Grab's $65B Quick Commerce Opportunity

A breakdown of food delivery, grocery, and non-food instant retail and how Grab is positioned to compete across all three segments

When we look at Southeast Asia’s quick commerce market, it is essentially three overlapping markets compounding simultaneously.

Food delivery is the foundation of it all, and the largest by far at the moment. It is a $23B market today which will grow to ~$35B by 2030. On-demand grocery and daily essentials is a largely untapped opportunity at the moment that could grow to ~$18B by 2030. Non-food instant retail will add a further $12B or so.

Together, these three layers represent a $65B quick commerce market by 2030, roughly 3x the size of the food delivery market today.

Grab is the only platform with an existing operational footprint across all three layers, but its current share of the grocery and non-food prize is negligible. To capture the opportunity, it will require a major supply-side buildout.

This report will examine each layer of quick commerce, Grab’s current position, the investments required to make it happen, and what the economics look like if Grab executes to a tee.

In case you missed the deep dive on the quick commerce landscape in China and Southeast Asia, do check out the free article linked below:

[Deep Dive] Alibaba, Meituan and JD's Quick Commerce War and How Grab and Sea Will React

![[Deep Dive] Alibaba, Meituan and JD's Quick Commerce War and How Grab and Sea Will React](https://substackcdn.com/image/fetch/$s_!4Mkm!,w_1300,h_650,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Ff095ce3c-1df7-4f3f-8a08-fc995b484668_1200x630.png)

This piece was written in collaboration with Zack Zhu, who publishes Contrarian Perspectives and is one of the sharpest analysts I know. Zack anchored the China section with ground-level insight into how Meituan, Alibaba, JD, and Douyin are actually fighting this battle, and why the unit economics matter more than the headlines.

It is a 15,000 word article written in collaboration with Contrarian Perspectives where we go through exactly why quick commerce is being competed over fiercely by major players across China and Southeast Asia.

1. The $65 Billion Market

The defining structural insight about quick commerce in Southeast Asia is that it is not a single market with a single competitive dynamic. Instead, it is three distinct demand pools, each at a different stage of maturity, different unit economics and each requiring a different set of merchant and infrastructure capabilities.

Yet, all three can, in principle, be served by the same on-demand rider network.

This is the strategic logic behind quick commerce as a platform play. Achieving sufficient density in food delivery means solving the hardest infrastructure problem. Specifically, a platform will need a highly-liquid, city-level rider network with excellent demand forecasting and merchant relationships. Both groceries/daily essentials and non-food instant retail rides on that existing network at no marginal cost. That is the beauty of this quick commerce opportunity.

For Grab, it is crucial that they treat food delivery as the foundation of this journey, not the destination.

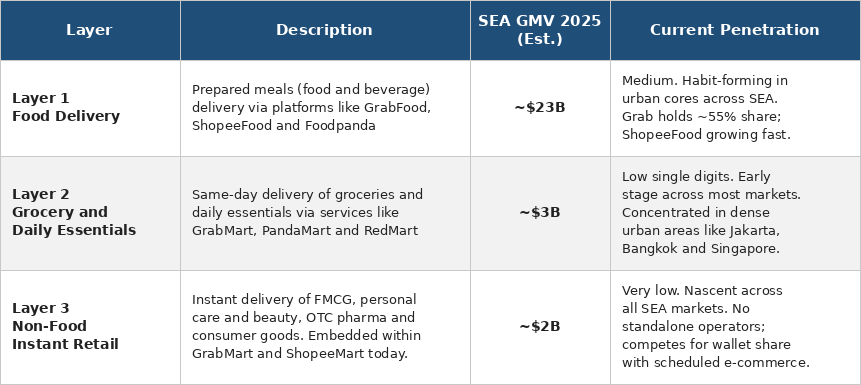

These are the 3 layers and how I define them:

Layer 1: Food Delivery

This refers to prepared meals (food & beverage) delivery, and as of 2025, GMV is projected to be ~$23B according to Momentum Works. Grab owns ~55% of the market.

Layer 2: Grocery & Daily Essentials

This refers to services like GrabMart, PandaMart and RedMart that offers same-day delivery of groceries and daily essentials. GrabMart is ~10% of GrabFood as of Q4 2025, implying a bottom-up estimate of ~$3B in market size for this business. (Noting that RedMart for instance, has no food delivery segment and therefore is incremental to this number)

Layer 3: Non-Food Instant Retail

Non-food instant retail is the smallest layer today and encompasses FMCG products, personal care and beauty, OTC pharmaceuticals etc…

This segment currently accounts for over 40% of China’s total quick commerce market today. With how nascent this space is in Southeast Asia, I would give an estimate of ~$2B for this segment, although there is massive room for growth.

2. Layer 1: Food Delivery

Food delivery is the most mature of the three layers and the one where Grab maintains dominance. Grab currently has ~55% market share across Southeast Asia and is the closest equivalent to Meituan in the region, a platform in China that has leveraged food delivery to build a massive logistics and consumer internet business that is now fuelling their quick commerce charge.

For Grab, food delivery is not primarily about market share gain. Rather, it is about continued category expansion with more restaurants, more cuisines, more price tiers, and deepening the habit across its user base.

In terms of the financial profile for this segment, Grab has a take rate of ~20-30% on restaurant GMV with delivery fees partially passed onto consumers. Grab’s model is therefore to monetise the movement of goods and skim a small take from each transaction. Grab also offers sponsored listings, promotional campaigns and other merchant services that provide visibility. In return for this, restaurants on GrabFood get access to millions of active users with intent to order. Grab also handles payment processing, fraud risk, chargebacks and cash float.

Overall, this is not a high-margin business in isolation. But it is the very foundation on which quick commerce will be built and the engine that keeps riders deployed, demand predictable and the platform within the consumer’s daily habit loop.

3. Layer 2: Grocery & Daily Essentials

Online grocery in Southeast Asia is one of the most structurally under-penetrated categories in digital commerce. Across most SEA markets, online grocery accounts for low single digits of total grocery retail spend, compared to 10-15% in mature markets like South Korea, Japan and the UK. In fact, it is ~25% in China.

I believe the gap between current penetration and mature market benchmarks represent the bulk of the layer 2 opportunity.

The reason behind the low penetration rates really boils down to a few key reasons. One, consumers in Southeast Asia who purchase groceries are typically the elderly who cook for their large multi-generational families. They are very skeptical over fresh produce quality and two, have the habit of frequenting their usual wet market spot where they can select items individually. Thirdly, the low basket sizes make delivery economics rather challenging without subsidies or subscription programmes.

However, these are challenges that can be overcome easily. For one, these constraints are likely to erode over time as consumer familiarity with on-demand delivery increases and as platforms invest in fulfilment consistency.

We’ve seen a similar story in China where food delivery became sufficiently habitual, and consumers began applying the same convenience expectation to adjacent categories. For example, a user who orders GrabFood daily may start asking why their shampoo, rice, or cooking oil is taking two days to arrive.

In 2022, the total grocery retail market in Southeast Asia was estimated at about $475B, growing 7% annually. That would imply a $622B market in 2026.

By 2030, if online grocery penetration reaches just 8% of total grocery retail (which still implies a level lower than most developed Asian markets), that would imply approximately $60B in online grocery GMV.

The majority of this would likely still be fulfilled through next-day delivery or longer. In terms of instant/same-day delivery which would qualify as quick commerce, I believe a realistic number here could be 30%. If so, that would equate to this segment being worth $18B in 2030.

GrabMart is positioned to compete for a meaningful share of this through its layer 1 capabilities.

4. Layer 3: Non-Food Instant Retail

Non-food instant retail is the smallest layer today but the fastest growing. It encompasses FMCG products, personal care and beauty, over-the-counter pharmaceuticals, baby and pet care, consumer electronics accessories, and eventually a broader range of lifestyle and home products.

In China, Meituan’s Flash Shopping non-food service grew to over 10 million daily orders by Q3 2024, with peak daily volumes reaching 25 million by August 2025. Non-food now accounts for over 40% of China’s total quick commerce market by value.

In SEA, the non-food quick commerce market is still very nascent. Consumer behaviour has not yet shifted to treating on-demand non-food delivery as a default channel. I believe there are a few constraints for this. Firstly, on the supply-side, brands and retailers have not yet positioned inventory close enough to consumers to make 30-60 minute non-food delivery economically viable across a broad SKU range.

As a reminder, the SKU range for non-food retail is 100x or more the size of food delivery.

The e-commerce market is estimated to be worth $359B in 2030. I believe it is fair to assume that about 3-5% of that could become eligible for same-day or instant fulfilment in dense urban areas within the region.

Assuming we do reach the higher end of that range by 2030, it would represent about $18B in GMV.