Everyone Is Wrong About The Emerging Markets Trade

Incredible Outperformance

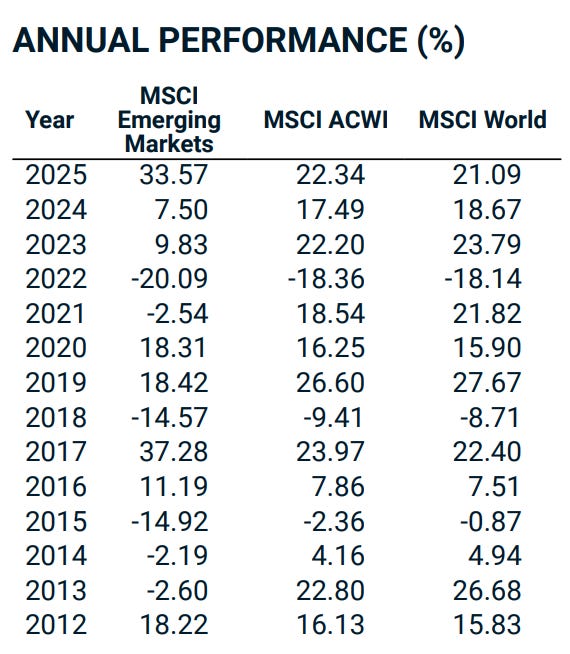

The MSCI Emerging Markets Index returned 33.6% in 2025, ahead of the S&P 500 at 17.9% and the MSCI World at 21.1%. EM ex-China did slightly better at 34.6%.

The index has carried that momentum into this year and is up ~25.6% YTD. Pretty much every strategist desk from JP Morgan to Lazard to State Street has been publishing constructive notes on EM since January.

Typically, when we see consensus like this, the chart has already played out and the easy money is often behind us, not in front of us.

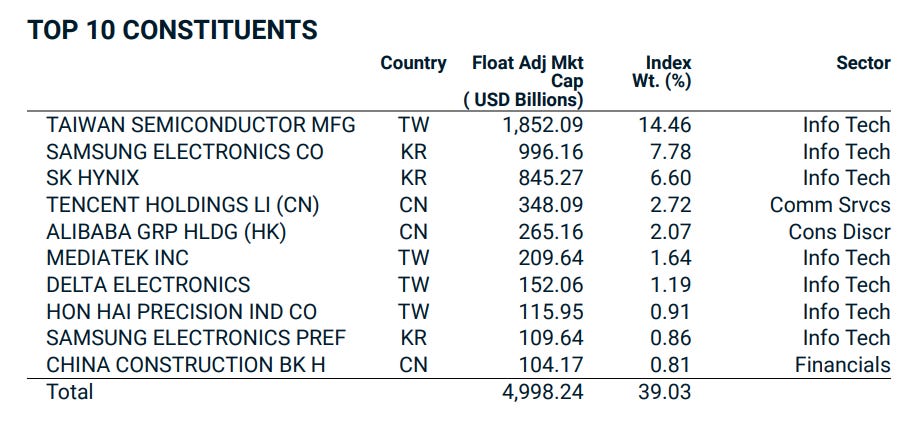

The truth is that when we look deeper into the EM indexes, most people who say “I am bullish on emerging markets” do not know what they are actually buying. The MSCI EM Index is now ~40% concentrated in its top ten names, and TSMC alone is more than 14% of it. When we add the rest of the Taiwanese and Korean semiconductor complex, the EM index is in large part, a leveraged bet on global AI capital expenditure.

The Other Side

However, the headline EM number hides a much more complicated story underneath.

On one side sits North Asian semiconductors and memory names like TSMC, SK Hynix and Samsung Electronics that have run incredibly hard on the AI build out. The forward returns for these businesses are now hostage to the same CAPEX revisions that govern Nvidia, Micron, Broadcom and others.

On the other side sits the structural EM story, which I believe has legs and a massive secular tailwind in the decades to come. These are typically businesses that operate in truly developing economies, the likes of Vietnam, Thailand, Indonesia, Brazil and Argentina. These businesses are levered to local consumption, financial inclusion, and demographics.

While the semis half of the story re-rated higher, several of the best domestic-demand compounders went the other way. They de-rated hard, through late 2025 and the first half of 2026. For instance:

Sea Limited has fallen from a high of $199 in October 2025 to ~$85 today, marking a ~60% drawdown despite posting three of its best quarters since.

Mercado Libre is down around 22% year to date and trades below its own 52-week low set last year, despite posting 49% revenue growth, its fastest since Q2 2022.

Grab sits near its 52-week low around $3.50, down roughly 28% over six months, while revenue grew 24% and adjusted EBITDA grew 46%.

Nubank is down over 26% YTD, after a quarter with record revenues of $5B (up 53% YoY) and $871M in net income.

dLocal is down 8% YTD despite accelerating TPV growth and its re-investment cycle coming to end.

Why I Believe The Other Half Will Re-Rate

There are four main reasons behind this.

The Iran war ending, and oil normalising with it.

The war that began on 28 February choked the Strait of Hormuz, through which roughly a fifth of the world's oil flows, and drove Brent toward $112 with Dated Brent spiking above $140.

Just a few days ago, the US and Iran reached a deal to end the war and reopen the strait, with formal signing set for 19 June in Switzerland. Crude is already back near $92, down around 20% from its 2026 peak.

Southeast Asia is a bloc of net oil importers, so the single largest macro pain of the last four months, imported inflation forcing local central banks to stay hawkish, is now reversing.

As the strait reopens and oil grinds back toward its pre-war equilibrium in the high-$50s to $60, that will be dis-inflationary for Indonesia, the Philippines, Thailand and Vietnam. This also gives central banks in the region the flexibility and option to cut, which feeds consumer spending and lowers funding costs for the digital lenders.

The earnings gap.

Consensus expects EM earnings growth in the high teens to around 20% for 2026, against roughly 13% to 15% for the US and developed markets.

However, the businesses I’m highlighting today are growing revenue at two to three times that index pace. Sea grew revenue 47%, Mercado Libre 49%, Grab 24%, Nubank 53% and dLocal 55%. The market can ignore the fundamentals for a year or two, but not forever.

What is the catalyst? I believe we are seeing a return-on-equity convergence, and that is crucial because it makes a re-rating permanent rather than a short-term trade. Return on equity is simply how much profit a company generates for every dollar of shareholder capital it holds, the cleanest single measure of how well a business compounds your money.

EM companies have historically earned a lower return on equity than their developed-market peers, and that gap is now narrowing as EM returns rise toward developed-market levels. One of the clearest signs of this playing out is that buybacks are becoming standard across these exact names.

Sea Limited:

$1 billion buyback programme announced on 17th Nov 2025

$168.4M exercised at average price of $93.55 per share as of Q1 2026

Nubank:

$1 billion buyback programme announced on 4th June 2026

Programme runs for 12 months from 4th June 2026 to 3rd June 2027

dLocal:

$300 million buyback programme announced on 18th March 2026

Permanent dividend programme, paying out 30% of FCF each year

Grab:

$500 million buyback programme announced in February this year

$400 million execution over 4 months ($250M ASR with JPM + $150M CFP with MS)

Governance and capital discipline are improving. I believe this will lead to a permanent re-pricing of high quality emerging market businesses.

The rotation out of the AI trade.

The AI trade has been the story of much of 2025 and all of 2026. Most of the deals have been led by the hyperscalers who have poured in billions in CAPEX and are expected to continue. However, there will be a physical limit to this eventually, as CAPEX guidance is beginning to run ahead of operating cash flow and free cash flow is heading negative. CAPEX revisions cannot keep ratcheting up indefinitely.

The moment those revisions stall, the optionality premium attached to anything AI-adjacent deflates, and a very large pool of capital will have to start looking for a new home.

The 2025 and 2026 YTD EM rally was substantially the semiconductor and AI complex. Globally, quality compounders have seen huge outflows and underperformance. I believe this will reverse soon, and benefit from a massive re-rating.

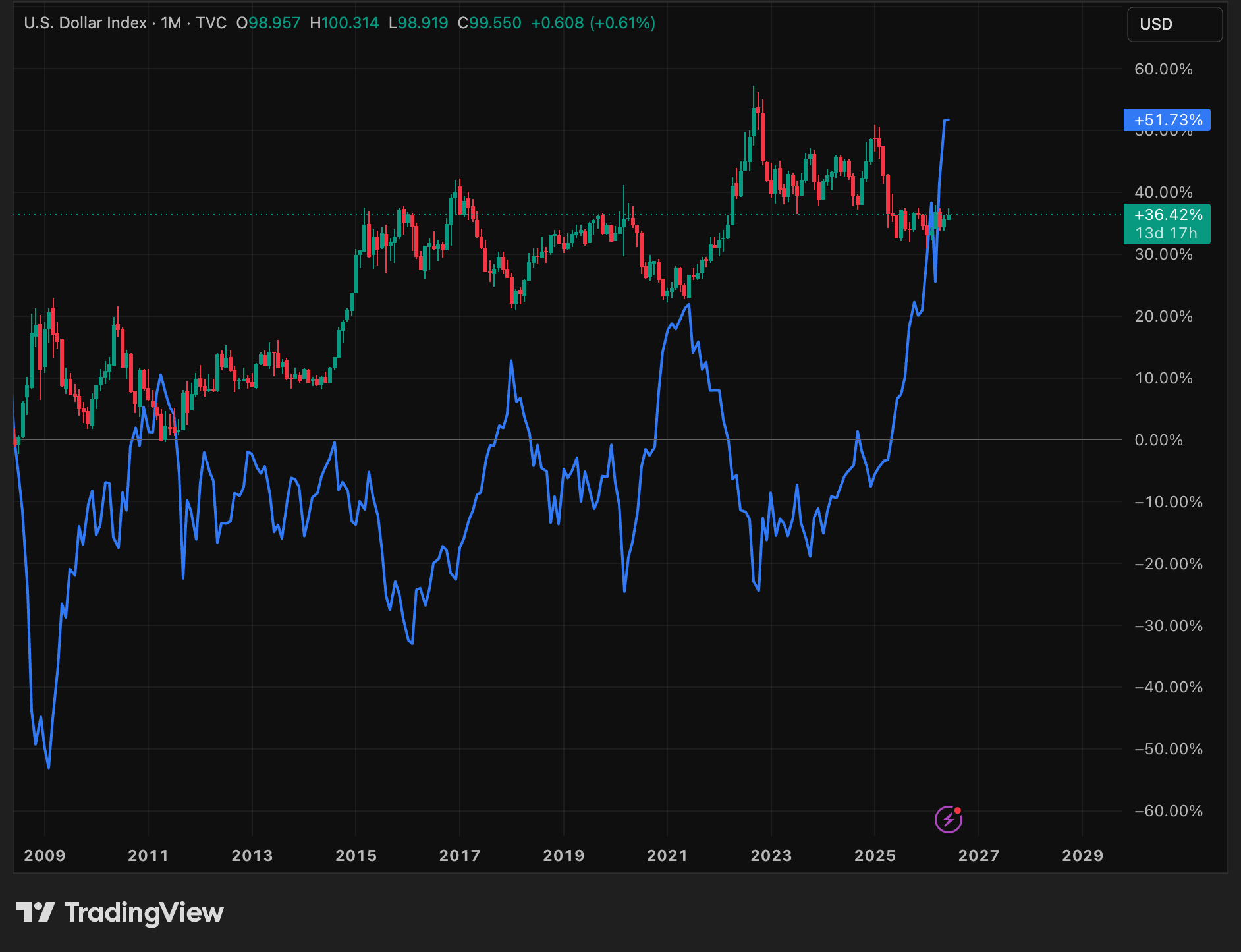

The dollar is the single largest driver of EM returns.

Emerging market debt is substantially dollar-denominated, commodities are priced in dollars, and for a foreign holder the entire return is translated back through the exchange rate.

When the dollar rises, EM is paying down hard-currency debt with depreciating local currency, importing inflation, and handing the foreign investor a currency loss on top of everything else.

When you look at the chart above, there is a near perfect inverse correlation between DXY (in candles) and EM (in blue). Cheap valuations did nothing for EM for over a decade (2011 to 2020) because the dollar was against the asset class the entire time.

The key catalyst is the dollar turning, and it has turned. There have indeed been several false dawns in the past decade. However, this time, there are 3 independent forces pushing the same way:

Cyclically, the Fed is easing, which narrows the rate differential that supported the dollar.

Structurally, the world is de-dollarising: the dollar's share of global reserves has fallen from about 71% in 1999 to around 56 to 57% by 2025. Emerging-market central banks cut their dollar holdings from 68% to 52% between 2013 and 2024.

Politically, a weaker dollar is the explicit aim of US policy under this administration, which views dollar strength as an obstacle to its trade agenda and is leaning on the Fed through a dovish chair willing to prioritise jobs over the inflation mandate.

Conclusion

I believe there are really two emerging-market trades today.

The first is the trade everyone already owns: Taiwan, Korea, semiconductors, memory, AI capex, and everything downstream of that cycle. That trade has worked incredibly well, but it is now crowded, consensus, and increasingly dependent on the next round of AI CAPEX revisions.

The second is the trade people are currently ignoring. High-quality domestic-demand compounders in genuinely developing markets.

There are massive secular tailwinds and structural growth in EM that reside in domestic demand. The best domestic-demand businesses have been left behind because they don’t fit the current narrative.

I can’t promise that these names will re-rate next quarter, but there are very real catalysts and reasons for them to perform incredibly well in the next few years. Assets typically bottom when nobody is buying and it feels dead. I believe that time is now.

Thank you for reading!

-Gab

Disclaimer: The content presented in this thesis is for informational and academic purposes only and does not constitute financial advice. The analysis and opinions expressed are based on research and should not be interpreted as a recommendation to buy, sell, or hold any security. Readers should conduct their own due diligence and consult with a qualified financial advisor before making any investment decisions.

Nice article, I think you've made a few valid points. But I don't feel that money will rotate into EM should the AI trade start to falter. I think historically the market has always viewed EM stocks as risk-on stocks, if investors do decide to flee to safety money will probably flow into consumer staples, healthcare, utilities etc... Or out of equities entirely.

Great article, thank you. The sharpest observation is in the opening and most readers will scroll past it. The EM index is 40% concentrated in its top ten names and TSMC alone is 14%. Which means the consensus "bullish EM" call and the consensus "bullish AI capex" call are the same position held in two different wrappers. Most investors who think they're diversified into emerging markets are actually doubling down on the same semiconductor cycle they already own through Nvidia and Broadcom.

That's why your second trade is genuinely different and not just contrarian for the sake of it. A domestic demand compounder in Indonesia or Brazil has no exposure to whether the next round of hyperscaler capex revisions comes in above or below expectations. The revenue is local, the growth is demographic, and the cycle is independent. If the AI trade unwinds, the first EM trade unwinds with it because it was always the same bet. The second one doesn't, because it never was. The diversification isn't geographic. It's structural.