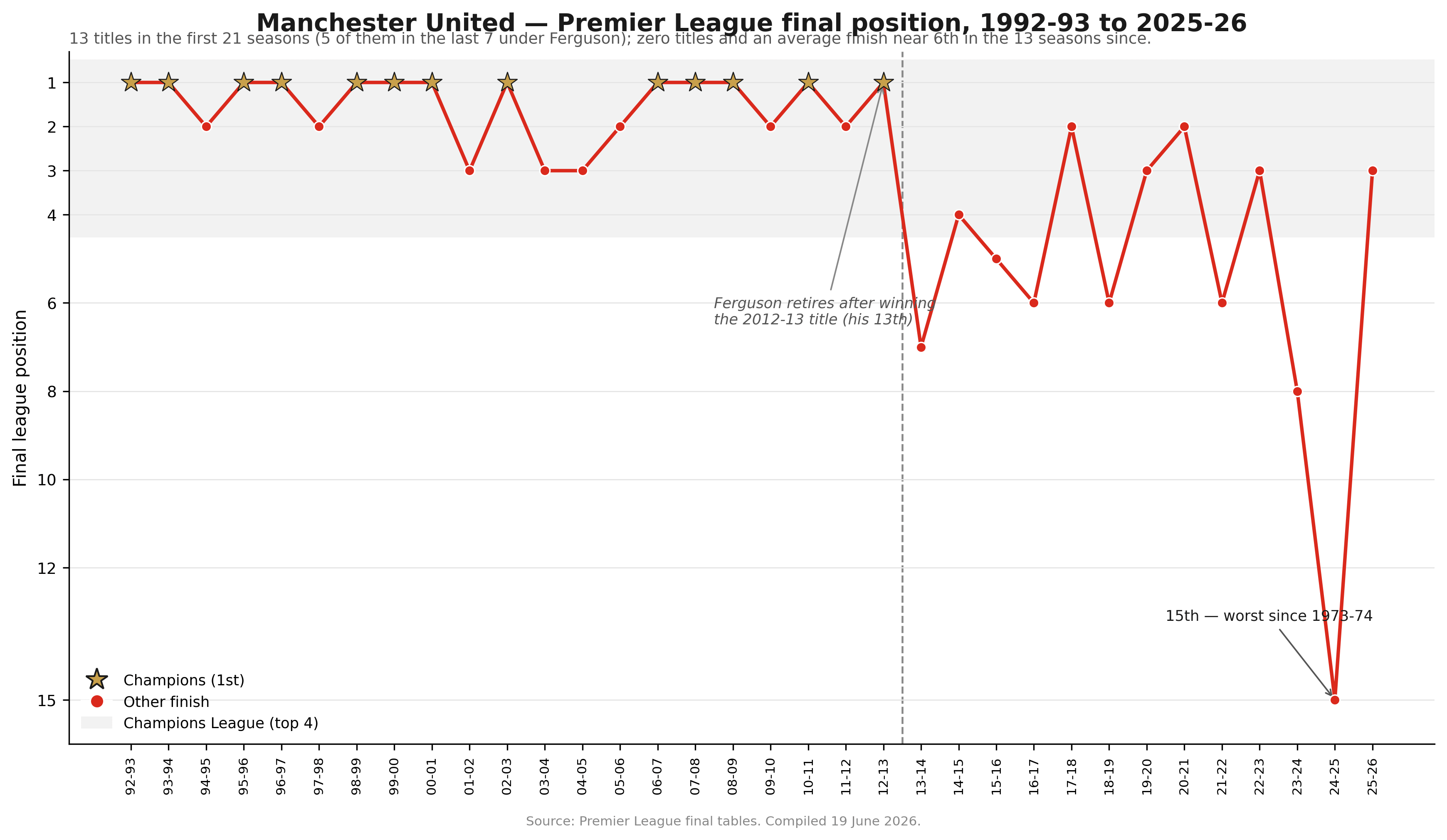

The drop-off in football success can be summed up in the picture above. However, the club has remained a commercial powerhouse. In November 2022, they announced a strategic review that opened the door to a potential sale of the club. This culminated in February 2024 with British billionaire Sir Jim Ratcliffe (founder of INEOS) acquiring a 25% minority stake for ~$1.25 billion.

The deal, valuing the club’s equity around $5 billion, included Ratcliffe investing an additional $300 million into club facilities and taking charge of football operations. The Glazers remain majority owners, but Ratcliffe’s investment marks the first significant ownership change in nearly two decades.

Since Ratcliffe’s entry into the cap table and him taking charge of football operations, not all has been smooth sailing. United have had 3 managers, with Erik Ten Hag first sacked in September 2025. Ruben Amorim, who had much success in the Portuguese League, was appointed but ultimately sacked too in January this year. Michael Carrick, an ex-player of Manchester United took the reins on a temporary basis. Since taking over at United, he has managed 17 games, won 11, drawn 3 and lost 2. This is a 70.6% win-rate, which is an incredible feat. The club rewarded him with a 2 year contract at the end of the season.

2. Business Model

Manchester United has three revenue streams. In FY2025, total revenue hit a record £666.5M ($858M).

This was split into 3 segments: Commercial (50%), Matchday (24%) and Broadcasting (26%).

Commercial is sticky and brand-driven, which tends to grow regardless of how the club does from year to year. That said, of course this trends upwards at a quicker trajectory when the team is more successful, thereby attracting more fans and sponsors.

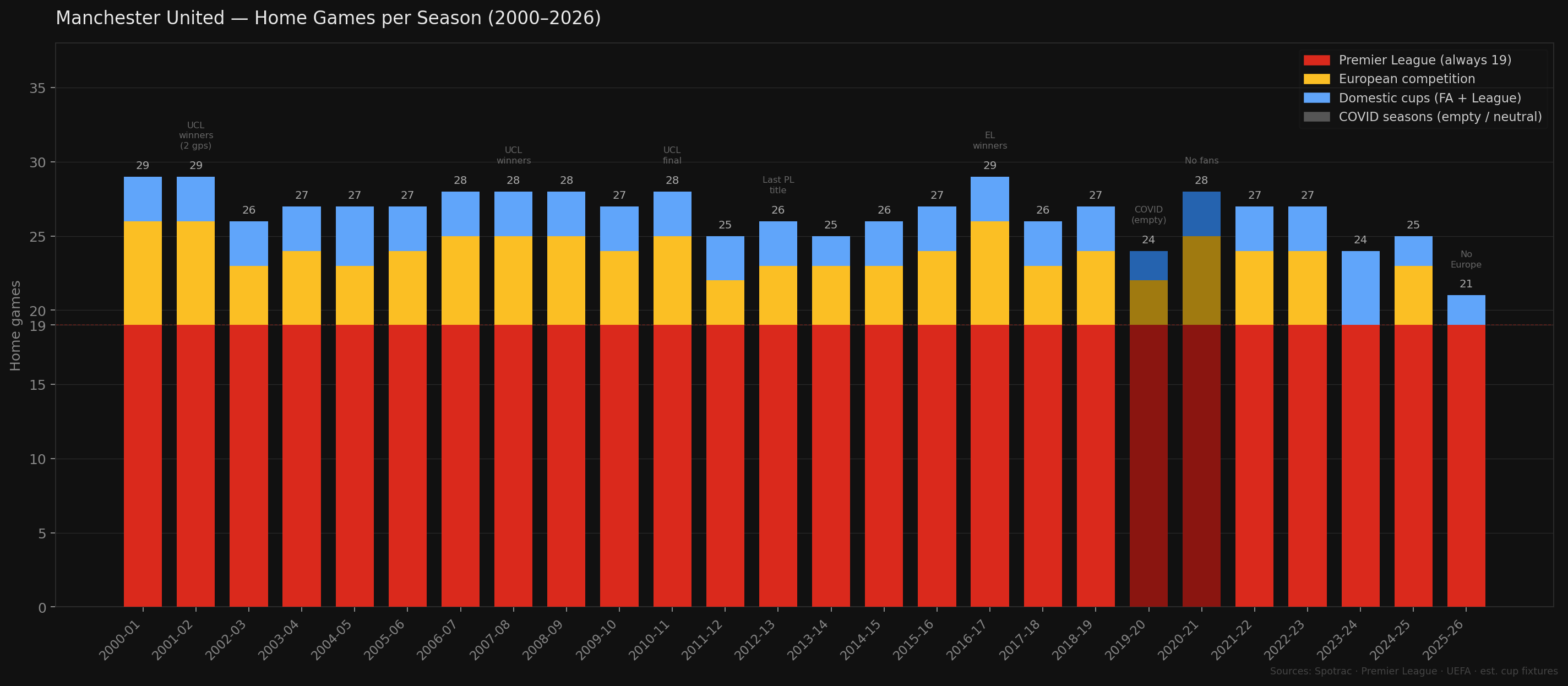

Matchday is structurally capped at Old Trafford’s 74,879 capacity, which has not changed since 2006. That said, this is affected by the number of games played in each season, which varies depending on how well the club does the previous season, as well as in the current season’s tournaments. For instance, the team did poorly this season, exiting the FA Cup and League Cup early on, resulting in a total of just 40 games played this season, a record low in 111 years. This will weigh on Matchday revenue.

Broadcasting is performance-linked and typically collapses if the club misses out on the Champions League (the most prestigious club competition in Europe).

Revenue Trajectory

Revenue has steadily grown in the past 5 years despite the team finishing outside of the top 4 places (which would have granted Champions League) multiple times. This is generally due to the Commercial moat in action where losses in Broadcasting and Matchday have been supported by the brands and sponsors associated with the club.

2a. Commercial

This is Manchester United’s genuine competitive advantage. At £333M, commercial revenue is larger than the total annual revenue of most Premier League clubs. It is also the segment most visibly detached from on-pitch performance. (e.g., it grew 10% in FY 2025 despite the team having its worst season ever in the Premier League era)

The commercial revenue bucket can be segmented into 3 sub-categories: sponsorships, retail/merchandising/licensing, and hospitality.

Sponsorships: Kit Deal

In terms of sponsorships, the main money maker is typically the kit deal, where most clubs sign with a major sports brand such as Adidas or Nike. In July 2023, Manchester United signed a 10-year extension with Adidas valued at a minimum of £900M, or roughly £90M/year, which was one of the largest kit deals in sport.

There is a notable clause in here where the club pays Adidas a £10M penalty for every season in which it fails to qualify for Champions League football. This is a direct financial cost of on-pitch underperformance, and it has already been triggered for FY2026.

Sponsorships: Shirt Sponsor

The second highest revenue generator is typically the front of shirt sponsor. In 2024, Qualcomm's Snapdragon brand replaced TeamViewer as the front-of-shirt sponsor in what was described as the largest shirt sponsorship deal in world football, £60M per year. For context, Liverpool's shirt deal with Standard Chartered runs at approximately £50M/year. Arsenal's Emirates deal is around £40M/year. United are currently pricing their shirt at a 20-50% premium to direct peers, a reflection of genuine brand demand and the depth of the global fanbase.

Sponsorships: Training Kit Sponsor + Regional/Global Partners

There are of course, many other types of sponsorships. United have 70+ active commercial partnerships spanning 20+ countries. There is also a regional deal structure which allows lower-tier sponsors to pay for rights in specific markets (Indonesia, China, India, US) without paying global rates, widening the commercial funnel.

They also recently announced a new training kit sponsor: Betway for a reported £20M annually, which stands as one of the most highly valued single-partner training kit deals in global football.

Retail & Licensing

A critical but under-appreciated element of the commercial segment is that United brought their e-commerce operation in-house in FY2025, ending a third-party arrangement. This shift is expected to add a material uplift to retail margins in FY2026 and beyond where the club now captures the full economics of online kit sales, replica merchandise, and apparel, rather than sharing margin with a third party.

2b. Matchday

Matchday revenue is the money United makes from Old Trafford. This includes tickets, season tickets, hospitality, executive boxes, food and beverage, parking, programmes, museum revenue, memberships, domestic cup gate receipts and other events hosted at the stadium.

This part of the business is purely physical and capacity-constrained. Unlike commercial revenue, which can scale globally, Matchday revenue depends on how many home games United play, how large the stadium is, and how much the club can charge per fan.

As a result, this business is driven by four main things: the number of home games, the size of Old Trafford, attendance levels, and ticket/hospitality pricing. United usually starts with 19 Premier League home games, then adds more if the team progresses in domestic cups or European competitions.

In my view, this is a strong, but under-optimised revenue stream. Old Trafford demand is clearly there. United has averaged over 99% attendance for Premier League home matches for every season since 1997/98. This is extremely rare.

However, Old Trafford is ageing and the stadium that was built in 1910 and extensively redeveloped through the 1990s under Ferguson now requires substantial maintenance investment just to remain operational. Multiple sections have required structural attention, and the Matchday experience has fallen behind newer grounds like Tottenham Hotspur Stadium and the rebuilt Anfield.

For comparison, the club generates approximately £2,100 of Matchday revenue per seat per season while Tottenham's stadium generates approximately £2,600 per seat. This does not seem like a massive difference, but (1) it adds up across tens of thousands of seats across multiple seasons, (2) United is a much bigger club than Tottenham and should realistically be making 2x or more per seat.

The New Stadium Plan

In March 2025, United announced plans for a new 100,000-seat stadium adjacent to the current Old Trafford site that is estimated to cost about £2B. It is positioned as the centrepiece of a broader Old Trafford regeneration project covering 370 acres of Greater Manchester. Moving from 74,879 to 100,000 seats is a ~33% capacity increase. At United's current Matchday yield of roughly £2,140/seat/season, that alone adds ~£53M annually.

On 23rd June 2026, United announced that they had acquired a 25-acre site sufficient for their new stadium that is located just 350m away from Old Trafford.

2c. Broadcasting

Broadcasting revenue is the money United receives from media rights. This includes distributions from the Premier League, UEFA competitions and other broadcast-related content such as MUTV. Unlike Commercial revenue, this is less directly controlled by United because Premier League and UEFA media rights are negotiated collectively, not individually by the club.

This revenue stream is highly sensitive to on-pitch performance. The better United performs in the Premier League, the better its league distributions. More importantly, qualifying for the Champions League creates additional UEFA broadcasting and prize money. Missing out on Europe, or playing in the Europa League instead of the Champions League hurts revenue.

Premier League Distributions

All 20 Premier League clubs receive a baseline equal share of roughly £60-70M annually from the current domestic and international rights cycle. United receive additional "merit payments" based on final league position, and additional "facility fees" based on the number of times their matches are selected for live broadcast, which historically is the highest of any club due to their global audience numbers.

Champions League Sensitivity

This is where the on-pitch failure costs real money. Champions League participation generates a floor of approximately £30-40M from UEFA distributions for a group-stage participant, with material upside (£100M+) for deep runs to the knockout stages.

In FY2026, United have no UEFA competition, which creates a £30-40M direct revenue hole. On top of the direct UEFA money, the Adidas penalty clause costs a further £10M. There are also some indirect impacts such as negotiating better rates with commercial partners when UCL football is on the table, and some sponsor clauses explicitly provide uplift for Champions League participation.

Broadcasting is a powerful but volatile revenue stream. United benefits from being in the Premier League, the most valuable football league in the world, but this part of the business is still tied closely to football performance.

Overall

The key point is that Manchester United’s business model is unusually brand-heavy.

Most football clubs are heavily dependent on broadcasting and sporting success. United is different because Commercial revenue alone is half the business. That means the club’s value is not purely tied to whether it wins this season. Its real asset is the Manchester United brand, with the history, the fanbase, the shirt, the stadium, and the global attention that comes with it.

3. Competitive Positioning and Moat

Competitive Positioning

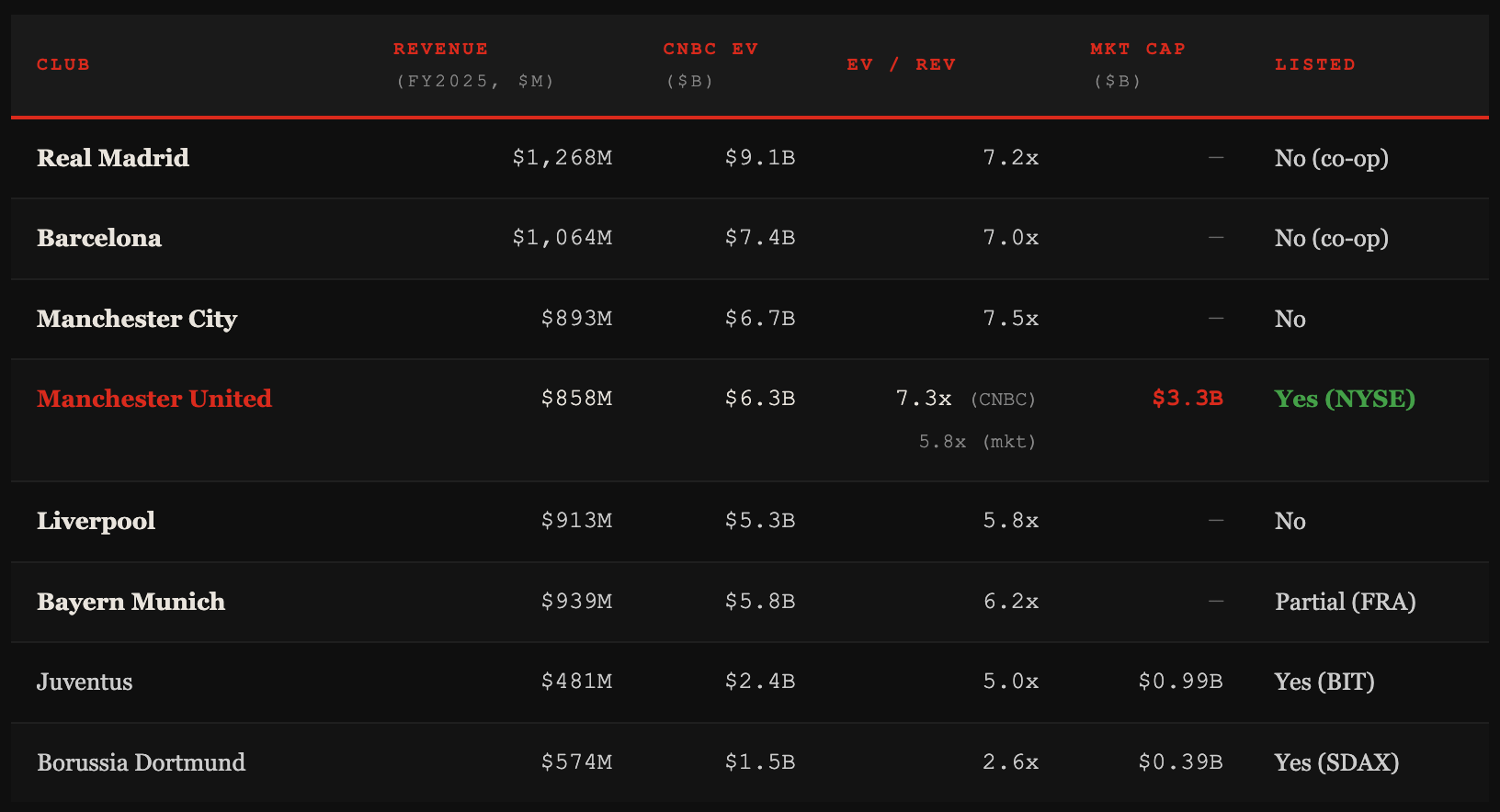

Most of these clubs are privately held and never transact publicly, which makes valuation a guessing game. The most widely cited independent attempt to appraise these clubs is CNBC’s annual Soccer Team Valuations. Their methodology blends revenue multiples (anchored to comparable sports franchise transactions in the NFL, NBA, and European football), brand premiums derived from commercial data, stadium asset values, and forward revenue projections.

Despite limited success in the past decade and a half, United remains one of the most valuable football clubs in the world. The two runaway leaders remain the Spanish giants (with Cristiano Ronaldo and Lionel Messi being the face of their success in the past 2 decades).

Within English Football, Man City and Liverpool provide the clearest competition, with City having won five of the last seven Premier League titles and Liverpool being the 2nd most popular English club in the world and most successful English club in terms of trophies won.

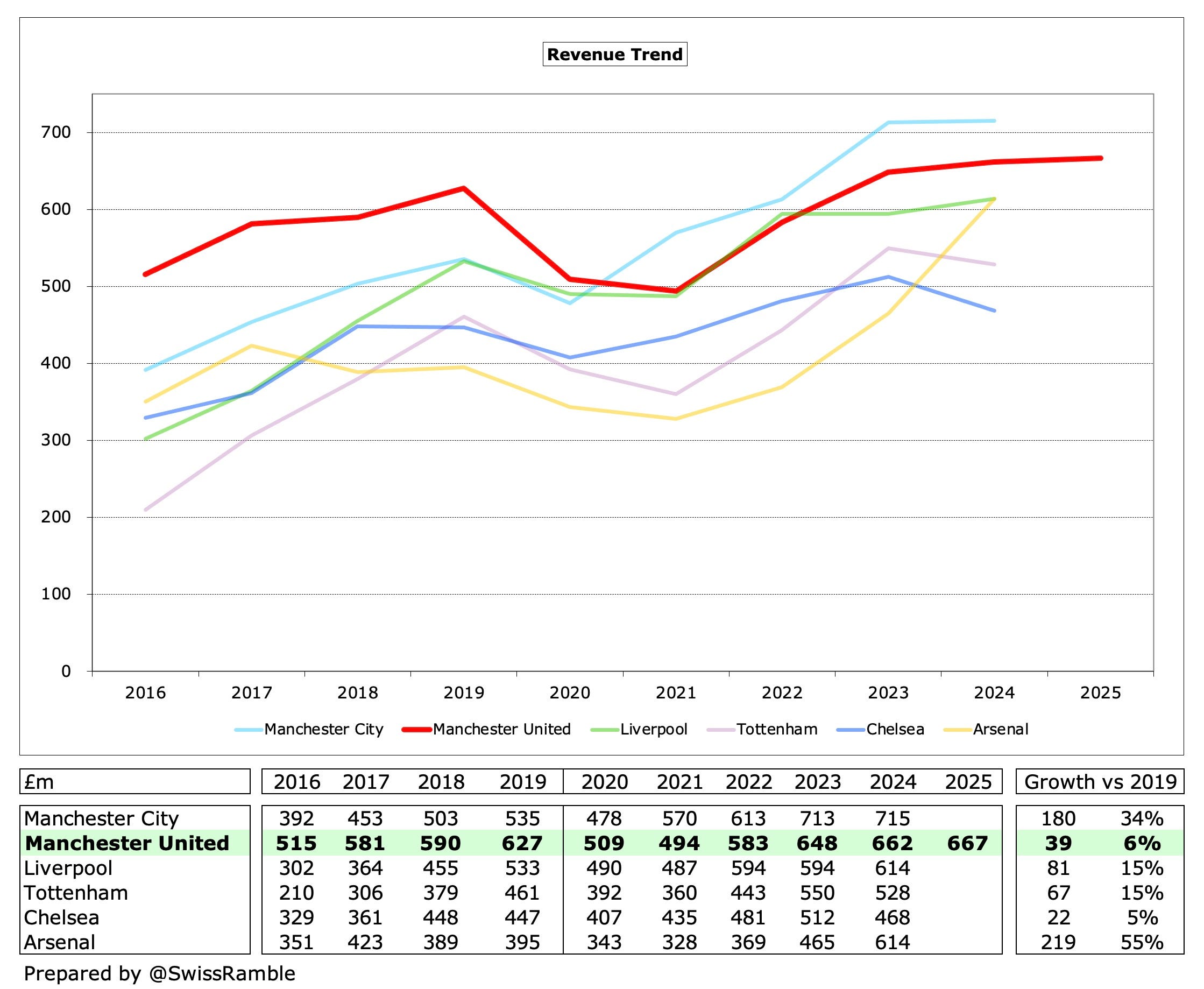

This excellent chart from Swiss Ramble gives the clearest view of how poorly United have done in comparison to rivals. In 2016, just 10 years ago, they were by far and away the largest revenue generating club in English football. Since 2019, they have only grown revenues by 6% compared to Man City and Arsenal who have grown at 34% and 55% respectively.

Moat

United’s largest moat is in its commercial strength which is rooted in history and geography. I believe there are 3 key factors that explain why there are very few European clubs that have built a comparable commercial machine.

Firstly, the history of the club. United was the first ever English club to appear in a European competition, and also the first to win the European Cup (equivalent to the Champions League today, the grandest club competition in the world). The circumstances around it are what makes it truly special. The Munich Air Disaster, as discussed earlier, was a watershed moment in the history of the club. A group of extremely talented young footballers lost their lives, a few of whom were tipped to be future superstars. In a single moment, United lost not only a team, but possibly a dynasty.

Sir Matt Busby, the manager, survived, recovered and rebuilt the club. Bobby Charlton, who also survived the crash, became the emotional bridge between the lost Busby Babes and the new United team. Ten years later, in 1968, Manchester United won the European Cup with Busby as manager and Charlton as captain. Munich became central to United’s identity and gave the club a deeper mythology around it.

During the Ferguson-era of 1993 and 2013, United won 12 Premier League titles and two Champions Leagues in an era when the Premier League was simultaneously becoming the world's most-watched domestic football league. United were the face of that export, building fanbases across Asia, North America and Africa, during a period when no other club at their level consistently.

It is also very notable that United have had several players who have extremely strong marketability and have been the face of football for years at their peak. This is an extremely underrated factor, many fans support a club because of the player they follow, not the other way around. For instance, United have had George Best, David Beckham, Wayne Rooney and Cristiano Ronaldo play for the club. These are some of the greatest and most popular players of all time.

Secondly, English-language content advantage. As a UK club whose matches are broadcast in English, United benefit disproportionately in the world's largest football markets outside Europe (India, Southeast Asia, the US) where English-language content has structural advantages in media licensing and fan engagement. The clearest example is the gulf in revenues between the English league and other top European leagues. 9 of the top 20 revenue-generating clubs in the world are English clubs, showing the dominance of the league. The EPL makes up ~40% of the top 5 European leagues revenues combined.

Thirdly, sponsorships and partnerships. United pioneered the commercial model of selling tiered regional rights where a sponsor in Indonesia gets to claim it is the "Official Financial Partner of Manchester United in Southeast Asia" and pays accordingly, without displacing global sponsors. This multiplicative structure generates revenue from the same asset simultaneously across dozens of markets. No club has replicated it at scale. Of course, this is all possible because of the history and brand of the club. Sponsors are paying for access to a massive global fanbase.

4. Financials

Overview

United’s financial year begins on 1st July and ends on 30th June, mirroring the English and European football league schedule.

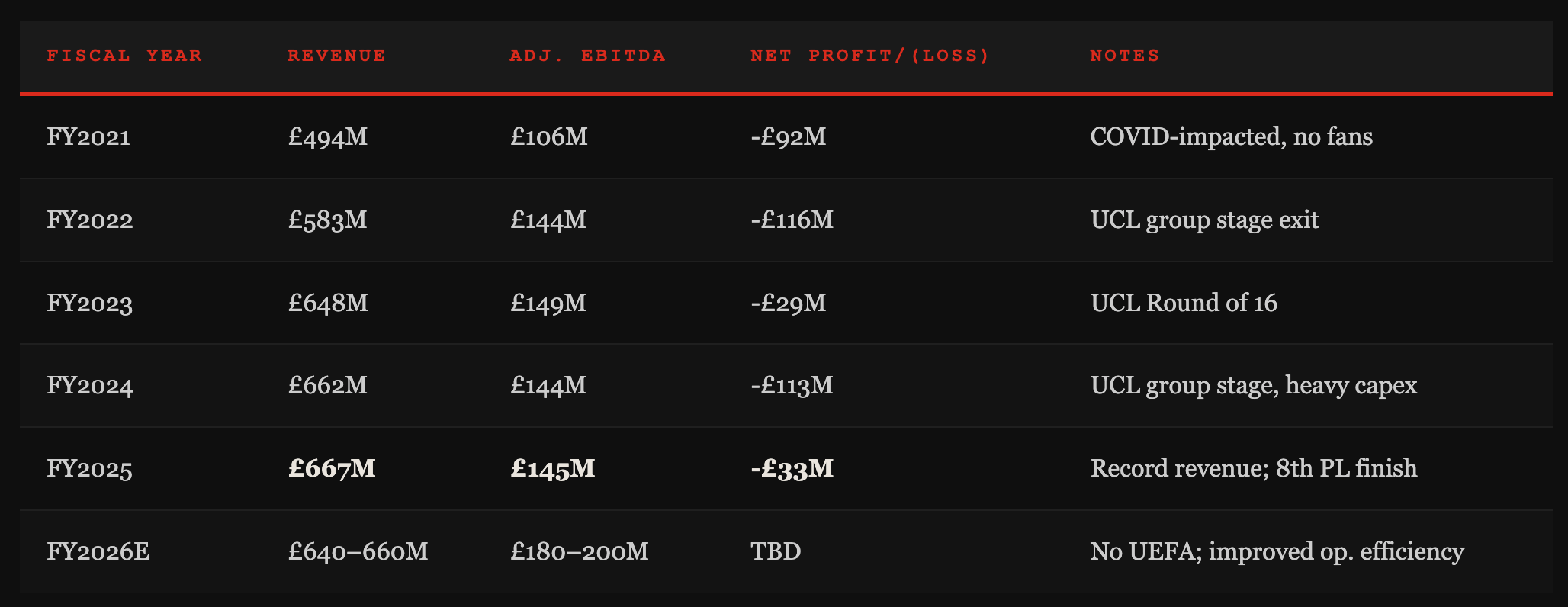

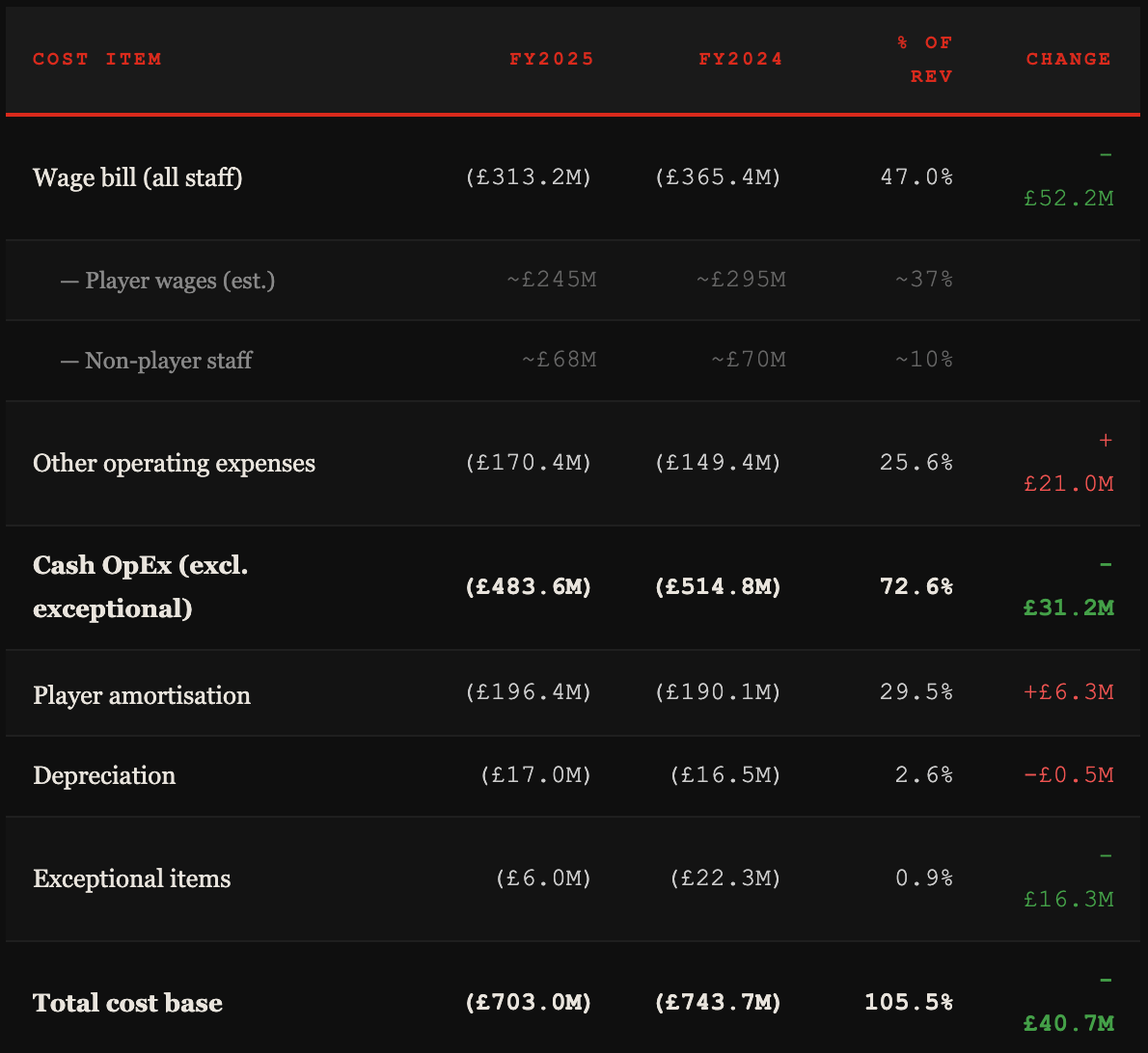

Total revenue grew very marginally from FY2024 to FY2025, with increases in Commercial and Matchday revenue negated by a drop in Broadcasting revenue. However, net losses narrowed massively from £113M to £33M, with a £52M wage bill reduction and a £16M reduction in exceptional items being the key drivers.

FY2026 will likely see a slowdown in Matchday and Broadcasting revenue due to the team’s failures in the league and various cup competitions in the 2025-2026 season. However, I do expect FY2027 to be much stronger, due to the team’s recent 3rd place finish in the league, which will mean Champions League next season. As we have discussed previously, this will mean higher Commercial, Matchday and Broadcasting revenue.

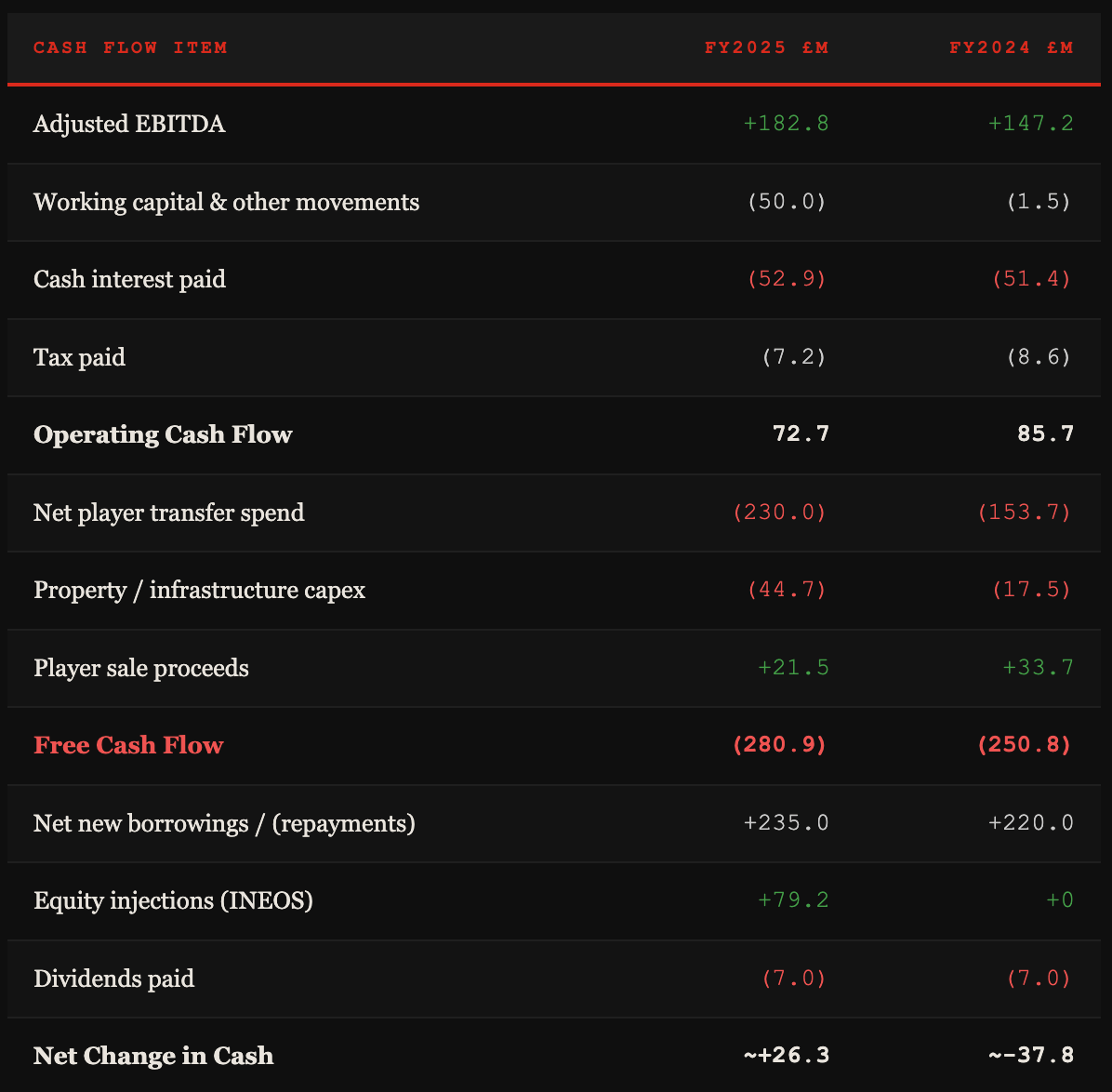

From a quick look, Adjusted EBITDA of £182.8M sounds healthy (~27.4% EBITDA margin). However, the club still lost £33M after tax. Why was that?

Something to note about football clubs is that one of the largest cost items from a P&L perspective is player amortisation. This is because players are capitalised as intangible assets and amortised based on contract length. For instance, Manchester United buys a player for £50M on a five-year contract. They would amortise the player at £10M/year. The £196.4M in amortisation does not represent cash going out the door this year, but the accounting spread of prior-year(s) transfer fees. This explains the huge discrepancy between the P&L loss (£33M) and the free cash flow loss (£281M).

The other huge item on the list is of course net interest expense. This is the price of the Glazer LBO which we will discuss in detail later.

Revenues

There are 3 key observations from this table.

Commercial compounds regardless of results, from £232M in FY2021 to £333M in FY2025, a 43% increase over four years and a CAGR of ~9.5%. As we have discussed, there are multiple drivers here such as the Snapdragon shirt deal (£60M/yr, record in world football), the Adidas extension (up to £90M/yr), and the in-house e-commerce transition.

Matchday has recovered strongly post-COVID, but is now hitting a structural ceiling. Old Trafford's 74,879 capacity is essentially full every home game. Without the new stadium, meaningful Matchday growth from here is difficult. FY2026 will probably be slightly lower due to fewer home matches (out of FA Cup, League Cup early and no European football).

Broadcasting is the most volatile factor, as we have already discussed. These fluctuate wildly according to United’s competitive success. FY2025 and FY2026 are very weak years due to the lack of Champions League participation, but we should see it at £220M+ in FY2027. This £50M+ swing is the single largest lever in the P&L.

Costs

The wage bill is the single most important cost in the club, making up ~47% of revenues in FY2025, which makes sense considering they are also one of the key revenue drivers. The £52M reduction in the wage bill from FY2024 to FY2025 is the most consequential thing INEOS has done since buying a stake in the business and running football operations.

Notably, this bill has come down massively by £52M through a combination of high-earner exits, reduced squad-size bonuses without UCL participation and job cuts across staff roles. The FY2026 wage bill should fall further too.

Other operating expenses did increase by £21M to a club record for this category. This bucket includes everything from Matchday operations, marketing, facilities maintenance, IT, legal, and administrative overhead. The increase is partly attributable to the Carrington Training Centre upgrade (one-time), partly to increased commercial activity (higher revenue comes with higher delivery cost), and partly to the transition costs of bringing e-commerce in-house.

Cash Flow

Operating cash flow in FY2025 was £72.7M. This is real cash generated from running the football business (ticket sales, sponsor payments, broadcast distributions, less wages and operating costs paid). This was a decline from the previous year largely driven by higher working capital requirements as the commercial operation scales.

Player transfer spending consumed £230M due to the signings of Leny Yoro, Manuel Ugarte, Matthijs de Ligt, Joshua Zirkzee, Patrick Dorgu and Noussair Mazraoui. While this appears to be a highly discretionary line item, it is far from it. To remain competitive enough to qualify for the Champions League, to satisfy PSR requirements by moving underperforming assets, and to satisfy fan and commercial partner expectations, the club must continuously invest in the squad.

Debt Schedule

The Glazer LBO resulted in huge debt loads placed on the club, which has plagued its finances for decades now. With the INEOS takeover, Manchester United has completed a major refinancing of its primary debt instrument.

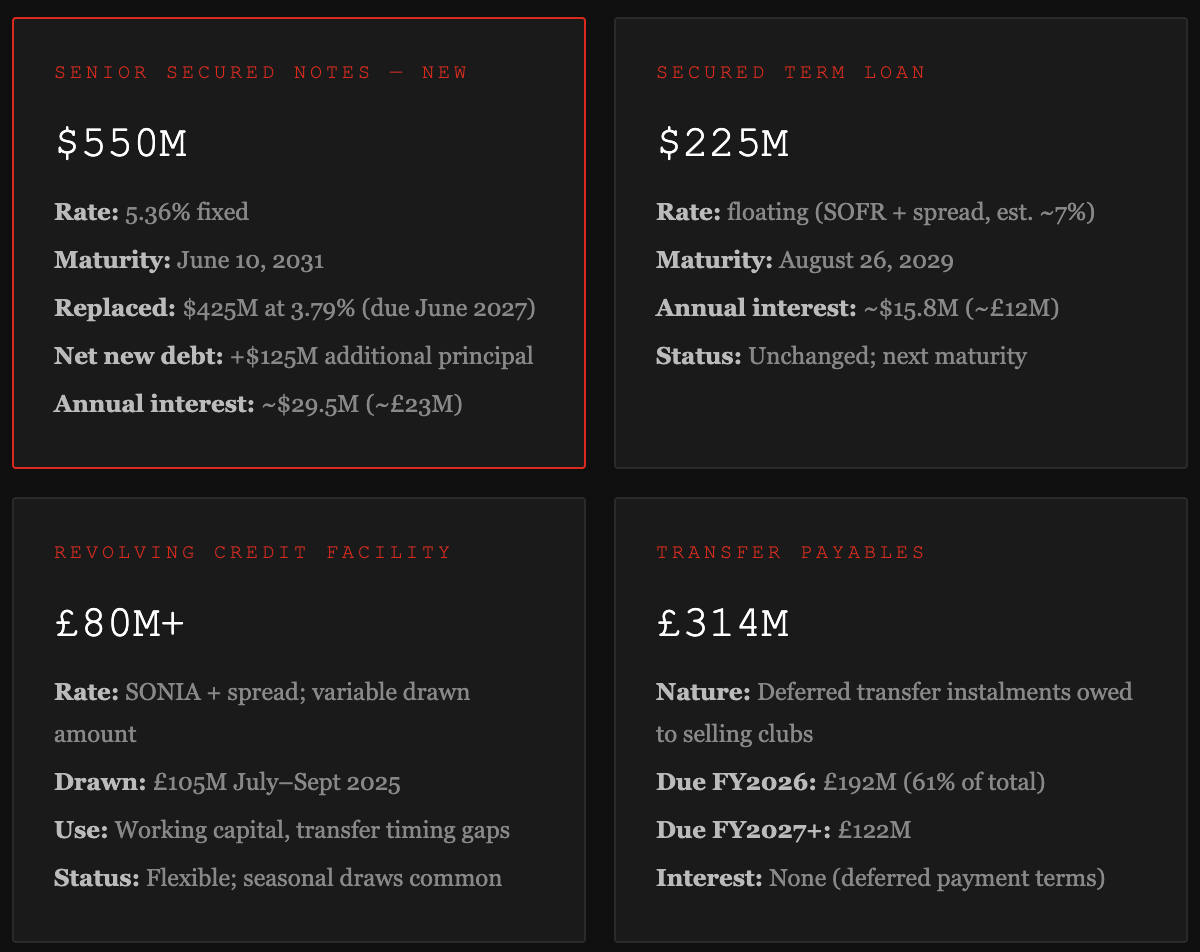

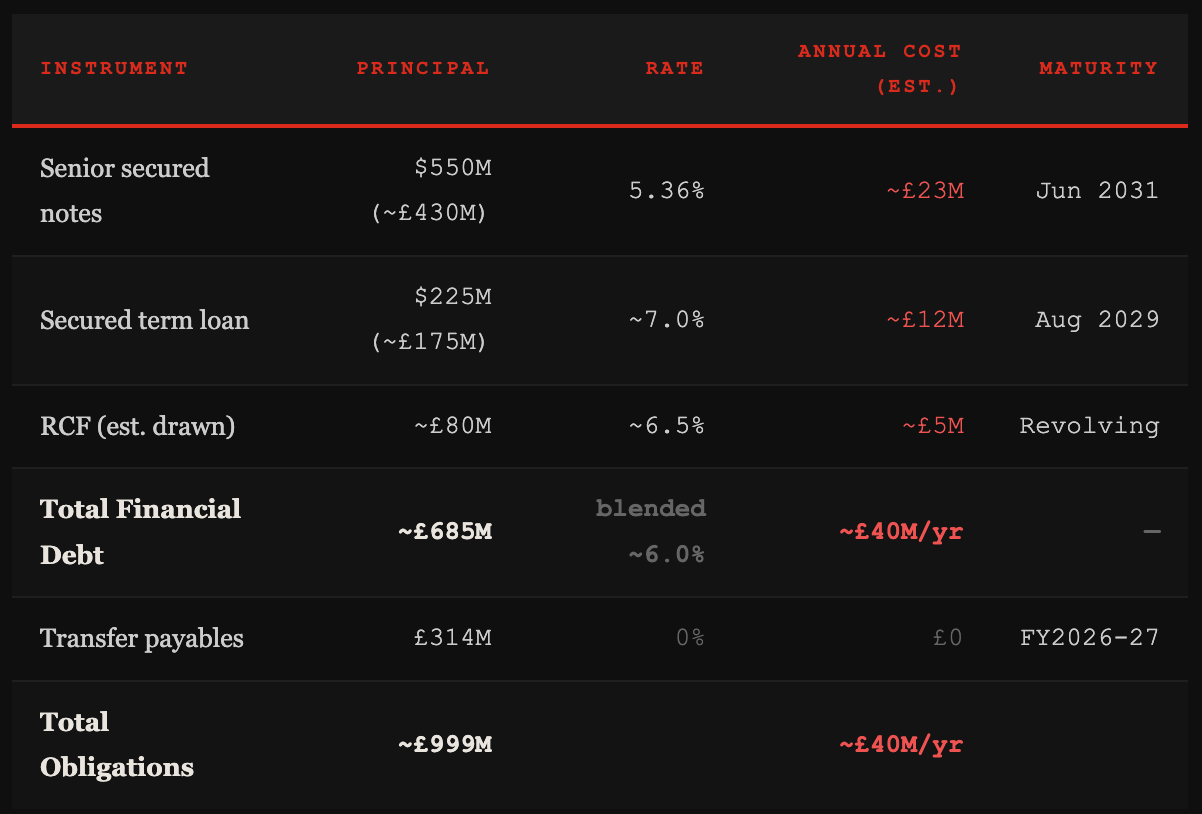

Just last week, United announced a refinancing of the $425M in senior notes at 3.79% into $550M at 5.36%, moving the repayment date from June 2027 to June 2031. This buys the club four more years before it needs to deal with this, and time for UCL revenue to accumulate and for a potential ownership change to simplify the capital structure.

However, this does increase the net interest payments on the debt by $6.7M a year. This is small in isolation, but highlights the key problem, the mounting debt figure that will mean every refinance increases the overall debt and yearly payments accrued.

The next figure to worry about is the $225M term loan due in Aug 2029 at floating rates. If SOFR remains elevated (current est. ~4.5%), the all-in rate is approximately 6.5-7.5%, costing £12-16M/year. This will need addressing before 2029.

FY2026 Trajectory

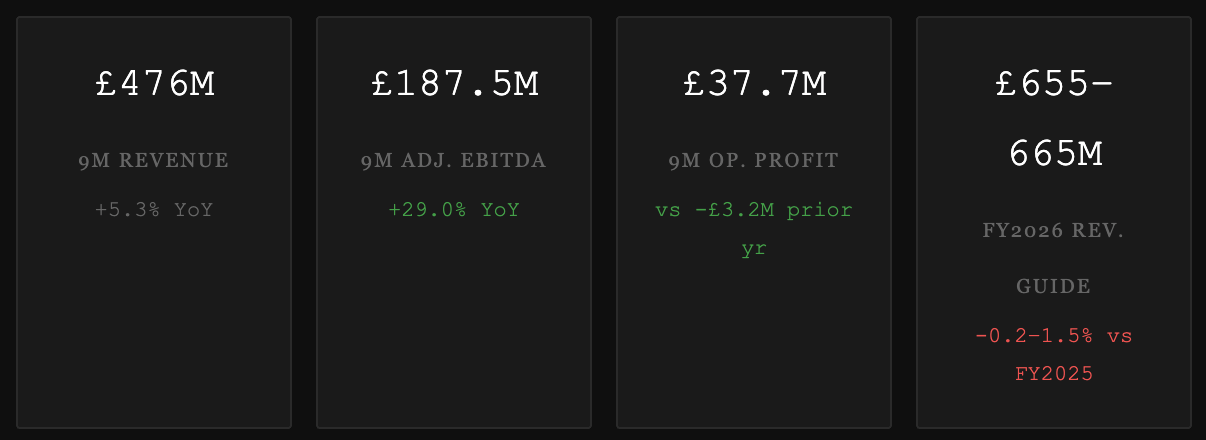

For the nine months ended March 31, 2026, Manchester United has reported:

United also revised FY EBITDA guidance from £180-200M at Q2 to £200-210M, which represents a meaningful step up from FY2025's £182.8M despite lower revenue.

The business at an operational level is clearly getting better. FY2026 will likely see operational improvement start to flow through, but the debt burden will also be most acute given the recent refinancing activity. That said, I do think FY2027 will start to look much better for the business.

The Core Issue

When reading the financials in aggregate, one thing is clear. The business is being undermined by two structural costs that the operating business alone cannot overcome.

Firstly, player amortisation exceeds EBITDA. This means that even in a year of record commercial revenue and significantly reduced wages, the accounting spread of prior transfer decisions consumes the entire operating cash surplus and more.

This is not unique to Manchester United, all major football clubs with active transfer markets face elevated amortisation. However, most successful clubs either generate sufficient EBITDA to absorb it (Liverpool, Manchester City, Real Madrid), or have owners with the balance sheet to absorb recurring losses (PSG, Manchester City) without structural damage. United sits in an uncomfortable middle ground where they have too large a commercial business to be restructured and are too leveraged to absorb the recurring losses painlessly.

Secondly, the £40M annual interest bill on financial debt (post-refinancing) is a permanent fixture as long as the current ownership structure persists. The debt was incurred in 2005 to allow Malcolm Glazer to buy the club. Of the ~£790 million used to buy the club, over £600 million was borrowed from parties such as JPMorgan and hedge funds. As of March 2026, the club still has ~£692m in net debt.

I believe there are two ways to resolve this structural mess. First, a Glazer exit to a well-capitalised buyer who retires the LBO debt with fresh equity, eliminating the £40M interest cost and potentially freeing capital for the stadium. Second, an extended period of Champions League participation generating £80-100M of additional annual revenue that allows the club to self-fund debt reduction over a decade. The optimistic case would be the latter, but the more realistic one would be the former.

5. Ownership & Management

This is perhaps the most important section in this deep dive. Every financial problem at Manchester United traces back to a single decision made in 2004 by an American real estate developer named Malcolm Glazer. Understanding that decision and its 21-year aftermath is the only way to correctly price MANU equity.

Today, Manchester United is controlled by the Glazer family, namely Joel, Avram, Bryan, Edward, Kevin and Darcie, all children of Malcolm who passed away in 2014.

The Leveraged Buyout

In May 2005, Malcolm Glazer completed a hostile takeover of Manchester United for £790M, the largest acquisition in the history of football at the time. Critically, Glazer did not use his own money to fund it. He took out loans totalling approximately £550M, secured against the assets and future cash flows of the club itself.

In other words, the club was made to pay for its own acquisition. This is known as a leveraged buyout (LBO), a structure that is extremely common in private equity, but deeply controversial when applied to a sports club with a fanbase that views itself as a community asset rather than a financial vehicle.

The immediate consequences of this were visible in the annual accounts from 2005 onwards, with interest payments of £50-70M per year, every year, regardless of how the team performed. By June 2026, the club has paid over £1 billion in interest on debt taken on to fund its own purchase. The Glazers have extracted approximately £200M in dividends from the club over the same period.

In essence, they have paid a couple hundred million pounds for an asset now valued at £5B+. The return profile has been incredible them, not so much for the club, fans and other shareholders.

Dual-Class Share Structure

When Manchester United listed on the NYSE in 2012, the Glazers engineered a dual-class share structure that gave them supernormal voting rights of 10 votes for Class B shares versus 1 vote for Class A shares.

As a result, the Glazer family holds approximately 48.9% of economic interest but commands 67.9% of total voting power. No resolution can pass over Glazer objection and today, a public investor buying into MANU Class A shares is effectively purchasing a minority economic interest in a company where they have zero governance input.

June 2026: The Glazers Study an Exit

On June 3, 2026, Bloomberg reported that multiple members of the Glazer family are studying whether to sell part or all of their stake. The family has faced 21 years of fan protests, supporter trusts riots, and green-and-gold campaigns.

No decision has been made with reports stating that the family remains divided. Any transaction would need to navigate the B-share structure and would almost certainly require a premium to the public market price to incentivise all parties. A full sale of the Glazer stake would likely be marketed as a strategic asset sale rather than a market transaction, targeting sovereign wealth funds, US sports owners, or Middle Eastern consortia.

INEOS, Sir Jim Ratcliffe Purchases A Stake

In February 2024, Sir Jim Ratcliffe, founder of INEOS, the British petrochemicals empire, completed the purchase of a 27.7% stake in Manchester United for approximately $1.65B (£1.3B), implying a club valuation of around £5.9B. On top of the £1.3B purchase price, he made a £158M capital injection in February 2024 and in December 2024 he had injected a further £79M, bringing his total shareholding to 28.94%.

The transaction gave INEOS two seats on the Manchester United PLC board and explicit control of all sporting operations, the academy, the first team, transfers, and managerial appointments.

The first 30 months of INEOS control have been characterised by aggressive cost-cutting and structural reform. They eliminated over 250 jobs across the organisation in 2024 and followed up with a second round in 2025, eliminating another ~200 jobs. This was estimated to save the club about £20M annually.

INEOS have also overhauled the structure of the footballing side of things. Sir Jim Ratcliffe and INEOS director of sport Sir Dave Brailsford completely replaced the executive and sporting structure with Omar Berrada was brought in from Manchester City to serve as CEO. Dan Ashworth was poached from Newcastle after United agreed to pay over £10M. He was tasked to oversee all footballing operations, including player recruitment and the academy while Jason Wilcox was hired as the technical director. Ashworth was subsequently sacked just 5 months after officially joining the club which left supporters confused.

The INEOS Problem

The issue is that Ratcliffe's intervention, while operationally credible, is financially constrained in a way that was not fully priced in at the time of his purchase.

INEOS Group Holdings is a privately-held petrochemicals company carrying approximately £18 billion in gross debt. In 2025, S&P downgraded INEOS's credit rating to B+, deep into junk territory, citing margin compression from Chinese overcapacity in the polyethylene market and deteriorating interest coverage ratios. Ratcliffe has subsequently been forced to pursue asset sales across the INEOS empire, including partial divestitures in the cycling and sailing divisions.

The consequence for Manchester United is structural. INEOS cannot credibly be the source of large equity injections into the club on a recurring basis. The £79M top-up in December 2024 may represent the ceiling of what INEOS can comfortably deploy into a sports asset while managing a distressed industrial balance sheet.

United's own net debt sits at approximately £1.29B, the highest since the original Glazer LBO. The club has in effect reached its own debt ceiling. Future investment in the stadium, the squad, or working capital likely requires either new equity from a third party or a Glazer sale that brings in a better-capitalised owner.

6. Valuation

For clarity, I will use all values below in USD as MANU stock trades on the NYSE.

MANU trades at ~$3.9B market cap. However, due to the debt on its balance sheet, the enterprise value is closer to ~$4.8B.

Revenue in FY26E will total ~$872M and guidance is for ~$273M in Adj. EBITDA. Essentially, United trades at 5.5x EV/Revenue and 17.6x EV/EBITDA.

Firstly, I would put more weight on EV/Revenue than EV/EBITDA, because EBITDA as we discussed previously is not clean economic profit. In the nine months to March 2026, United reported £187.5m adjusted EBITDA, but also had £161.1m amortisation, £55.7m net finance costs, £257.9m payments for intangible assets, and £29.2m interest paid. In football, “intangible assets” largely means player registrations. Therefore, EBITDA can look strong while cash keeps being recycled into transfers, wages, interest and infrastructure.

Of course, in valuation, what truly matters is the future. Much of United’s intrinsic value is dependent on how the club does in the next 1, 5 and 10 years.

Let’s look through some key catalysts for the club that could lead to a huge increase in revenue over the foreseeable future.

Stadium Rebuild

Between FY2016 and FY2019, United’s Matchday revenue remained relatively stagnant. FY2020 and FY2021 was a write-off due to the COVID pandemic while FY2023 saw a huge boost in revenues.

This was a direct impact of the 2022/2023 season being a strong year for United in all 3 competitions it participated in. They went far in the Europa League, won the League Cup and reached the final of the FA Cup. This meant 7 more home games and stronger demand for hospitality.

FY2024 highlighted a different thing. FY2024 actually saw 8 less home games compared to FY2023, but despite that revenue stayed flat. This was attributed to pricing/hospitality as United increased ticket prices by 5% for the first time in 11 years.

FY2025 also saw a bump due to 5 more home games compared to the previous year, a deep Europa League run, and more hospitality spend.

What’s clear is that there are 3 key variables today in how much Matchday revenue brings in: pricing, hospitality and competitive success.

However, there is a 4th variable that is worth discussing: the Stadium rebuild. The best analogy to this is the Real Madrid example.

Real Madrid is the most successful team in the world and their stadium, the Bernabéu, prior to FY2024 seated ~81,000 people, making it a very similar sized stadium to Old Trafford. Interestingly, their Matchday revenue was very similar to Old Trafford, remaining relatively stagnant from FY2016 to FY2023, excl. the COVID pandemic.

Real Madrid’s Matchday revenue jumped from €122M in FY2023 to €248M in FY2024, up roughly €126M, or +103%. Naturally, most would assume this meant the seat capacity doubled to allow for this. However, in actuality, it is estimated that seat capacity increased by only 2.5-3%. The uplift in revenue came from increased monetisation of those seats through Personal Seat Licences and new VIP seats. It must be noted that the renovation did not come cheap however, with figures suggesting that the stadium project investment cost as much as €1.347B.

A stadium rebuild could therefore increase Matchday revenues materially for United. Previously, we discussed how moving from 74,879 to 100,000 seats is a ~33% capacity increase, and at United's current Matchday yield of roughly £2,140/seat/season, that alone adds ~£53M annually.

A new-build stadium with a materially better hospitality mix, more premium sections, better suites, improved F&B infrastructure, could realistically lift per-seat yield by 20-30%, producing total incremental Matchday revenue of £50-110M per year above the current £160M base.

Return to Champions League Football

This is the most immediate revenue driver for the business. In FY2025, United’s broadcasting revenue fell £48.9m, or 22%, to £172.9m, mainly because the men’s team played in the Europa League instead of the Champions League and finished 15th in the Premier League versus 8th the year before.

By May 2026, United had secured Champions League qualification again, and Reuters reported that the club raised FY2026 revenue guidance to £655m–£665m, partly helped by a third-place Premier League finish.

The recent 2025-2026 season is the lowest number of home games United have played in decades due to them bowing out at the first round of both domestic cup competitions and not qualifying for Europe. A return to European football would guarantee at least four more home games, and potentially many more if they were to make a deep run in all competitions. The theoretical maximum number of home games for an English top-flight team in a season is 35. If United can get to 29-30 home games next season, it could boost Matchday revenue by about £40M from FY2026 to FY2027 considering the average revenue per home match is ~£5.3M.

Of course, competitive success also leads to more lucrative sponsorships, partnerships and broadcasting revenue.

a. Sponsorship Revenue

Most sponsor clauses are private so it is harder to determine the exact number for this. However, there is one disclosed clause that is significant. United’s Adidas extension includes a £10M deduction for each year of non-Champions League participation from 2025/26 onwards. The Adidas deal can also increase by up to £4.4M per year based on performance in league, domestic and continental competitions.

United’s FY2025 sponsorship revenue was £188.4m, so even a 10% uplift from better sponsor pricing, bonuses and renewals would equate to ~£18M.

b. Broadcasting Revenue

UEFA’s current Champions League distribution is much richer than Europa League. The UCL league phase alone gives each club €18.62m just for qualifying, plus €2.1m per win, €700k per draw, league ranking bonuses, value-pillar money, and knockout bonuses.

Just being in the Champions League is probably a £55m-£75m broadcasting/UEFA uplift versus no Europe for United while going deep can make it £100m+.

Putting the Revenue Bridge Together

I think the more interesting question to ask is “What can revenue look like if the club is run properly and returns to consistent Champions League football?”

Starting from FY2026E revenue of roughly £660M:

A normalised Champions League uplift could add £55M-£75M

A deeper European run and more home games could push that to £100M+

A stadium rebuild or major redevelopment could add £50M-£110M in annual Matchday revenue over time.

Commercial repricing from better performance, better sponsorship demand and a stronger global product could add £30M-£50M.

So, over the medium term, it is not hard to see a path where United goes from ~£660M revenue today to £850M-£950M revenue.

In USD, that is roughly $1.1B-$1.25B of annual revenue.

I believe that is the core bull case. Today, United trades at around $4.8B EV on $872M revenue, or 5.5x EV/Revenue. But if revenue can get to $1.15B over time, then today’s EV is only ~4.2x forward medium-term revenue.

The Multiple

The other important point is that football clubs are not normal businesses. They are typically trophy assets, and there are only a handful of these truly global football clubs. Manchester United is certainly one of them.

I believe this means that it is almost impossible to value them purely on EBITDA or free cash flow. A normal industrial company that burns cash on transfers, wages and interest would deserve a lower multiple. However, a scarce global sports asset with irreplaceable brand equity, global distribution and billionaire-owner demand can trade at a premium to what near-term financials imply.

Of course, that doesn’t mean price does not matter at all. But it means United should probably be valued closer to a scarce sports franchise than a normal consumer business. If United can reach $1.1B-$1.25B of revenue, then applying a 5.5x-7.0x EV/Revenue multiple gives an enterprise value of roughly $6.1B-$8.8B.

After subtracting net debt, the equity value could be roughly $5.2B-$7.9B.

Compared to the current market cap of ~$3.9B, that implies around 30%-100% upside.

Bull Case

The bull case is that United becomes a structurally larger business and that revenue moves toward $1.2B+. This would require a stadium rebuild, the club to become consistent Champions League participants again, which would drive more commercial and broadcasting success, as well as spending more frugally in the transfer market, relying on home-grown talent like they used to.

In that scenario, United could be worth $8B-$10B enterprise value over time.

Bear Case

The bear case is equally simple. United remains inconsistent on the pitch, Champions League qualification is not sustained, the stadium project becomes expensive, delayed or poorly financed and transfer spending continues to absorb most of the cash flow. Interest costs remain high and the debt keeps climbing.

My View

At the current valuation, I would not say United is cheap based on present financials alone. It requires quite a few assumptions that I’m not sure the recent history of United would suggest it is capable of.

7. Bull and Bear Case

Bull Case

United is a scarce trophy asset and should be accorded a premium valuation

Manchester United should not be valued like a normal football operating company. It is one of the very few listed ways to own exposure to a global sports trophy asset. These assets are rare, emotionally owned, supply-constrained and usually transact at values that look expensive on normal earnings metrics. There are only a handful of football clubs with Manchester United’s global relevance, history, fanbase, brand recognition and commercial reach.

At the latest quoted price, United trades at about $4.8B in EV. Forbes values Manchester United at $7.2B as of May 2026. Forbes states that their methodology is based on historical club transactions and the future economics of each league and team.

I think the scarcity point is extremely interesting as sports assets are increasingly being bought by billionaires, sovereign wealth-linked investors, private equity and strategic investors who are not necessarily underwriting the asset on near-term free cash flow. Instead, they are valuing the asset based on scarcity, global distribution, brand permanence and optionality. I think that could command a premium.

Ratcliffe’s transaction provides a valuation anchor

Valuation is a subjective matter, but the price at which an asset was actually transacted is certainly objective. Sir Jim Ratcliffe agreed to acquire 25% of the Class B shares, and pay the Glazer family and Class A shareholders $33.00 per share. The deal also included a further $300m investment intended for future investment into Old Trafford.

That is about a 50% premium from current prices. Of course, it doesn’t automatically mean MANU is worth $33 today, because Ratcliffe received strategic influence that ordinary Class A shareholders do not have. However, it is an interesting anchor. It is also arguable that the club’s value has gone up since.

INEOS gives the club a credible football-operations reset

For over a decade now since Ferguson’s retirement, United has been a laughing stock to many for how inefficient its football operations were. They have shuffled through 6 full-time managers since Ferguson retired, excluding 5 interim managers. Transfer spending has been extremely poor, with zero wage discipline.

INEOS has hired experienced football people to run the operations and it appears to be paying off. The 4 summer signings last season: Matheus Cunha, Bryan Mbeumo, Benjamin Sesko and Senne Lammens have been a huge success for the club and key to the 3rd place finish.

INEOS will not fix everything, but it is that the probability of better football decision-making is higher than under the previous structure. If United can improve recruitment, reduce wasted wages, build a more coherent squad and stop paying for repeated managerial resets, the operating leverage will be very meaningful.

As we discussed, much of it comes down to competitive success on the pitch. Better football leads to higher league placement, European qualification, more home matches, stronger sponsorship conversations, more merchandise sales and better global engagement.

Champions League return has immediate financial impact

United’s 3rd place finish in the Premier League led to the company also raised FY2026 revenue guidance to £655-665m and adjusted EBITDA guidance to £200-210m.

This matters because United’s revenue is very sensitive to Champions League participation. Europe affects broadcasting revenue, matchday revenue, sponsorship visibility, player attractiveness and brand momentum. A Champions League season usually means more high-value home fixtures, more global TV visibility and better commercial activation opportunities.

The cost cuts appear to be paying off

In the past decade, United was a high-revenue but poorly run asset. The club had enormous commercial power, but too much of that power leaked away through wages, transfer mistakes, manager pay-offs, bloated headcount and inefficient operations. The 450 job cuts, cancelled ambassadorial contracts and other cost-saving initiatives have started to pay off.

For the nine months to March 2026, United generated £37.7m of operating profit, versus a £3.2m operating loss in the prior-year period. Adjusted EBITDA increased 29.0% to £187.5m. Management specifically pointed to operating cost and headcount reduction programmes, alongside improved Premier League performance.

The new stadium is a massive call option

A new stadium could transform the economics of the entire club. Approximately 33% more seats, more premium hospitality, more sponsorship inventory, better food and beverage, improved retail, more non-football events, possible naming rights, and a much better fan experience.

The Real Madrid comparison is extremely useful and shows a 100% uplift is possible. Real Madrid’s own 2024/25 accounts also said the first full cycle without construction restrictions saw recurring stadium capacity and commercial operations fully operating, and that excluding personal seat licence revenue, recurring capacity and stadium commercial operations were 38% higher than the prior year.

United’s massive fan base and iconic brand deserves a new and improved stadium that would be befitting of a club of its stature.

Bear Case

Public shareholders have zero control, and the Glazers have proven to be poor capital allocators

The Glazers’ supernormal voting rights mean that MANU Class A shareholders have no say in forcing a sale, demanding capital allocation discipline or any other matter. This is why the stock can trade below private-market value for a long time. The club may be worth $6B or $7B to a buyer, but if no control transaction happens, public shareholders only own a listed minority stake in a controlled company.

The Glazers have left the club with persistent debt, and paid themselves dividends while the club remains indebted and loss-making. For instance, in FY2022, they paid themselves £33.6m of dividends while also drawing £40m on its revolving credit facility. In the same year, net debt increased to £514.9m, finance costs were £62.2m, and the club made a net loss of £115.5m. United also had the most negative net transfer balance among big-five league clubs over a ten-season period, with a negative balance of more than €1B.

Debt is significant and does not appear to be decreasing

21 years after Malcolm Glazer loaded £550M of acquisition debt onto Manchester United's balance sheet, the club carries more financial obligation today than at the 2009 peak and there is no clear path to reduction.

Combined interest runs ~£68M per year against operating free cash flow that barely exceeded £70M in FY2025 before player investment. There is no deleveraging catalyst visible. The proposed 100,000-seat New Trafford will require ~£2B in additional financing. Every Champions League miss will deteriorate the debt-to-revenue ratio further.

United’s sporting performance is very volatile, and the financial model depends on it

United’s financial results are heavily tied to on-pitch outcomes. Broadcasting revenue, Matchday revenue, sponsorship visibility, merchandise sales and player costs all move with sporting performance.

FY2025 is a good example. Broadcasting revenue fell 22.0% YoY to £172.9m, mainly because United played in the Europa League rather than the Champions League and finished 15th in the Premier League versus 8th the year before.

This is a single source dependency and not exactly something that breeds confidence. Shareholders would therefore have to buy into an unknown future that is ever-changing.

The stadium upside may come with dilution or more debt

The stadium is the biggest call option, but it is also one of the biggest risks. United has only said work continues on the ambition to build a new 100,000-seat stadium, however there are huge question marks over the funding structure.

Real Madrid proves the revenue opportunity, but it also proves the capital intensity. Real Madrid’s stadium remodelling project had total investment of €1.347B by FY2024/25, with €1.132B of stadium project loan used.

For United, the bear concern is that stadium upside may be real but not necessarily equity-accretive for minority shareholders. If the project requires large new debt or dilution, the market may apply an even bigger discount.

Commercial strength is not immune to underperformance

I think one of the scariest threats to United is the prospect of its rivals overtaking them in terms of revenues and popularity. The chart below is an obvious sign. Ultimately, sponsorship and merchandise revenue depend on visibility, sentiment and relevance. If the club is not competing at the top level, commercial partners may still pay for the brand, but the highest-value deals become harder to justify.

In a relatively short 10 year span, United has seen many of its rivals catch up with its revenue numbers despite being ahead by at least 50-100%. Younger fans will naturally support more successful teams, and in the Premier League, those are Man City, Arsenal and Liverpool today. In fact, it has been the case for a decade now.

8. Concluding Thoughts (What I’m personally doing)

I'll start by acknowledging the obvious conflict of interest. I am a Manchester United fan, and I have been for most of my life. I've tried to write this as objectively as possible, but you should factor in that bias when reading my conclusions.

The honest answer is that this is not a clean investment. It does not fit into the typical framework of a business I like:

There is no clear earnings inflection, the debt is incredibly high, governance is structurally broken and free cash flow is negative.

Yet, I think there is a case to be had here for certain investors. The case is that you are buying a scarce global trophy asset at a discount to its private market value, with a credible near-term catalyst in the form of a Glazer exit. The June 2026 Bloomberg report on the family studying a full or partial sale is the most significant development for MANU equity in years.

A full Glazer exit to a well-capitalised buyer such as sovereign wealth, US sports money or a Middle Eastern consortium would retire the LBO debt, restructure governance, and likely unlock a re-rating toward private market value. Ratcliffe also paid $33 per share for his stake, about 50% higher than the price it now trades at.

There are of course, many risks that was just highlighted, largest of which is that the debt continues to accumulate, the Glazers stay in power and performances remain inconsistent.

Personally, I do not hold a position in MANU and do not intend to for the foreseeable future. That said, this has been a very eye-opening deep dive for me and one that I thoroughly enjoyed. I hope you learned something from this deep dive regardless of whether you decide to take the opportunity to invest.

Thank you for reading!

-Gab

Additional Content to Watch/Read:

If you’re interested in learning more about Manchester United stock, I would highly recommend these resources:

If you enjoyed this and would like to read more deep dives by me, click on this link.

Share It With A Friend!

If you know a football (soccer) supporter who you think would enjoy this, kindly share this article with them. It is completely free to read and I would be extremely grateful.

Paid Subscription Upgrade

If you’d like to support the work I do, consider becoming a paid subscriber. Your support will allow me to spend more time finding asymmetric opportunities in the market, writing and analysing various businesses.

As a reminder, paid subscribers get access to:

Monthly Portfolio Updates (+98% in 2024, +26% in 2025)

Earnings Reviews on Portfolio Companies (SE, GRAB, DLO, MELI etc)

Archive of Deep Dives and Posts (17 Deep Dives and counting)

For the next week, you can get 50% off your first month with the link below.

Disclaimer: The content presented in this thesis is for informational and academic purposes only and does not constitute financial advice. The analysis and opinions expressed are based on research and should not be interpreted as a recommendation to buy, sell, or hold any security. Readers should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.

from one united fan to another, great work on this! would actually love to see you doing some back of the envelope LBO on a potential deal - could be an interesting time to dive into it especially with increasing number of deals among sports clubs. mentioning how shambolic the club has been in their transfer windows would've been great, especially how EtH destroyed the depth of our academy players. also, one thing i will have to disagree on is the 4 signings were great, but they weren't exactly marquee players. the reason for our success and 3rd place finish can be largely attributed to Carrick's takeover and next season's success will be on him as well (which drives the commercial value of the club).

I must say, if I am going to read 40+ minutes of a breakdown into a company, I would prefer to read about Arsenal but when the level of content is this high, I'll have to read it anyways.

Thanks for doing the research into this fascinating niche.