Is CoreWeave a Buy or Sell at these prices?

CoreWeave is one of the most debated stocks in the market today where bulls and bears are equally confident in their thesis.

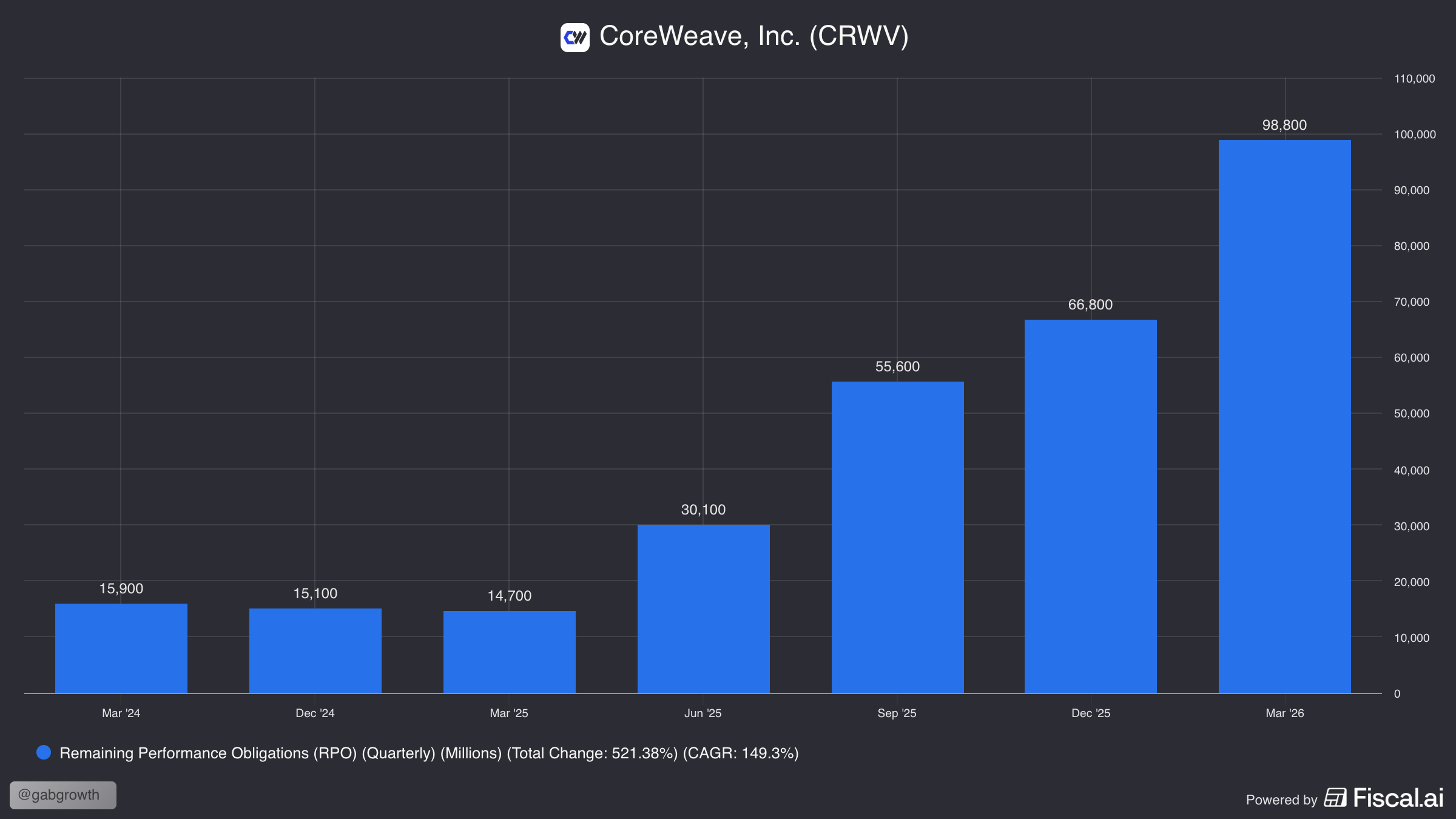

Their primary business model is renting GPU capacity to the most important companies in the world, with a client list including OpenAI, Meta, Anthropic, and Microsoft. Its largest shareholder after the founders is NVIDIA. Revenue grew 112% year-over-year in Q1 2026 to $2.08B and its contracted backlog is now $99.4B.

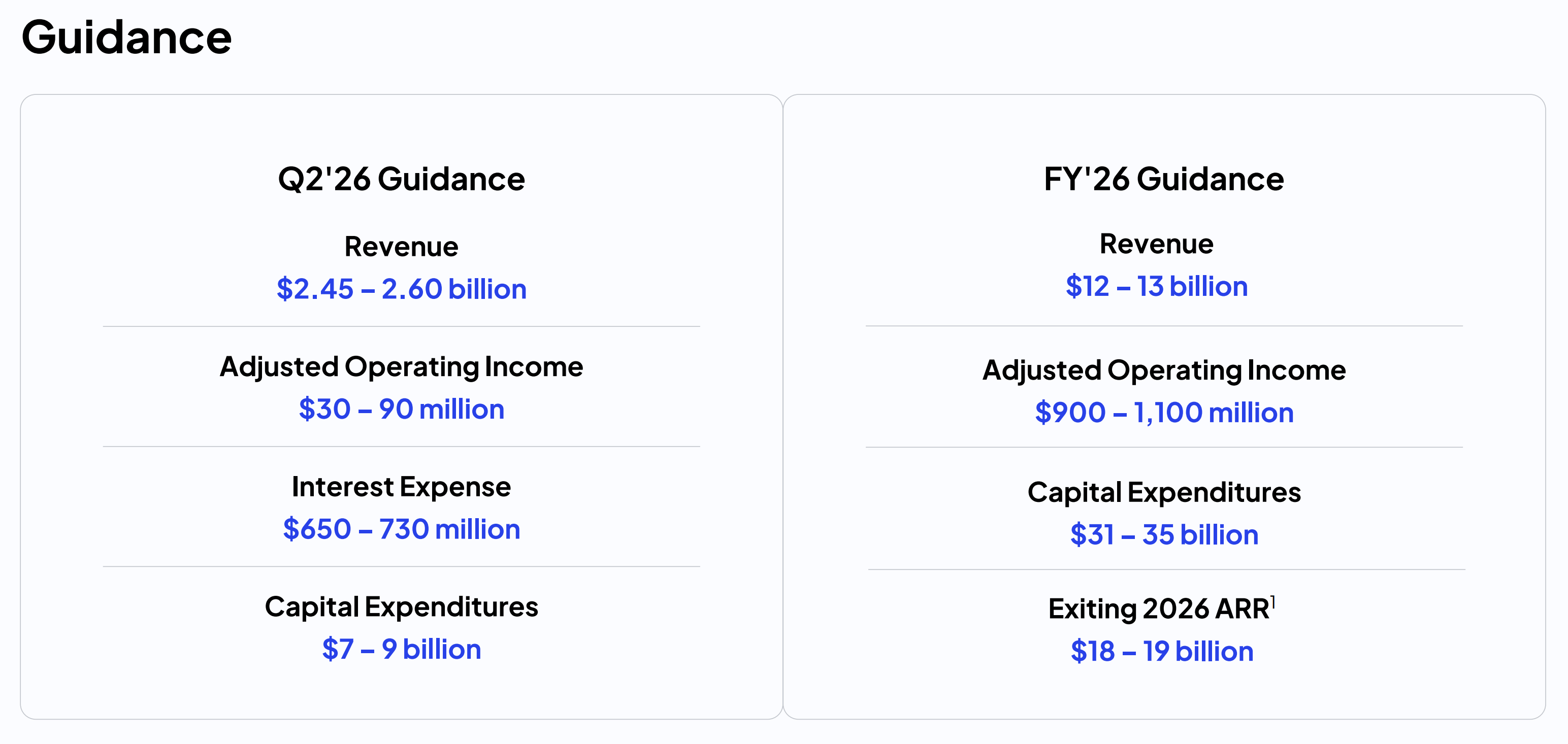

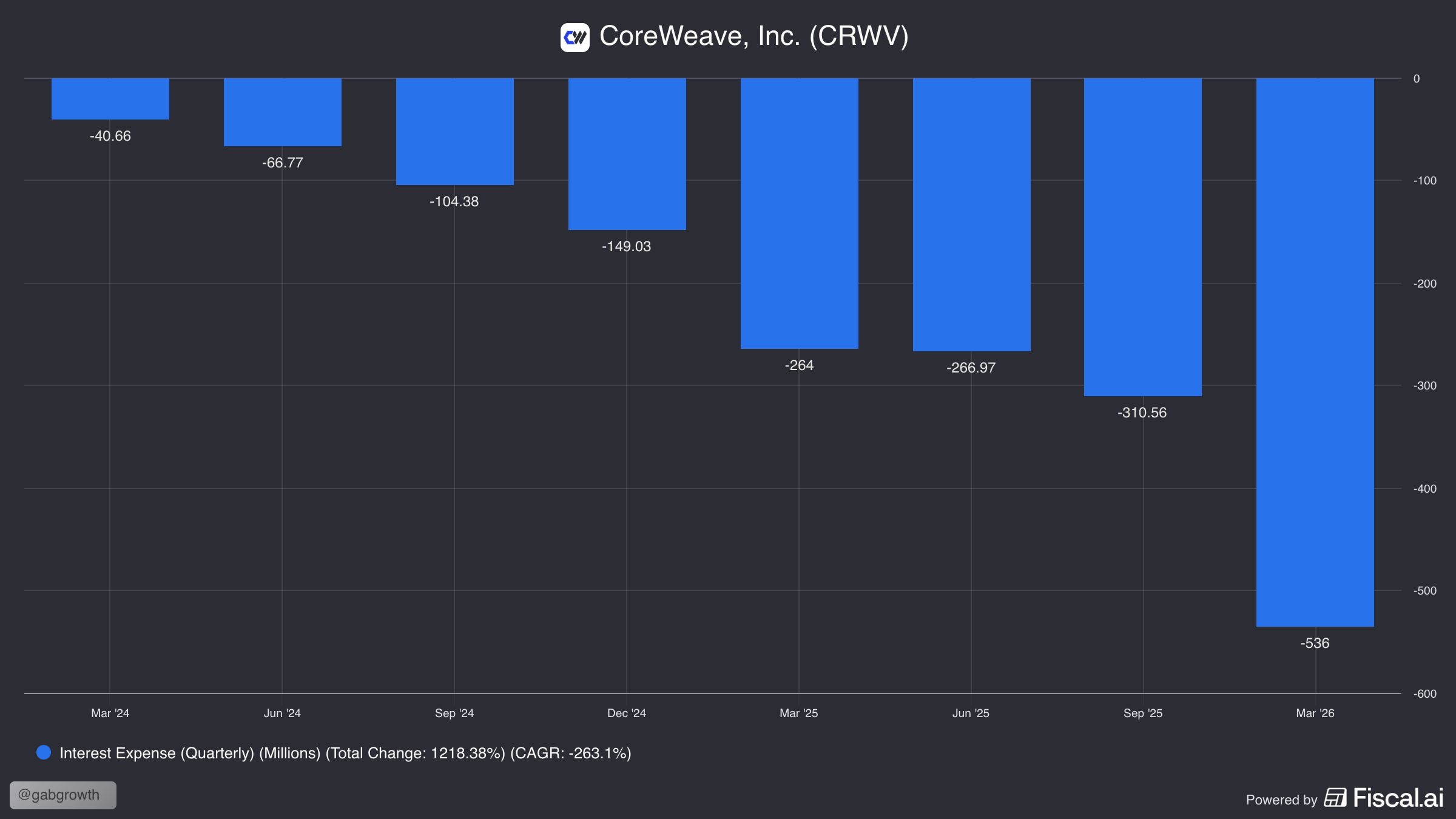

Yet, it carries $35B in debt, which resulted in a $536M interest payment in a single quarter while burning $4.71B in free cash flow within that same 3 month period. CAPEX guidance for 2026 is $31-35B, which is larger than the annual revenue of most S&P 500 companies.

The bull case for CoreWeave is that it is a generational infrastructure franchise that will be the key cog in the AI buildout.

The bear case is that it is an AI bubble proxy that rests on a handful of hyper-scaler contracts that could be re-negotiated or cancelled if demand falls.

In this piece, we will work through the key debate points and end with what I am personally doing and why.

Table of Contents

The Bear Case

The Bulls’ Counter to the Bear Case

The Bull Case

Conclusion: My View

1. The Bear Case

Let’s first start with the bear case, and understand it from the bears’ point of view.

GPU depreciation makes the economics look better than they are

CoreWeave reports adjusted EBITDA margins of 56-60%. Some bears argue that GPU hardware depreciates at approximately 30-40% per year as successive generations are released. On a $31-35 billion CAPEX programme, the depreciation charge flowing through operating income over the next 3-5 years will reach an estimated $7-12 billion per year by 2027.

If that holds true, the 60% EBITDA margin collapses to 7-8% at the adjusted operating income level. In essence, bears are arguing that the H100 cluster generating revenue today is partially obsolete the moment Rubin is deployed. They also argue that investors pricing CoreWeave on EBITDA are systematically ignoring a real economic cost embedded in the asset base.

The backlog is not a receivable

The $99.4 billion figure is reported under ASC 606 (U.S. GAAP Standard) as remaining performance obligations, which sounds unconditional. However, it is not a guaranteed number. Take-or-pay provisions vary by contract and some backlog includes customer options to expand that are included on a signed basis but represent customer rights, not CoreWeave’s receivables. CoreWeave does not disclose what proportion of the backlog is genuinely non-cancellable versus terminable with penalty payments.

The Training-to-Inference transition structurally impairs the business

CoreWeave’s architecture of bare-metal servers, InfiniBand fabric, dense GPU clusters is purpose-built for model training. Inference at scale, which is where the volume goes as AI products serve hundreds of millions of users, requires geographically distributed compute with low latency to the end user. AWS has 32 regions globally while Azure has 60+.

CoreWeave has 40 facilities, but they are primarily in the United States. For global consumer inference, that footprint is not enough to stay competitive. As the frontier AI labs shift from building models to running them at scale, the demand profile could migrate towards hyperscalers.

The leverage is permanent, not transitory

CoreWeave is paying around $2.1 billion of annual interest expense, which is roughly 17-18% of guided 2026 revenue. That is a real drag on equity holders, regardless of how exciting the top-line growth looks. The other issue is that the debt is not simple corporate debt. A lot of it is backed by GPUs, and GPUs are depreciating assets. Every time NVIDIA releases a new generation, the collateral value of the older GPUs falls. That matters because CoreWeave will need to refinance a large part of this debt in 2027-2028.

If the company enters that refinancing window without proving it can generate real free cash flow, lenders are not going to underwrite it cheaply. They will price in the uncertainty through higher spreads, tighter terms, or both.

2. The Bulls’ Counter to the Bear Case

1. GPU depreciation makes the economics look better than they are

Bull counter: Depreciation is only a problem if GPU revenue decays faster than the asset base.

The bull counter is that bears may be treating GPU depreciation too harshly. While H100s and Blackwell’s will be less valuable once Rubin and future generations are widely available. However, that does not mean previous generations become worthless overnight.

Older GPUs can still be used for inference, fine-tuning, enterprise AI workloads, batch processing, rendering and lower-priority compute. In a world where AI demand continues to outstrip available power, data-centre capacity and advanced GPUs, the useful life of older chips could be longer than bears assume.

CoreWeave itself depreciates technology equipment over six years, after changing its estimate from five to six years in 2023. That does not prove the economic life is six years, but it shows management is assuming a much longer life than the 30-40% annual obsolescence bear case implies.

In recent months, we have gotten more evidence that GPUs can run workloads for much longer than bears are predicting, and still earn attractive revenue even after new and future architectures are widely available.

NVIDIA’s own vGPU lifecycle docs state that supported GPUs usually come with an OEM hardware warranty of around 3 years, and NVIDIA’s software support lifecycle can extend beyond the first full-support period through extended full support and maintenance support phases. That tells us these GPUs are not designed to become unusable after one generation.

Second, hyperscalers generally use multi-year depreciation lives for servers and networking equipment. Microsoft moved server and network equipment useful lives from 4 years to 6 years in FY2023. Alphabet also moved servers and certain network equipment to 6 years in 2023.

Older GPUs are still commercially useful. AWS still lists P3 instances with NVIDIA V100 GPUs, even though V100 launched back in 2017. AWS also still offers A100-based P4 instances (launched in 2020), while Google Cloud and Azure still list A100-based GPU products. As we know, data center space and power capacity are one of the crucial bottlenecks today. If these old GPUs weren’t profitable to operate, and if they were dragging down margins, why would the 3 hyperscalers not replace them?

xAI built phase one of Colossus I with 100,000 H100 GPUs. This was despite H200 having already been released and right before the launch of the B200. Why did Elon decide to choose the H100, despite the H200 being available?

Gavin Baker also made a very good point on the recent “Invest Like The Best” podcast, where he argued that disaggregating prefill and decode could extend GPU useful lives from the 3-4 years many lenders were underwriting to something much longer. In his framing, you could put a specialised inference system in front of Hopper or Ampere capacity, use those older GPUs for the phase where they still perform well, and extend the useful life of the asset materially.

If this is true, it would change the CoreWeave debate pretty meaningfully. The bear case assumes that GPUs become obsolete in 2.5 to 3 years. The bull case is that software, workload routing and inference architecture can extend the monetisable life of the hardware. In that scenario, the useful life of a GPU is not just determined by NVIDIA’s product cycle, it will also be determined by how well the market can reallocate older chips into the right workloads.

This would also matter for financing too. If lenders and the market believes that older GPUs can remain cash-generative for much longer, then collateral values improve, financing rates come down, and the entire AI infrastructure build-out becomes easier to fund.

The backlog is not a receivable

Bull counter: It is not a receivable, but with demand through the roof and not stopping soon, it is of much higher certainty than bears believe.

I believe the bears have a very good point here and it is also one of the core concerns I have.